Last week’s two-day drop in the stock market caught a lot of people off guard and it’s continuing this morning after the holiday weekend. Stocks had been on a tear for a while and some investors were getting a little too complacent. Sounds familiar, right? Periods of relative calm followed by volatility slapping you in the face – that’s been typical market behavior in recent years and is common over the long-term. But it feels worse when markets get extra frothy based on short-termism and thin news.

An example of this short-term thinking is how day trading is coming back into fashion. In recent months “retail” traders have been plowing money into the big tech names, helping to drive prices up to nosebleed levels for certain stocks. The popularity of the Robinhood “freemium” trading platform illustrates this point. The firm makes it incredibly easy (maybe too easy) to buy shares of stock and reported over 4 million trades per day in June, eclipsing more established firms like TD Ameritrade and Schwab. This followed a large spike in trading on the platform during the early stages of the pandemic.

These numbers are reported with a lag, but we can assume this activity continued through the summer as a relative handful of stocks rode the wave of popularity. The narrative here is that younger unemployed folks were bored during the shutdown and started trading stocks with their stimulus money. They did well by getting lucky and got too enthusiastic. That seems overly pessimistic and a little harsh, but I can imagine many of these short-term traders getting caught unawares and dumping shares in recent days. That, plus the rapidly shifting sentiment of computer algorithms and other speculators who make up much of the day-to-day on Wall St, was certainly sufficient to blow some of the froth off tech stocks.

So, in addition to everything else impacting stock prices these days we have to add newbies with itchy trigger fingers trading stocks on their iPhones. At least it provides a clear example of what not to do. Speculation versus long-term investing; know the difference!

Another factor driving stock prices lately was news that Apple and Tesla were splitting their stock. An abundance of splits helped fuel the 90’s tech bubble but had fallen out of favor in recent years. The current price slide notwithstanding, the split news had a big impact on each company’s share price, so it’s possible more companies will want to split their stock. If so, this could be a tailwind for the markets as we emerge from recession.

Along those lines let’s review a few paragraphs from my research partners at Bespoke Investment Group, in which they look at the recent Apple and Tesla splits and what they might say about the makeup of the market.

In recent months Congress and the Federal Reserve have been “printing” trillions of dollars in response to the coronavirus pandemic. That old saying of “a billion here, a billion there, and pretty soon you’re talking about real money” now needs a “t” in front of it. With numbers this large it’s reasonable to assume all that money sloshing around the economy would eventually cause inflation. It could even be unaffordable and somehow wrong, depending on your choice of commentary.

It’s in this context that I recently read The Deficit Myth, by Stephanie Kelton, as part of a book club for financial planners (sounds like a real barn burner, right?). The book had been in progress for some time but was published right as the pandemic was revving up in March. The timing was a lucky coincidence for the author because the topic, Modern Monetary Theory, speaks to just about everything we’re hearing these days related to government spending, deficits, the debt, and the affordability of large amounts of economic stimulus.

MMT, as it’s known, is a big topic and I’ll only touch on some of it in this post. It has also been politicized in some circles for reasons that will become obvious the more you learn about it. As you’d correctly assume, I don’t get political in these posts so none of what I write below should be misconstrued as such.

Probably the most interesting thing to me about MMT as a concept is that it’s, as the name implies, an attempt to modernize the way we think about money at the federal government level. The U.S. has been completely off the gold standard since the 1970’s but most of our elected officials still think of our currency and federal spending in relatively archaic terms, according to MMT economists. It’s the way I learned it originally as well.

We’re almost five months into the aftermath of the coronavirus stay-at-home orders and our economic recovery is uneven at best. Some companies have been doing extremely well and their stock prices are up a ton due to having some sort of pandemic narrative (more people streaming Netflix, buying from Amazon, and so forth). This can absolutely continue so long as hopes of further economic stimulus remain.

Some individuals are doing fine, all things considered, in their work and financial lives. Others are retired and work issues are less relevant. But for others the work problems and financial woes are just beginning.

We’re all familiar with the many small retail-oriented businesses that have permanently closed following the confusion of temporary shutdowns. Recent data from Yelp lists California as having the third highest amount of permanent and temporary business closures per capita in the US (behind Hawaii and Nevada, I think). Many of these closures have been within the Bay Area, even our own county. Each of us probably knows at least one person whose financial life has been thrown into shutdown-induced chaos.

