The third quarter (Q3) of 2023 was negative for the markets and, with the exception of returns through July, there were few bright spots. Core inflation continued to decline during the quarter while the economy remained resilient. The combination of the latter two items led the Federal Reserve to pause raising interest rates during the quarter while signaling to markets that rates could remain higher for longer than anticipated. This theme was prevalent during the quarter and helped push down market sentiment.

Here’s a roundup of how major markets performed during the quarter and year-to-date, respectively:

- US Large Cap Stocks: down 2%, up 13%

- US Small Cap Stocks: down 4.7%, up 2.5%

- US Core Bonds: down 3%, down 1.2%

- Developed Foreign Markets: down 3.8%, up 7.6%

- Emerging Markets: down 3.3%, up 2.2%

The AI stock boom that began the year wasn’t strong enough to propel markets through Q3. Ironically, that boom contributed to the selloff in stocks over August and September as investors hit sectors like Technology, down 4% for the quarter, harder than Financials which was down 1.2%, or Communication Services, which was actually up 1%. That sector and Energy were the only sectors positive for the entire quarter. And September saw every sector but Energy down for the month. Even though performance wasn’t that bad compared to history, merely down low single digits, all major indices ended Q3 in “Extreme Oversold” territory, according to my research partners at Bespoke Investment Group. So the tone was decidedly negative regardless of what the final numbers looked like.

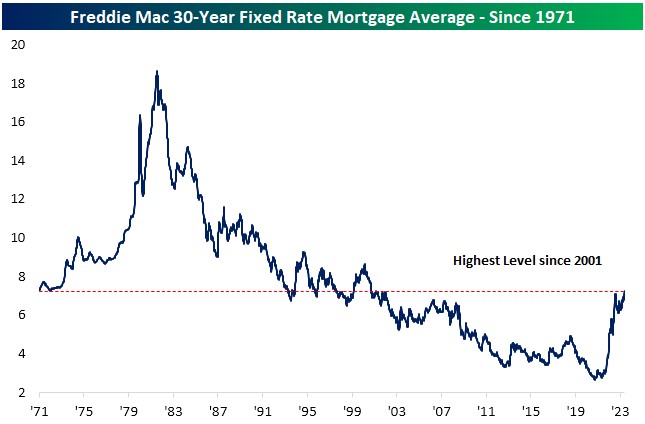

Bonds continued their poor performance during Q3. Even though the Fed pressed the pause button on raising short-term interest rates, investors raised them anyway by selling bonds across the maturity spectrum. Long-term bonds were hit hardest, with the typical government bond index down around 13%. Short-term government bonds eked out a positive return of about 0.6%, but the tone grew more negative as we closed out the quarter.

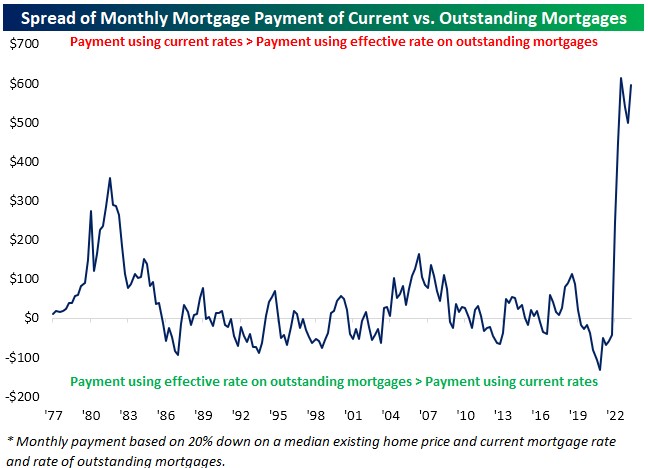

A big part of the negative performance we saw in Q3 was shifting opinions about if or when our economy will go into a recession, how bad it might be, and how high interest rates might rise along the way. This debate has been going on for many months now. Making this hard to pinpoint is that our economy continues to chug along due to a generally healthy consumer, a strong job market, and good momentum in the manufacturing and construction sectors. This, while the Conference Board’s Leading Economic Indicators index has been falling for nearly a year and a half. And the yield curve, a popular and near perfect recession indicator, has been inverted for almost a year without a recession occurring. Maybe higher interest rates haven’t hit home yet and it’s only a matter of time. Or perhaps we’re seeing see the fabled “soft landing” where the Fed raises rates quickly and slows the economy down without crashing it. Not much of this is typical and the general uncertainty amid otherwise favorable conditions is hard for many to reconcile.

And to top it off, investors also contended with another potential government shutdown as we closed out the quarter. Ultimately, Congress was able to craft an 11th hour bipartisan-ish deal to keep the lights on for 45 more days while somehow also generating more animosity and disfunction in its ranks. Unbelievable and believable at the same time, and a sad commentary on the state of our government.

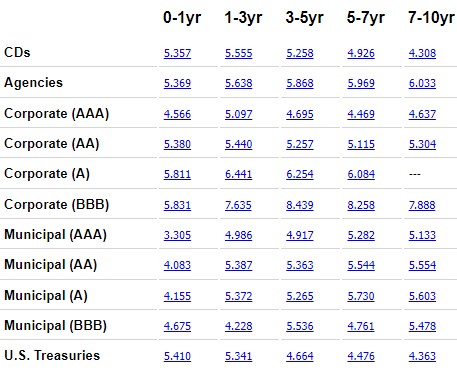

Some good news coming out of all this is that yields on cash are higher than they’ve been in a long time. This has been playing out for many months as well, but deposit rates continued to climb during Q3. As I write, FDIC-insured CDs are paying around 5.5% for a year and this matches up closely with Treasury securities of similar maturity. Now there are viable alternatives to bonds for short-term money, and perhaps also for medium-term money you would like to keep “safe” or otherwise earmarked for specific expenses. Contrast these yields with the roughly 1.6% dividend yield offered by the S&P 500, for example, and we can see where at least part of the pressure on stocks is coming from.

Keep in mind, however, that short-term yields are higher than long-term (that’s the inverted yield curve) so it’s hard to lock in 5+% for more than a couple years without taking on additional risk or other nuisance issues. Additionally, nobody knows where interest will be over any timeframe, so the ability to respond to shifting market conditions is important. Given that, I think there’s absolutely still a place for medium-term bond funds in your portfolio since they should outperform cash if given enough time. Additionally, be wary of moving too much money from stocks into cash for this same reason – we know from history that holding cash in lieu of stocks is a losing bet over the longer-term.

Fortunately for investors we are entering what has historically been the best quarter of the year for stocks, again according to Bespoke. I think odds are good for a decent quarter this time round given the steady selling we’ve seen lately, but the negative tone and rising bond yields from Q3 are still impacting prices as I write. Whatever awaits in the fourth quarter, a little help from the stock market (and from the bond market too!) would indeed be welcome as we close out the year.

Have questions? Ask us. We can help.

- Created on .