Conference Notes: Updates on Aging

Last week I mentioned some takeaways from two speakers at recent conferences I attended and this week I’m continuing that theme. Part of the reason I make time for these conferences is the variety of information we get to hear. It’s a lot about investments, for sure, but we also hear from cybersecurity experts, technologists and futurists, financial therapists and, for nearly four hours, updates on aging in America.

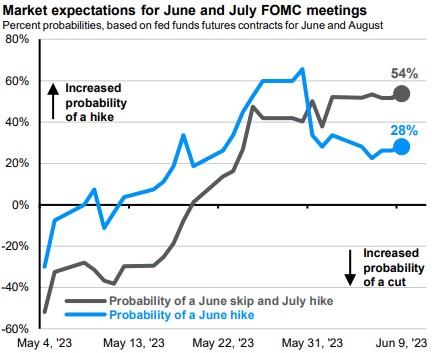

But before we get into that, a few people have asked about this week’s Fed meeting and whether our benevolent central bankers are likely to raise interest rates again. We’ll find out tomorrow, but the emerging consensus is that the Fed may hold off raising rates this month. The simplest summary of why this might be the case comes from JPMorgan and I’m including it and a chart below. The rest of my post follows.

On Wednesday, the Fed should provide more clarity on the trajectory of rates after vacillation in market expectations over the past month, which we illustrate in this week’s chart. As of Friday, the federal funds futures market was pricing in a 28% probability of a hike in June and a 54% chance of a skip in June followed by a hike in July. Since the FOMC last met, expectations have oscillated due to resilient growth, moderating inflation, diminished threats from regional banking turmoil, a solution to the debt ceiling standoff and mixed messages in the public pronouncements of Fed officials.

Given a gradual slowdown in growth and inflation and the fact that we have yet to see the full effect of the cumulative 500bps [100 basis points = 1%, so 500 bps is 5%] of hikes so far, the Fed would be well advised to pause at this point. Nevertheless, another hike is still clearly on the table and, if the Fed doesn’t hike this week, Chairman Powell will likely emphasize that skipping a rate hike now does not necessarily imply that the Fed is done raising rates. However, regardless of the Fed’s decision and messaging this week, we expect to see rate cuts within the next year that should improve the backdrop for investors across a broad range of assets.

Now on to the updates about aging in our country…

Carolyn McClanahan –

Carolyn was a family MD before becoming a financial planner and speaks about related issues from that unique perspective.

She’s an advocate for care planning since a lot of the problems faced by families with aging relatives could be avoided, or at least mitigated, by doing so. Waiting to plan makes just about everything more expensive, so start conversations early and write things down. These documents, even of informal agreements between family members, can help later when everyone is stressed.

Part of this means defining goals for care and understanding that those goals can, and often do, change. For example, how long does mom and/or dad want to stay at home? What resources (financial and familial) are available to support this? Who will take the lead on decisions and care, and are you planning to hire help? If so, get an idea of cost and plan for inflation. Earmark accounts and investments for these purposes.

The following site from Genworth is a good starting place to determine cost in your area.

https://www.genworth.com/aging-and-you/finances/cost-of-care.html

Are there sufficient resources? If not, start thinking about and planning for Medicaid assistance early.

Carolyn also talked about The Dwindles, or “failure to thrive”, that occurs in about 40% of elderly people. This can mean reclusiveness, lack of appetite and low energy, all of which makes caring for the individual more difficult and obviously impacts quality of life. This can be especially true for those widows and widowers living at home alone. Are they engaged with family and others? Who is measuring their quality of life, and do they have an advocate?

Carolyn spent more time talking about homecare and the variety of issues related to deciding to move into a more supportive environment. She offered this search tool from Medicare that shows homes and rehab services in your area.

https://www.medicare.gov/care-compare/?providerType=NursingHome

And this checklist helps with evaluating different types of facilities.

http://www.canhr.org/factsheets/nh_fs/html/fs_evalchecklist.htm

If your loved one has a long-term care policy, start the claims process early so as not to leave money on the table. There may be other benefits available, such as from the VA. Carolyn mentioned how some folks who served in Vietnam, for example, assume they don’t qualify, and nobody calls to find out. Other programs exist, such as SHIP and PACE in some parts of California, and those websites follow.

https://www.aging.ca.gov/Programs_and_Services/

https://www.npaonline.org/pace-you/pacefinder-find-pace-program-your-neighborhood

Andrew Carle –

Professor Andrew Carle, of Georgetown University, gave us a fabulous but at times bleak presentation on the future of aging. It’s a global phenomenon, with Japan and Italy listed as the #1 and #2 countries with the highest percentage of the population over age 65, respectively, but most of his talk was geared toward the US (we’re #36 on that list, by the way).

According to Prof. Carle, the three-legged stool of caregiving is collapsing. More households have both spouses working full time so there’s less time to provide care for aging parents. Additionally, roughly 20% of family caregivers are themselves over age 65 and 7% are over 75. And we’re over 4 mil short of professional caregivers. He discussed ways to address this staffing shortage, including pending legislation to incentivize entering the field, expanding legal immigration, and trying to keep older adults healthy and working longer (maybe even as professional/paid caregivers).

Carle’s other proposals included shifting away from seniors aging in place, which is inefficient for the healthcare system, to more facilities-based solutions that are easier to staff at scale. But he admitted that the industry needs to get away from the stigmas associated with “nursing homes” and build facilities people actually want to live in.

He said the assisted living industry is gearing up to offer more choice for seniors who want to congregate. These facilities will offer the same essential services but would be aimed at niche audiences, such as Asian-Americans, university alums, RVers, and even fans of The Grateful Dead and Jimmy Buffett. Some of these properties are quite successful, so more money is moving in this direction. These changes, Carle said, should accelerate as seniors demand better options for continuing care.

But since many seniors will still want to stay at home for as long as possible, the healthcare industry needs to help while not making the professional deficit worse. Along these lines Carle discussed the rise of what he termed “nana technology” to make care more efficient. Some of the ideas currently being researched by a range of companies and universities include:

Services that track medications and remind various contacts when it’s time to take a pill and if it isn’t taken. Apparently, medication-related errors are the primary cause of hospitalizations for those over age 65, so reducing this problem will take a load off the healthcare system.

Various gadgets and web-based services that track those with dementia/Alzheimer’s and alert a variety of people if the wearer gets outside of a predetermined range. Other services, such as Grandcare.com, track the wearer/user in their home and can provide telehealth services on demand.

Also mentioned were custom insoles for shoes that help with balance to avoid falls, and even exoskeletons from companies like Honda in Japan that greatly reduce fall risk. Researchers are also developing “i-textiles” that could serve all of the above functions while being worn like clothing. Apparently MIT is working on a version that will administer CPR if the garment’s sensors are triggered.

So, both of these speakers discussed the challenges of aging but there’s reason for optimism. Planning ahead can help alleviate a lot of stress down the road and various entities are trying to adjust and innovate to serve the aging population. There should be more choice in care options as time goes on and that should help keep quality of life higher for longer.

Have questions? Ask us. We can help.

- Created on .