But lately I’ve been hearing from folks who had been feeling insulated from much of this. They’re not in retail or the restaurant business but nonetheless are finding themselves facing reduced hours or even an outright layoff. They’ve been mid- or late-career professionals who have saved money but not enough to pull the trigger on early retirement. They have young kids or are getting their kids through college. They’ll soon need cash but the only buckets they can draw from are their retirement accounts. They’re worried about taxes and penalties, not to mention needing to spend “future dollars” for current needs.

So, the following are some thoughts and rule changes related to drawing money from retirement accounts when you’re younger than 59.5 (an important cutoff for the IRS).

Holy cow, there’s a lot going on right now. In the news it’s social unrest and violence in the streets. Covid numbers are showing improvement, but still nearly 25 million Americans are unemployed or underemployed. Locally it’s two weeks of fire destruction, horrible air quality, and now stories of possible “smoke taint” for our region’s grapes.

According to the Press Democrat, the 2019 Napa, Mendo, and Sonoma County harvest was worth over $1.6 billion, with almost 40% of that being picked right here. Time will tell how hard this hits our grape growers but it’s not likely to be good news. And to top it off, it seems like every third person I talk with is considering moving. Where to? Lots of places. What else could be in this list of negativities? Probably a lot. These are challenging times, no doubt about it.

In lighter news, the major stock indexes are positive for the year after brutal losses during Spring. We’ve discussed previously how this rally has been due to a variety reasons but led by a relatively small number of stocks. The so-called FANG+ index is a good example. It’s made up of Facebook, Amazon, Netflix, Google, and includes stocks like Apple and Tesla. This index has doubled in value since the March lows. The latter two companies have now split their stock after a massive runup of 75% and nearly 500% year-to-date, respectively. Exuberance for certain companies seems to be getting irrational, so to speak, especially since a surprising number of high-quality stocks are still down for the year. But again, there are a variety of reasons for this and they’re not all crazy.

One reason is news from the Federal Reserve last week. The central bank announced changes to how it views its inflation-fighting mandate (it has two mandates - the other is to promote maximum employment). We need some inflation to keep the lights on in our economy, just not too much. We also need the Fed to help us expect where inflation might be headed.

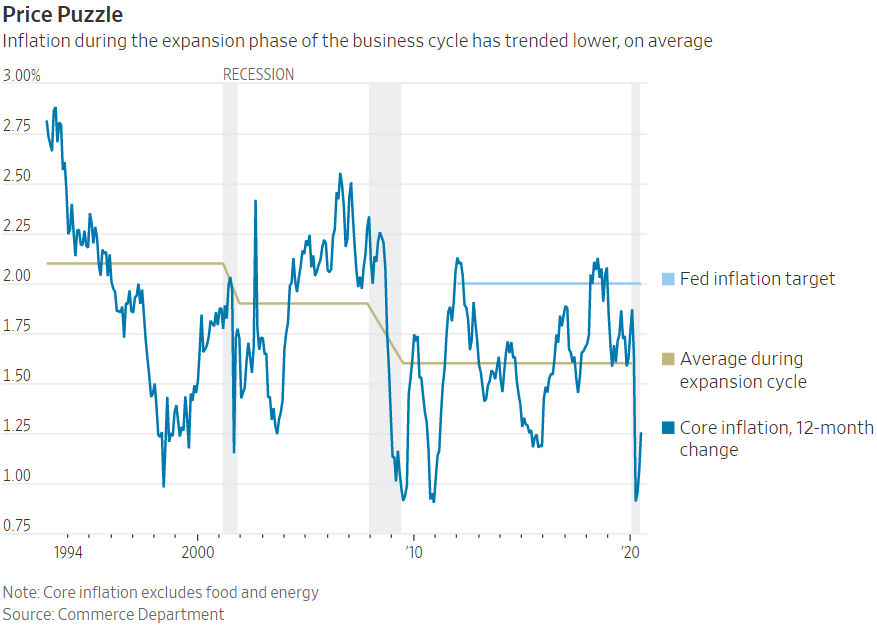

To help set clearer expectations, the Fed announced a specific target for annual core inflation (“core” removes food and energy prices) of 2% back in 2012. The problem, of course, is that since then our economy hit the target just a couple of times and only briefly (see the chart below from The Wall Street Journal). This, after the Fed added gobs and gobs of money to the financial system coming out of the Great Recession. Perhaps the Fed wasn’t being aggressive enough? Perhaps the focus needed to shift?

