The fourth quarter (Q4) of 2023 was an about face from the first nine months of the year. Just about every asset class was up almost the whole time and investors were optimistic. This, after investors had spent the bulk of the year on recession watch while punishing most stocks and bonds. Expectations about inflation, recession, and the Federal Reserve’s interest rate policies were the crux of market developments for the quarter and year before momentum finally turned positive in a big way during Q4.

Here’s a roundup of how major markets performed during the quarter and for the year, respectively:

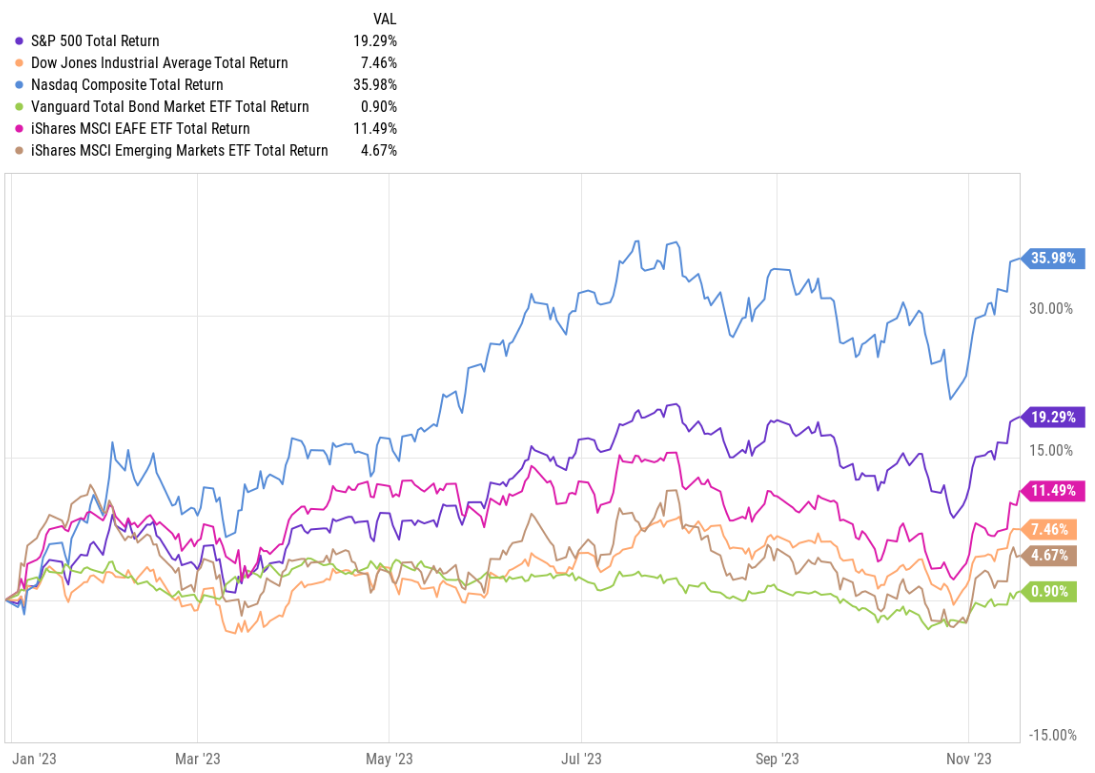

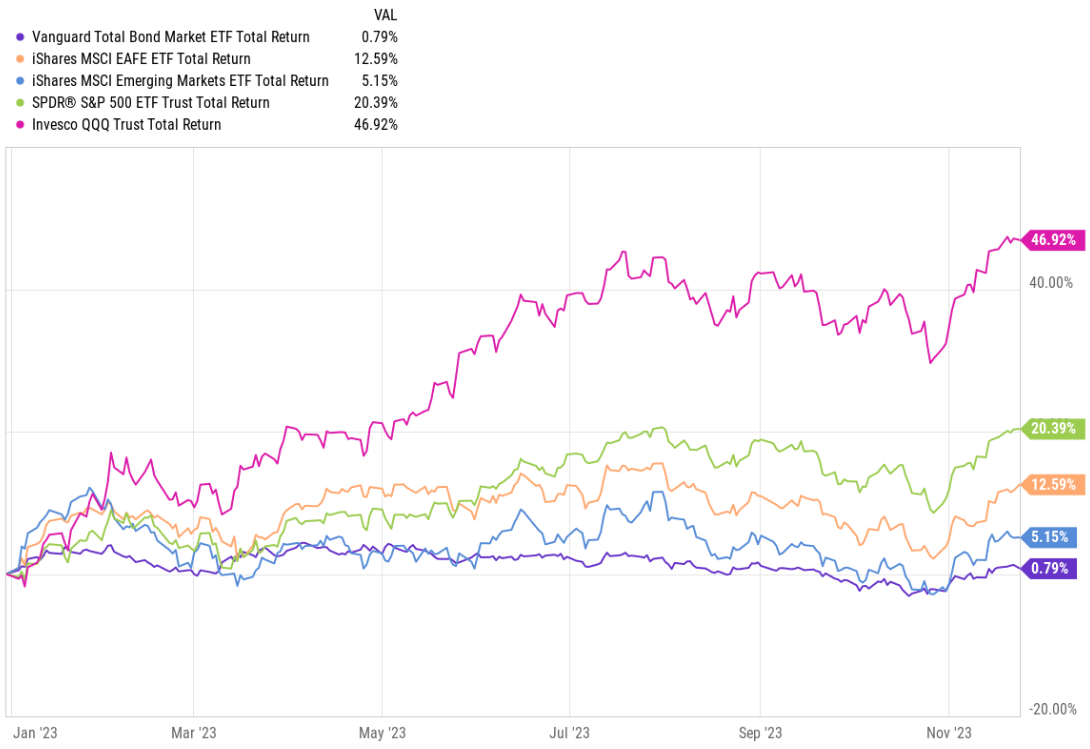

- US Large Cap Stocks: up 11.7%, up 26%

- US Small Cap Stocks: up 14%, up 16.6%

- US Core Bonds: up 6.8%, up 5.5%

- Developed Foreign Markets: up 10.5%, up 18.9%

- Emerging Markets: up 7.9%, up 10.3%

Most of the stock market’s 11 sectors limped into Q4 while major indexes leaned on a relative handful of stocks within the Tech, Communication Services, and Consumer Discretionary sectors for performance. AI enthusiasm boosted returns and companies in the S&P 500 like NVIDIA, Meta (Facebook), AMD and Tesla were each up over 100% for the year, far outstripping the index’s return. Much of the rest of the stock market spent most of the year in mixed territory and suffered several demoralizing slumps as the months ticked by. Sectors such as Healthcare, Energy, and Utilities finished the year down a bit. In fact performance and the general environment (multiple wars, bank failures earlier in the year, and lingering concerns about inflation to name a few of the issues present) created enough uncertainty that investors spent much of the year feeling quite bearish about investing.

