Thoughts on Housing Affordability

Sometimes it’s hard to tell if there’s more news on a topic lately or if it’s just the Great Algorithm in the Sky feeding me more of what it thinks I like. In any case, there’s been (or at least seems to be) an uptick in news about housing affordability in recent weeks.

There are good reasons for this. Here are some that come to mind.

The national average for a 30yr mortgage is now 8%, as measured by Bankrate.com. My system and the Wall Street Journal show it at 7.6%, but Bankrate tends to be a little better at determining loan terms actually available in the marketplace. In the grand scheme of things that’s close to the long-term average of about 7.7%, according to Freddie Mac. That’s small consolation, however, for new borrowers who feel they missed the boat on the sub-3% lows of the Covid-era.

The yield on the 10yr Treasury bond is bouncing around 5%. This imperfect but typical benchmark for mortgage rates has been rising relentlessly but gained momentum in the last month or so, driving mortgage rates higher. This has a lot to do with the Fed raising short-term rates but is also about inflation, expectations for growth, and how parts of our economy and financial markets are still struggling to find equilibrium post-Covid. The bond market is expecting rates to come down a bit in the second half of next year, but not dramatically. Higher interest rates make borrowing more expensive, but how long is a potential homebuyer willing to wait based on market expectations that are often wrong?

Redfin reports that 38% of recent homebuyers under 30 needed family money to cover their downpayment. This is higher than normal but understandable given the circumstances. It’s interesting that these “nepo-homebuyers” (meaning they rely on nepotism – I had to Google it) are still deciding to buy even though affordability is seen as a huge problem.

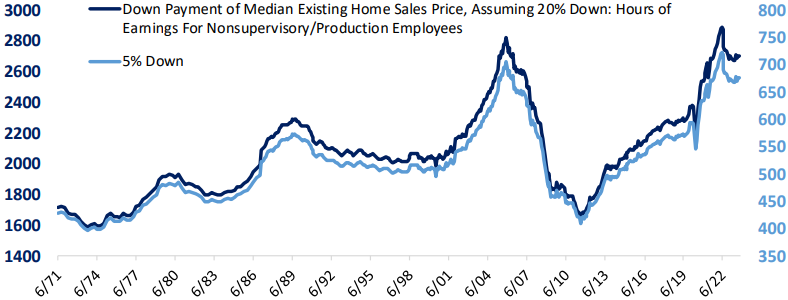

My research partners at Bespoke Investment group updated their numbers for housing affordability and it confirms the anecdotes – buying a home is expensive! The chart below shows how many hours of non-supervisory average hourly earnings (i.e. blue-collar workers) it takes to save a downpayment when buying at the national average home price. Magnify this by a homebuyer’s personal situation, such as not earning as much while living (or wanting to live) in a more expensive area, and it’s easy to see how unaffordable, or simply unattainable, homeownership can be for many people. That helps explain the nepo-buyers, right? Family help to buy a home is a head start or perhaps a cut in line, depending on your perspective.

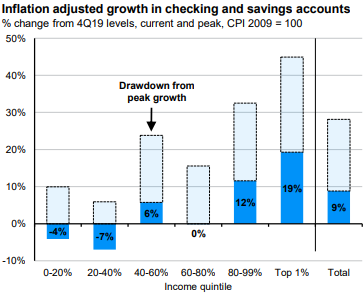

Along these lines, analysis from JPMorgan of recent Fed data shows how checking and savings balances by income level have changed from 2019. The light blue is the amount of drawdown from saving stimulus payments while the dark blue is the current balance for low-income to high-income folks, from left to right. JPMorgan talks about how surprising this data is given recession narratives and how this cash savings is part of what’s helping support consumption in the economy. The analysis doesn’t get into the home affordability concept, but it seems obvious where downpayment help is coming from, at least on average.

So what’s my point with all this? Buying and owning a home is expensive, we all know that. Nonetheless, many people still want to be a homeowner and I agree with them. Buying a home is an optimistic act and a commitment to the future that some, for a variety of reasons, aren’t ready, willing, or able to make and that’s fine. However, there’s a sense of security and freedom that comes from owning your home that’s hard to replicate. Yes, I can’t readily move as a tenant can at the end of their lease, but I can buy a dog and paint my walls mauve if the mood strikes, so it’s a fair trade. And it’s not like renting is a cheap option right now anyway. Even as inflation comes down, the relative cost of renting versus buying has remained high. (My opinion on home ownership is biased, by the way, because my wife and I have been homeowners for nearly 30 years after buying our first home at age 19 as nepo-buyers with maybe 3% down and haven’t looked back.)

Financially, after factoring everything in over the long-term, you usually come out ahead by owning versus renting. You benefit from the principal and interest portion of your mortgage being fixed (ideally) because, over time, inflation reduces the size of your mortgage payment relative to your overall income.

You can also expect the value of your home to grow at least by the inflation rate; a default long-term savings plan for your downpayment and monthly principal payments. If your home value grows faster and you make more than that, great! If you’re able to resize later to a nicer but cheaper home while paying down or paying off your mortgage, even better! Contrary to popular stories about people getting rich after mere months of home ownership, these outcomes are absolutely possible but usually take a long time to materialize.

So if you feel ready to be a homeowner, both emotionally and financially, go for it. It’s expensive but that’s normal and often worth it. Graciously accept help from family if it gets you into a home you can build from. Just don’t let yourself be overly swayed by outside opinions and risk overextending yourself. The National Association of Realtors and Redfin suggest you’ll stay in your home from 9-13 years on average, so the first or next home you buy likely won’t be your “forever” home. Be patient as you look for the right fit.

Remember – unless you’re actively flipping homes or are otherwise engaged in the real estate business, your home is your home first and an investment second. Begin with that in mind and you’ll likely be better off as a homeowner.

Have questions? Ask us. We can help.

- Created on .