Well, last week the Fed announced its findings after looking at these issues as part of a review it began last year. It’s main outcome: Going forward the Fed will treat its inflation target as a longer-term average, letting inflation run higher for a time to balance out below-target periods. This is important because the Fed has already said it plans to keep interest rates low for a year or so as we emerge from the virus-induced recession. This change means that low rates could last much longer than that. The Fed may also get aggressive in pushing Congress for more stimulus spending and other regulatory changes.

All of this should stimulate the economy and continue to underpin the stock market (as of this writing on Monday the S&P 500 just ended its best August in decades). Low rates also punish conservative savers and an overly accommodative Fed can help create asset bubbles, so “low for longer” isn’t without risk. But we’re still digging ourselves out of an economic hole and need all the help we can get.

It’s tough out there in many ways right now, so I think it’s good to know that our nation’s central bank is innovating to help support the economy. They can’t find a coronavirus vaccine, re-open a closed business, or put out wildfires, but they can make borrowing money as cheap as possible. The Fed is also looking into how it can impact the social justice discussion, so that’s positive too. Let’s take good news where we can get it, right?

Before I begin this week’s post, I can’t help commenting on the weather we’ve been having these past several days. As I wrote this yesterday morning the sky was dark, rumbly, and ominous. And the sights and sounds during the wee hours of Sunday were truly phenomenal.

Like many, our family was woken around 4am by thunder and a tremendous crack of lightning that caused a fire across the street from our home. Fortunately, the rain came and the wind died at the perfect time to help neighbors extinguish the small blaze. If nothing else, this unpredictable weather shows that anything can and will happen. Anxious and exciting times indeed!

Much the same can be said for our economy as it emerges from recession. We are all aware that the recovery so far has been uneven with some sectors doing much better than others. In many ways this reflects the rapid adoption of technology that we had been on the path to adopting anyway. Two obvious examples are the shift to virtual instead of in person meetings and the Amazonification of retail. Both offer long-term opportunity for our economy but lead to messy unintended consequences in the near-term.

There are a variety of indicators to gauge how all of this is playing out in the real economy. Today we’ll look at two. I’ve previously mentioned the high quality and prolific work done by Bespoke Investment Group and wanted to share some of their insights with you. I’m going to italicize their work below so you can tell who’s who.

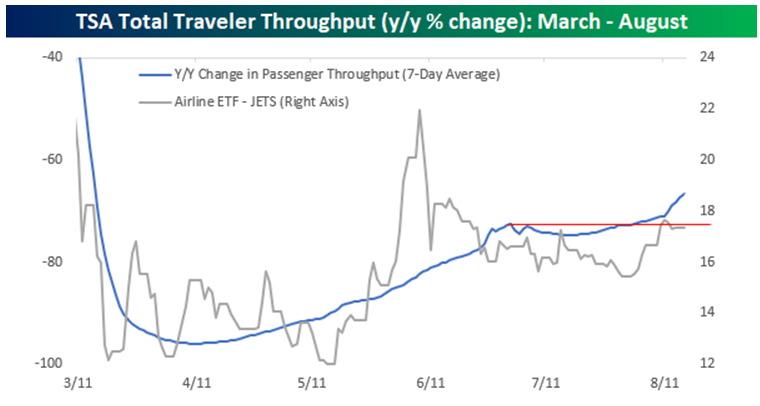

The first indicator we’ll look at is air travel. The TSA reports how many passengers it processes through security each week. These numbers, like gasoline sales and freight traffic on the highways, gives us an idea of how the wheels of commerce are turning. In other words, if folks aren’t flying, they’re not doing business, spending money on vacation, and so forth. Yes, there’s Zoom, but not everything can be done virtually so actual travel is still vital to the health of the economy. We know that air travel dropped off a cliff following shelter-in-place orders in March. Let’s review where we are now.