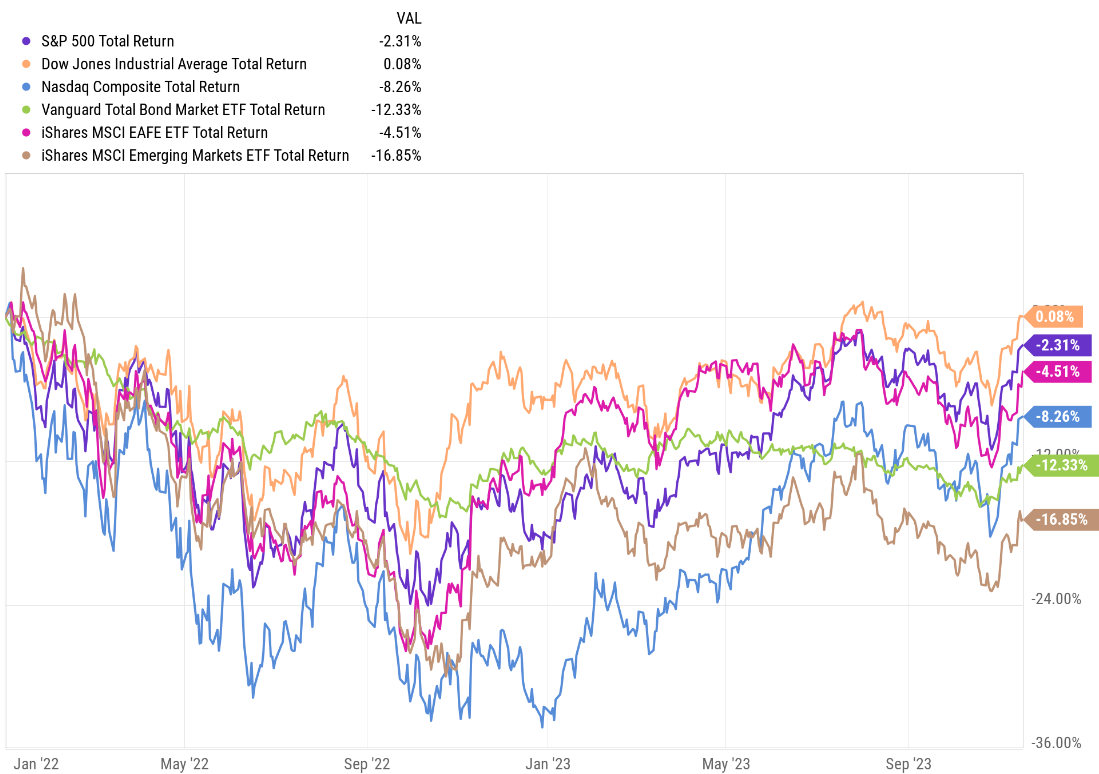

From about late summer the stock market began another of its downward slides that eroded returns across markets well into October. Indexes with less tech exposure to help hold them up, such as the Dow Jones 30, were pushed into negative territory and the nascent recovery from bonds was smashed. The numerous reasons for this went back to the Fed and what they might do with interest rates.

Investors saw the Fed pause rate increases during the summer but were expecting plans to cut rates. That wasn’t materializing fast enough for investors and the central bank remained hawkish about its willingness to fight inflation. Interest rate sensitive sectors and the bond market saw values suffer as rates continued rising even while the Fed was in pause-mode. The 10yr Treasury, a key benchmark, rose to 5% in late October and that ultimately marked a turning point. Investors began feeling certain that interest rates had risen high enough and that the Fed would start reducing rates early in 2024. This was eventually confirmed, more or less, by the Fed Chair during Q4. Investors cheered this change in direction and bought bonds, sending the same 10yr Treasury yield that had recently been so worrisome back down below 4% as the year closed.

This long-awaited dovish tilt for the Fed sent markets soaring throughout November and December. Almost like flipping a switch investors turned bullish, pushing top performers higher while lifting asset classes and sectors that had been lagging. As you can see from the performance numbers mentioned above, core bonds can thank Q4 for their positive performance and emerging market stocks can too. Another example of the rapid sentiment change came from US small cap stocks which saw their primary index change from a 52-week low to a 52-week high in just 48 days, the shortest timeframe ever according to my research partners at Bespoke Investment group.

One takeaway from Q4 and last year as a whole is that market volatility works both ways. Downside volatility is scary because it can happen fast but prices can rise just as quickly. Bespoke also shared that the turnaround for a typical 60/40 (percentage in stocks and bonds, respectively) asset allocation did well last year but much of that growth occurred during the last two months. That recovery was nearly as fast as coming out of the Covid market lows in 2020. Does anyone think the environment last year was that bad? Regardless, the collective will of investors around the world can change rapidly and has the tendency to create a sense of whiplash and of being left behind.

The outlook is good as we enter 2024. Goldman Sachs publishes an index of financial conditions and, due primarily to the Fed policy shift already mentioned, conditions swung from tight to loose quickly during Q4. In the past that has boded well for markets and the economy a year out and this helps fuel the current positive narrative. But as we know, dominant narratives and investor sentiment can turn on a dime so it’s best, as always, to be cautious. Some analysts suggest that stocks are priced for perfection and that investors could be overly optimistic about Fed rate cuts, so some amount of pullback should be expected even in the context of a continued bull market.

The repeated lesson from all this is to double down on planning, ensure your portfolio makes sense relative to your plans, and then stay the course while making necessary adjustments along the way. Growth will happen but it takes time and demands intestinal fortitude. Nothing is free but staying calm and disciplined while others around you are panicking is as close to a free lunch in the investing world as you’re likely to get.

Have questions? Ask us. We can help.

- Created on .