Mid-Quarter Update

For this shortened Thanksgiving week let’s look at where the markets are now, sort of a mid-quarter update. You’ve likely noticed that stocks have done well over the past few weeks and bonds have perked up a bit too. The positive performance hasn’t been evenly distributed and this can lead to some head scratching when looking at your investment performance.

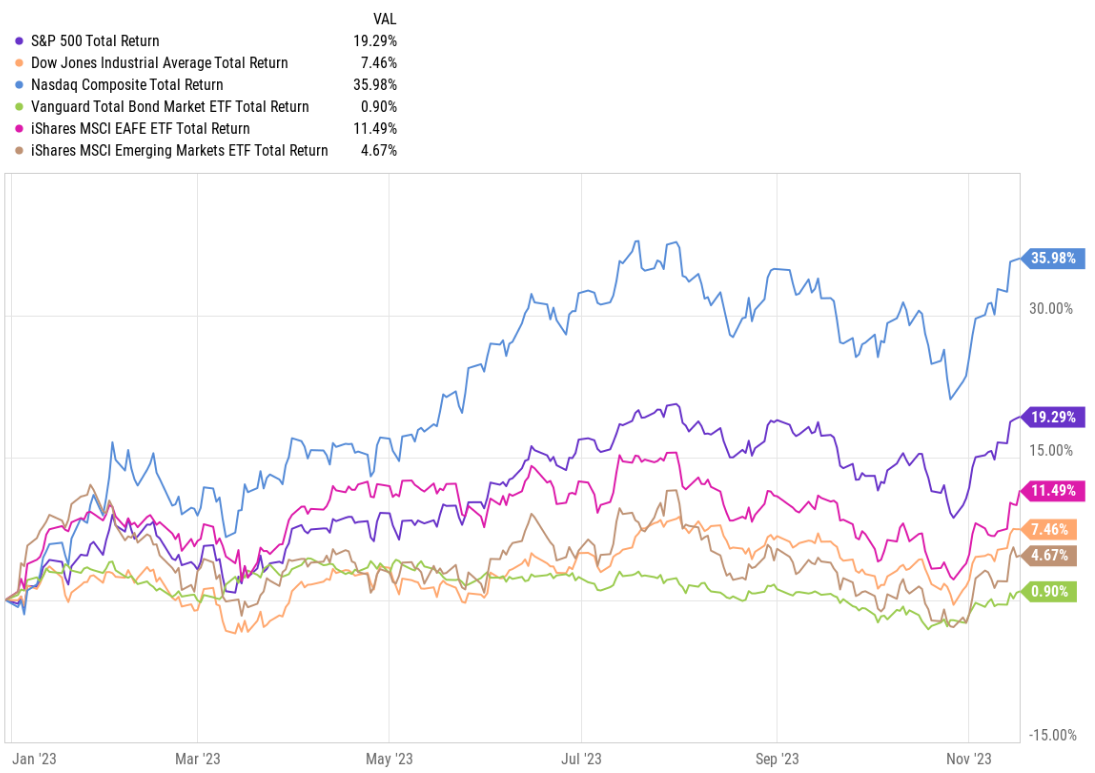

For example, here’s a chart showing the year-to-date (through last Friday) performance of major market indexes. You’ll see how the standout is the tech-heavy NASDAQ with the S&P 500 close behind. Then the bottom four lines on the chart are Developed Foreign stocks, the Dow Jones, Emerging Markets, and the US bond market, respectively. This same dynamic has been playing out across sectors as well with Tech, Communication Services, and Consumer Discretionary leading the other eight sectors by a wide margin.