According to Bespoke… there aren't many scenarios where a 67% year/year decline in any measure of activity is considered a good thing, but when it comes just four months after that same measure was at negative 96%, you can understand if people in that industry start to get a little bit excited. The chart below shows the seven-day average change in passenger throughput as measured by the TSA. Through Sunday, the seven-day average [was] 715,777 passengers compared to an average of 2.465 million passengers in the comparable seven days last year. While traffic is down 67% compared to last year, it was still the least negative reading for the seven-day average since 3/22, just days after the WHO declared COVID a pandemic in March.

So, TSA passenger volumes have been slowly moving in the right direction even in the face of travel restrictions and a general unease about being locked in a steel tube with other people amid a global pandemic. All kidding aside, this increase in passenger volumes is good to see, we just need to see more. A lot more.

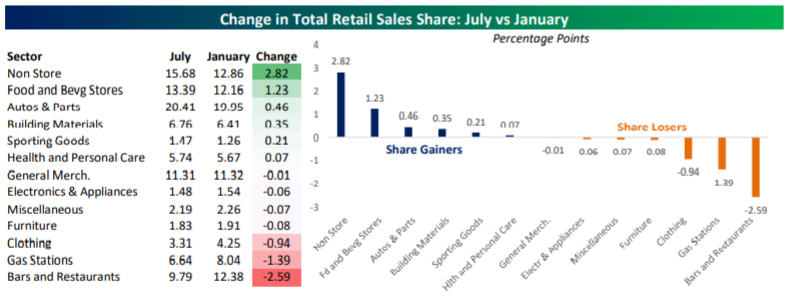

Another indicator is the detail within the widely reported retail sales numbers. The following chart and commentary from Bespoke shows how we’ve bounced off the lows of March and April, likely helped a great deal by Congressional stimulus. But we still have a way to go before we get back to normal in terms of what Americans are spending. Here's look at what folks are actually buying and how this has changed in the Covid era.

The table and chart below show how each sector’s total share of Retail Sales has changed between January and July. Online sales, which were already in a secular growth mode, only saw that growth accelerate with the sector now accounting for nearly 16% of all sales. With a large number of Americans still fearful of leaving their homes, it only makes sense that they would be shifting their spending to online providers… Covid has only accelerated what will ultimately be the dominance of online retail over brick and mortar peers… The next largest gainer in share has been Food and Beverage Stores, which have seen their increased share of sales come at the expense of Bars and Restaurants, many of which remain closed or at best serving limited capacity. Consumers are also going out less, and that means less driving and getting dressed up. That’s not good for Gas Stations or Clothing Retailers.

These indicators show us what we already intuitively know. The lives and habits of many Americans have shifted in recent months and each shift has a variety of corresponding economic impacts. Also, our situation is improving in the aggregate at the expense of specific parts of our economy. More stimulus from Congress will help keep these numbers moving in the right direction and assumptions about that are what, at least in large part, is driving stock prices higher. I’ll continue watching these and other indicators to see how all of this plays out in the coming weeks and months.

Greetings from your team here at Ridgeview Financial Planning. As I’m sure is the case for you, we’re adjusting to the recent re-shutdown of certain business categories including non-essential offices. Our building remains closed to the public, but we can still access it as needed. Fortunately much of what we do is already in the virtual world, so it’s been a relatively simple pivot for us these past several months. Now we just need to keep doing it a little longer.

As has been my routine in recent years, I’m taking the next few weeks off from writing my blog. I’m still working every day on your behalf, of course. I’m just harvesting extra time to spend with my family during what remains of summer.

I wish you all the best during these turbulent and anxious times. Little in our lives has been untouched by this crisis but I am optimistic about our future. (Repeat that last part like a mantra.) I hope you create opportunities to enjoy the beautiful summer weather.

The following few-minute read is from Liz Ann Sonders, Chief Investment Strategist at Schwab. It’s especially challenging these days to find voices of reason, and Liz Ann is one of them. In this article she reiterates how our economic recovery is likely to be lumpy and bumpy and protracted, what she refers to as “rolling W’s” instead of looking like a “V”. She explains that while some economic metrics showed a dramatic positive shift in June, which is great, they’re off historic lows and shouldn’t be expected to continue in the same way.