Picking Out the Good Stuff

These are anxious times for many of you, I know. The stock market has been volatile lately and other news you're hearing may make it seem like things are going from bad to worse. There's good information out there, but sometimes we have to look for it.

We learned last week that our economy is continuing its strong run of over eight years of job growth. Our economy isn't perfect, of course, nobody's is, but the current 3.7% unemployment rate is near the lowest in history.

Wage growth is also picking up, climbing at a 3.1% annual rate, the highest since 2009. This is long overdue and will benefit many who have seen their wages stagnate against even the modest amount of inflation we've seen.

Additionally, according to the Department of Labor, the last several months have seen the number of job openings in our economy exceed the number of unemployed workers for the first time in history. Granted, fewer people are actively looking for jobs, but it's better to see more job openings as new this could tempt folks back into the workforce.

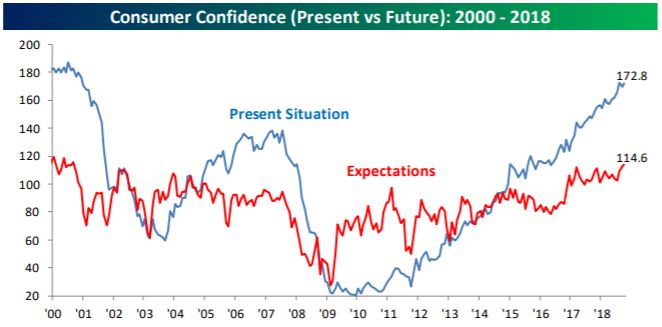

Perhaps due to these points, consumers continue to express growing levels of confidence. Interestingly, consumers are enthusiastic about their current financial situation while being less optimistic about the future. The following chart from Bespoke Investment Group shows this growing divergence.

While increasing consumer confidence and other data is largely positive, it is also indicative of an economy in the later portion of the economic cycle. But just because the next phase of the cycle is a slowdown or recession, it doesn't mean one's right around the corner. It also doesn't mean you should drastically alter your financial plans and start preparing for the coming zombie apocalypse (a link to the CDC's blog on the subject is below if you're interested...).

In all seriousness, it's important to frequently review the current market environment and the longer-term outlook. Don't just take it from me, however. Read below for a collection of excerpts from two recent JPMorgan research articles. The content is meant for advisors but it's worthwhile for anyone to see what some of the large institutional investors are thinking.

As we have traveled around the country in recent weeks, the most frequently asked question is whether the current bull market has come to an end. We think the answer is no - while we may have seen both peak economic and earnings growth, an economic recession does not seem likely in the near term and profits look set to continue growing next year, albeit at a slower pace. Furthermore, as the Federal Reserve continues to unwind the greatest monetary policy experiment seen in our lifetime and other central banks hint that they will follow suit, it should not be surprising that risk assets have come under pressure.

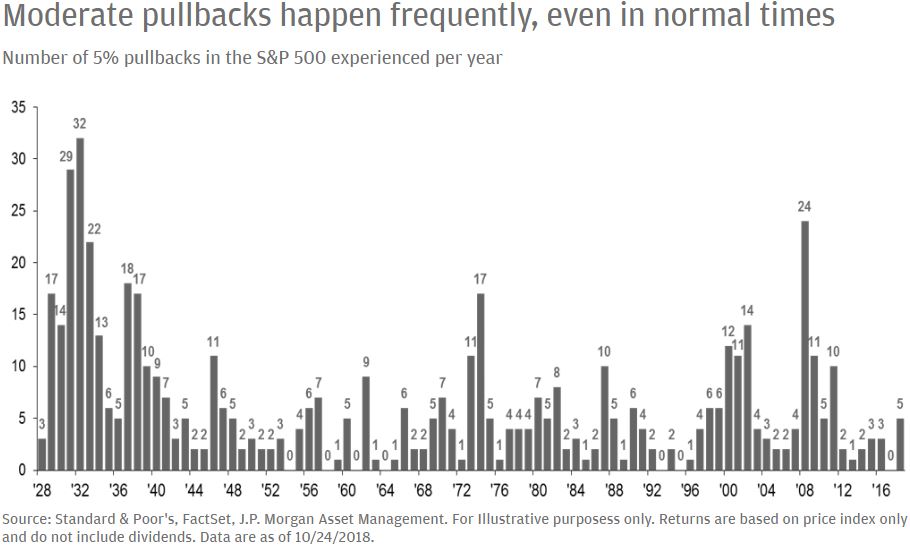

Times like these require a bit of an iron stomach, and a little bit of perspective. The S&P 500 has fallen by an average of 14% each year over the past 38 years. However, in 29 of those 38 years, the stock market finishes the year in positive territory. However, as shown in the chart below, 5% pullbacks are actually quite normal, reminding us that even in years where market returns are stellar, there can be rolling waves of volatility.

While markets rise and fall over the course of a cycle, the biggest pullbacks tend to come when an economic recession comes into view. With fiscal stimulus continuing to boost growth through the middle of next year, we are not at that juncture, at least not yet. Additionally, it is important to remember that over the past 20 years, 6 of the 10 best days have occurred within two weeks of the 10 worst days. In 2015, the best day for the market (August 26) occurred just two days after the worst day (August 24). Jumping ship when the outlook is bleakest is often the wrong decision.

Coming into 2018, the path forward for markets seemed clear: U.S. stocks would rise modestly after an exceptionally strong 2017, the dollar would continue its fall and international equities would once again outperform on the back of strong global growth and attractive fundamentals. But with the year-end looming, it is clear that this thesis has not played out.

Fueled by concerns of rising U.S. interest rates, slowing economic growth, ongoing geopolitical concerns and select disappointing earnings guidance, U.S. stocks are down roughly 7% quarter-to-date. International stocks have fared worse, with the broad ex-U.S. index down over 8%. As a result, many investors may be frustrated with the current state of their diversified portfolios, and are wondering: has recent performance affected long-term prospects?

The answer, perhaps surprisingly, is no.

https://am.jpmorgan.com/us/en/asset-management/gim/adv/insights/is-the-bull-market-over

https://www.cdc.gov/cpr/zombie/index.htm?CDC_AA_refVal=https%3A%2F%2Fwww.cdc.gov%2Fcpr%2Fzombies.htm

Have questions? Ask me. I can help.

- Created on .