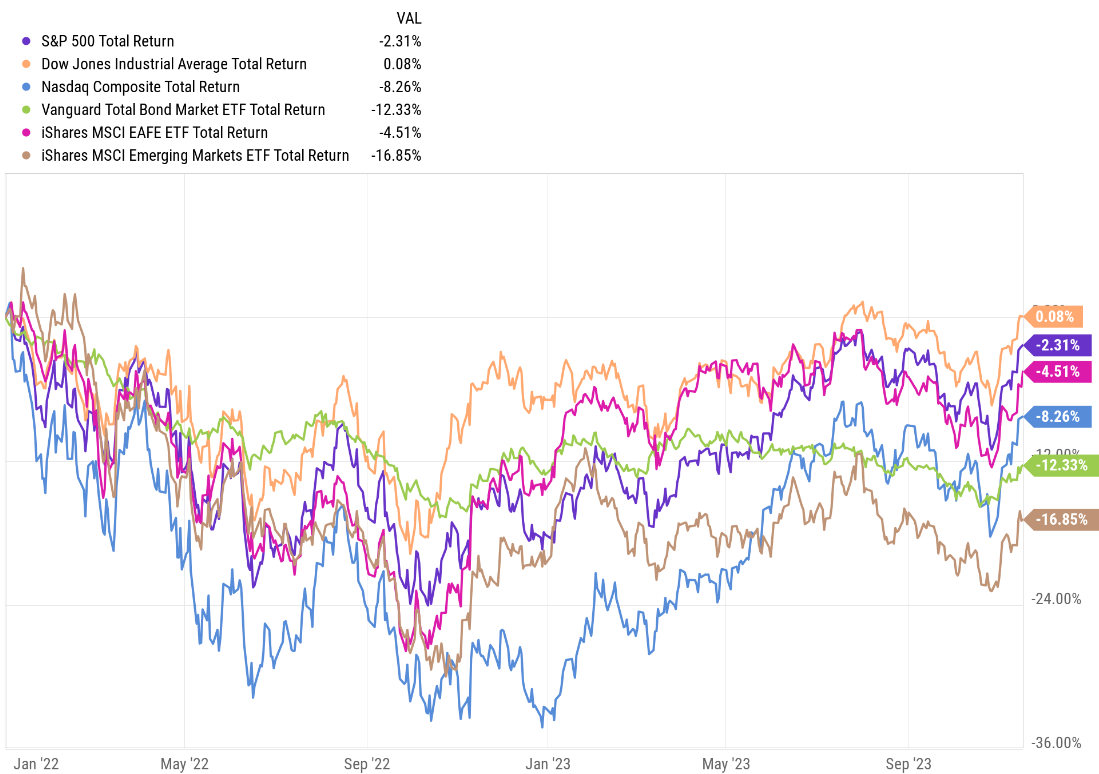

Now let’s stretch our timing back a bit to January 2022 before inflation and interest rates became big issues. You’ll see how the Dow Jones has held up well, followed by the S&P 500 and Developed Foreign stocks. Other areas of the markets, such as the NASDAQ, are still net-negative even with how well they’ve done this year. Core bonds have been the biggest heartbreaker of the bunch, down 12% since 2022 began.

Looking at it this way should help make sense of how your overall performance is dependent on the amount money you have allocated to each of these areas. More risk tolerant investors have been making up for ground lost last year while, ironically, more conservative investors have been dragged through the mud first by inflation and then the Fed’s fight to tame it.

Here’s a chart showing how Fed policy walloped bond prices as our central bank stair-stepped short-term rates higher to fight inflation. You’ll see those steps matched pretty closely by the yield on the 2yr Treasury, for example. Bond prices move in the opposite direction of yields, so you’ll also see how this impacted core bond prices as measured by the iShares US Core Aggregate Bond index fund.

But tame inflation they have, or at least that’s the narrative that’s been helping stock and bond prices recover in recent weeks. Yes, some prices in the economy remain high but on average they’ve been falling back toward the Fed’s 2% inflation objective. One example of this is gas prices. While the Fed doesn’t include gasoline prices when it assesses inflation, the national average gas price is 15% lower since Labor Day and this absolutely moderates inflation within the broader economy.

