Updates to Social Security & Medicare

A couple of weeks back we learned about some important updates regarding Social Security and Medicare. I had meant to write about them at the time but, as happens every now and then, the markets turned volatile and took precedence within these posts.

While I'll address the updates below, here's a quick note from my research partners at Bespoke Investment Group. The note came out last week on the anniversary of so-called Black Monday. The important takeaway is, as the saying goes, "it's time in the market and not timing the market" that pays the most over time.

Please feel free to ask questions regarding current market volatility and the general outlook.

From Bespoke...

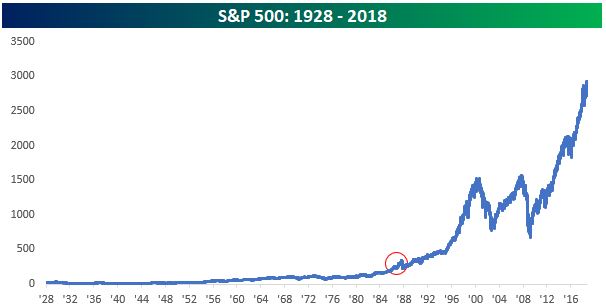

While Halloween is still 12 days away (remember, this note came out last week on the 19th), the scariest day of the year for many equity investors is today, as it represents the anniversary of the 1987 stock market crash 31 years ago. When you consider the fact that the S&P 500 fell 20% in a single day back in October 1987, the recent weakness seems like peanuts.

For anyone who was sitting around a trading desk at the time, we're told that it was the scariest day of their careers. That being said, look at the simple historical chart of the S&P 500 since 1928 below. You can barely see the 1987 crash.

More importantly, though, remember the number 9.9% because that is what your annualized total return would have been if you had 'bought' the S&P 500 at the end of September 1987 before the crash and held through today. While anyone making that trade in 1987 would have felt pretty stupid pretty quickly, over the long term, even buying equities at one of the worst possibly timed points in the last 50 years would have netted you an annualized return of 9.9%. Nobody knows where the market is going in the short term, but time and time again throughout history, the long-term direction has been the same.

Since 1975 the Social Security Administration (SSA) has been increasing benefits in line with a version of the Consumer Price Index (CPI), the metric commonly used to assess inflation. The Bureau of Labor Statistics calculates CPI based on price data of a variety of different goods and services. This metric is then compared annually by the SSA from the third quarter of each year and sets the increase for the following year's benefits.

The idea, as you can imagine, is to keep benefit checks roughly in line with prices in the real economy. The problem is that it doesn't always work out as intended.

We've seen some lean years in terms of benefit increases lately. In fact, the first two years of this decade (2010 and 2011) were the first years since 1975 that saw no increase at all. Ironically, the CPI was positive for those two calendar years, but happened to be negative during the quarter-to-quarter periods looked at by the SSA. This was during the Great Recession of course, obviously tough times for the economy when little growth was expected. But it still stung beneficiaries who lost out on a whole year of benefit increases due to what seemed like vagaries of the calendar.

A similar situation played out for the 2016 benefit year, marking the third time this decade without a bump for inflation. The culprit was a decline in CPI right at the end of the third quarter of 2015, due primarily to falling energy prices, if memory serves.

Since then, however, the economy has been doing better and inflation has been more consistent. There was a slight benefit bump for 2017, a 2% increase for this year, and next year beneficiaries will get a 2.8% raise. This is welcome because, as we are all aware, prices seem to be rising for just about everything and rising prices impact those living on a fixed income the most.

Healthcare costs are rising as well, but folks on Medicare are getting some good news too. Part B premiums are set to increase about 1.3% next year, or about $1.50 per month for a typical enrollee. Compare this to someone enrolled in the private insurance market staring down an approximate 9% increase in 2019 (in our area) and you can see this is a positive change for folks on Medicare.

Combine the Social Security benefit increase with the relatively small increase in Medicare premiums and retirees should see a net increase in their monthly benefit (most people withhold Medicare premiums from their checks) whereas in prior years the two sometimes canceled each other out.

So, this is all positive news for folks receiving Social Security benefits and those enrolled in Medicare. What does it mean for everyone else?

One takeaway regarding Social Security should perhaps be that while Congress mandates inflation increases to benefits, the CPI metric can be fluky (a technical term) and dependent on the calendar. Also, inflation adjustments typically lag actual household inflation and, as such, mean that the purchasing power of the payments degrades over time.

Because of this, and a host of other issues beyond the scope of this post, you should consider holding off from retiring if your plan is overly dependent on Social Security payments. "Overly dependent" is a subjective term that we all need to define for ourselves and, of course, I can assist in this process.

Regarding Medicare, a good takeaway might be how valuable the program is for retirees. Folks enrolling in Medicare often see a drop in their household premiums compared with buying insurance in the private markets, for example, where premiums could easily be two or three times the cost of Medicare. It's not perfect, of course, but I shudder to think of what retirement would be like without it.

Given Medicare's importance, and since we're now in open enrollment, it pays to know as much as possible about the program. A good place to start is www.medicare.gov and locally at https://senioradvocacyservices.org/hicap/, a non-profit in Petaluma providing education.

Here's a factsheet from the SSA detailing the changes for 2019.

https://www.ssa.gov/news/press/factsheets/colafacts2019.pdf

Have questions? Ask me. I can help.

- Created on .