How About Your I Bonds?

A few of you have recently asked what to do with your I Bonds, should you hold or redeem them. This is a good question amid the swirling interest rate environment, so let’s take a few minutes to look at some of the details.

As you may recall, we talked about buying I Bonds when inflation was peaking a year or so ago. I also bought some back then partly as an experiment because my preference is for investments that have an active secondary market that helps them to be easy and cheap to buy and sell. You buy I Bonds directly from the US Treasury on its website and, while not a horrible experience at any stretch, the process is a little clunky. Anyway, like many others back then I bought some I Bonds and, like you, are now considering my options.

I Bonds pay interest based on the Consumer Price Index and that inflation measure has come down meaningfully in recent months. At their peak during the summer of 2022, I Bonds were paying 9.62%. Yields on US Treasury bonds were in the mid-3% range at the time, for comparison. But since part of the rate calculation on I Bonds can reset every six months based on CPI readings, they marched down to 6.48% and then to where they currently sit at 4.3% for new purchases, including a recently increased 0.9% fixed rate. That’s a far cry from almost 10% a year ago, right?

The following chart from Treasury Direct shows this rate progression over time. I’m not reposting the image here because the text would be too small. Click the link if you’re interested.

https://www.treasurydirect.gov/files/savings-bonds/i-bond-rate-chart.pdf

And here’s some higher-level information on I Bonds for reference.

https://www.treasurydirect.gov/savings-bonds/i-bonds/

When I log into Treasury Direct I see that my original bond now pays 6.48% and another bond I purchased in January of this year is down to 3.79%.

These rates are lower but still decent, right? Let’s compare what else is available in the marketplace.

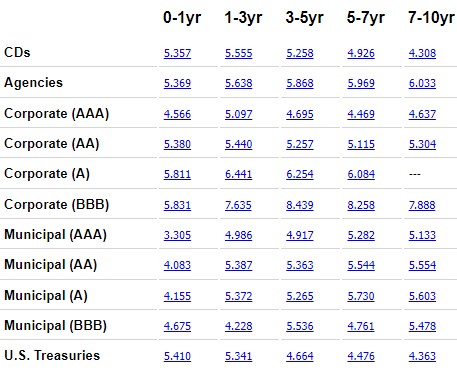

Below is a yield matrix from yesterday morning showing timeframes across the top and issuer type down the left side. To simplify, just look at the top and bottom lines and the left column showing rates on bank CDs and US Treasury securities out to one year. I consider both to be risk-free and each pay about 5.4%. These investments have a defined maturity date and, assuming you don’t need to sell them prior to maturity, essentially no risk. You’ll see other options below offering higher rates, but these get riskier as rates rise.

You’ll see in the second column from left that you can lock in 5+% returns for maybe a few years. Longer than that and yields drop meaningfully. You’ve heard of the inverted yield curve, right? This is what it looks like in the real world and it’s all backwards.

And a quick check of “high yield” savings accounts on bankrate.com shows that some online banks are offering 4.5% to 5% on money market accounts. Pretty favorable but those rates can change anytime.

https://www.bankrate.com/banking/savings/best-high-yield-interests-savings-accounts/

Alternatively, we can look at a typical bond fund that goes out a little farther, say in that 5-7yr column above. Vanguard Total Bond Market is an index fund that buys Treasuries, government agency, and high-quality corporate bonds, is free to buy pretty much everywhere, is cheap to hold, and pays a monthly dividend. It’s current yield, as measured in a standardized way known as the SEC Yield, has averaged around 4.6% in the past 30 days.

Okay, so we have options in the 5%-range for money out to a year or so, maybe a little longer with CDs and Treasuries. Money markets are nice but there’s no time guarantee there. Medium-term higher-quality bond funds offer a decent yield but can’t keep up with short-term investments amid an inverted yield curve. Bond funds will catch up eventually, however.

What to make of all this? Depending on what happens with inflation over the next couple of years and exactly when you bought your I Bonds, your investment return is likely to average out to about the same as the bond fund, perhaps a little less. You had a pop in rate for the first year or so, or maybe the first six months, potentially followed by X years of average to below average returns. In other words, I Bond returns where fun while they lasted and helped assuage the impact of high inflation but, assuming inflation continues coming down and stays there for a while, they quickly lose their luster.

So I suggest you monitor your I Bonds to see if the rate continues to drop. Roughly 4% is a decent return for short-term money but we don’t want medium or long-term money to linger too long at rates lower than that.

A couple other considerations…

- You’ve owned your I Bond for at least a year, ideally at least 15 months. The latter is because redemption prior to five years incurs a three-month interest penalty. It would be great to have at least received a year’s worth of interest. This accrues monthly and isn’t pro-rated, so ensure you’re counting in full months. I plan to hold the bond I bought in January until next Spring and then will likely be looking for the exit.

- You’re not holding onto the I Bond for some other reason, such as saving for college, where potential tax benefits are part of your calculation. If not for college, interest earned will likely be taxable at the federal level in the year you redeem, so just be aware of your tax situation. Otherwise, income tax on the interest is deferred so long as you hold your I Bond.

Other things to do with the money? Fund an IRA for you and your spouse. Or maybe indirectly add the money to your 401(k) or other plan at work. You can buy stocks if you’re thinking longer-term or consider medium-term bonds since rates have risen. Otherwise, that CD or Treasury going out a year or so looks pretty good right now if you don’t want to tie up your money longer than that.

And a quick business update: My associate, Brayden, has left Ridgeview to pursue other things. I'd like to thank him for being a diligent and patient student these past years, and I wish him well. I'll be looking for his replacement but, in the meantime, am positioned well due to support from my virtual asisstants, Brandy and Melissa.

Have questions? Ask us. We can help.

- Created on .