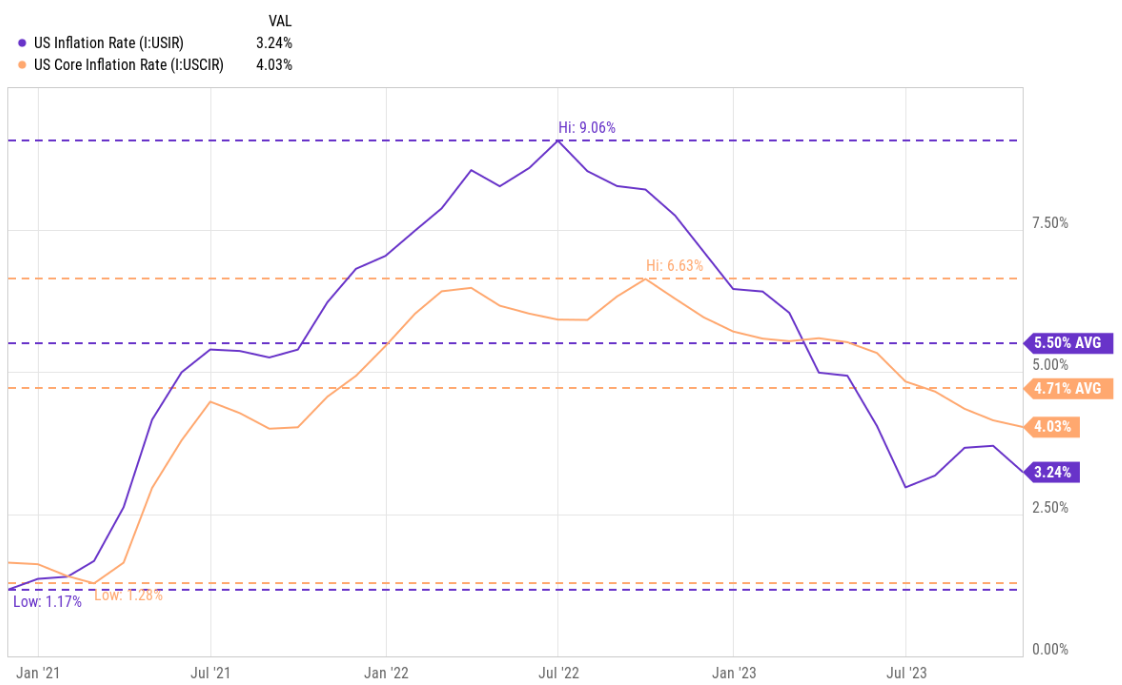

This next chart clearly shows the quick runup and nearly as fast decline of the Consumer Price Index that includes energy prices and it’s “Core” sibling over the past three years that doesn’t. Look at those lows in the lower-lefthand corner of the chart – that’s a dramatic change in average prices and it’s overwhelmingly positive that it’s been tapering off so rapidly.

I mention this recent history because it’s been fundamental to the markets this quarter and still is today.

As mentioned above, investors have been growing optimistic about inflation coming down and staying there, that the Fed has stopped raising interest rates, and that the fabled soft landing for the economy might actually be happening. We won’t know the answer to that until well after, unfortunately, so these issues will be prevalent into next year.

That said, here are a few things to consider related to your portfolio as we prepare to close out the year.

- Harvesting losses – This would likely relate to bonds or bond funds and is only relevant for non-retirement accounts. Look at your “unrealized gain/loss” detail within these accounts. I’m happy to help with questions about this, but Google the topic and closely follow the steps to offset other capital gains you might have or, at minimum, use up to $3,000 in losses as a tax deduction. Unused losses carry over to following years.

- Rebalancing – Go back to the first two charts above. Performance has likely been mixed across your portfolio and some areas may be out of balance. Assuming you have target weightings for each of your holdings, you may want to add a bit to bonds from stocks and to emerging market stocks from domestic to bring them back to target.

- Start planning for next year’s cash – Harvesting losses and rebalancing present opportunities for generating spending cash for the next 6-12 months. For example, you could sell some of your bond funds now if they’re at a loss and then leave the proceeds in a good money market fund or a CD that matures when you’ll need the cash. This, instead of planning to repurchase the harvested shares only to resell them in a few months. Better to keep that short-term spending money away from market risk and earn a good rate on cash while it lasts.

As a reminder, I’m handling these topics on your behalf if I’m managing your portfolio but let me know of any special cash needs.

I’m also happy to help hourly clients with these topics but time is scarce as we approach year-end.

Happy Thanksgiving!

Have questions? Ask us. We can help.

- Created on .