Volatility is Normal

As you are no doubt aware, last week was a wild one in the stock market. The Dow Jones Industrial Average, the index most widely quoted in the media, fell about 5% over two days before eventually ending the week on a positive note. The index ultimately declined a little over 4% for the week.

Other indexes did worse while some fared better. The index for small company stocks, which had been on a bit of a run lately, dropped over 5% last week. Emerging markets, the worst performing asset class this year, did better, only dropping about 2%. Bonds, which had been lagging all year, largely did their job and held their value, increasing a fraction for the week. In short, returns were all over the place while being generally negative.

I've mentioned before how so much of successful long-term investing is counterintuitive. Well, this is another perfect example. During times of market volatility, it's easy to get caught up in the emotion of seeing prices fall and thinking you have to do something. The irony is that it's often best to do nothing, or at least nothing rash.

What are some things to do when volatility spikes? Rebalance if needed, "harvest" some losses if reasonable, confirm your holdings are of good quality and in the right proportion, and generally stick to your plan. You know, the boring stuff.

But why did the markets suddenly get volatile last week, and so far this month in general? The following note from JPMorgan lays it out better than I can. The note also suggests (and I agree) that this is probably a short-term volatility spike and should serve as a reminder to stay calm and be well diversified.

October has seen the return of market volatility, with the S&P 500 Index falling for six consecutive sessions through last Thursday, its longest losing streak in nearly two years.

A combination of factors has led to this sell-off including fears of an overheating U.S. economy, Chinese economic deceleration, negative effects of tariffs on corporate earnings, perception of aggressive Federal Reserve rate hikes, and elevated equity valuations. However, after considering each of these factors in turn, they each appear to be downside risks to an otherwise still positive outlook for the U.S. economy and corporate profits.

Inflation still looks contained, the Chinese government has recently implemented a variety of stimulus measures to combat an economic slowdown, new tariffs still look like they can be absorbed by U.S. companies, interest rates are still rising slowly by historical comparison, and U.S. equity valuations are now marginally below average. As a result, this is likely a normal pocket of volatility, rather than the beginning of a bear market.

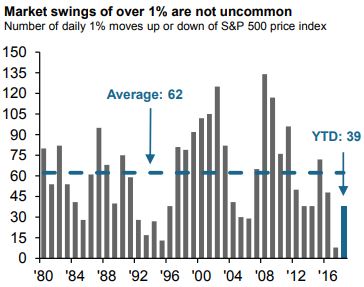

As seen in this week's chart, daily market moves of 1% up or down are not uncommon and have occurred an average of 62 times a year since 1980. This year, we have seen 39 such moves; this feels high when compared to 2017 but remains below the historical average.

Given a still constructive backdrop, investors should resist the urge to time the market or abandon equities altogether. Rather, given that the U.S. economy is later on in its cycle, this is a good time to ensure that portfolios are well balanced and diversified.

Here's a link to the note if you're interested:

Have questions? Ask me. I can help.

- Created on .