What's a Soft Landing?

Recently a few clients asked about what a soft landing for the economy would look like and how it might show up in the various metrics watched by market prognosticators. Soft landings don’t happen very often and there isn’t even an agreed upon definition for them so it’s natural to wonder about this.

Below I’m including some snippets from a good article on this topic by David Wessel, an economist and journalist formerly of the Wall Street Journal and frequently heard on outlets like NPR.

Of course we won’t know we’ve had one until it’s happened, but if there’s to be a soft landing one place it will show up is in consumer habits, so it’s instructive to look at Holiday spending expectations. Some reports have suggested a major decrease in expected gift buying, but I think it depends on who you ask. For example, the Conference Board surveys people on these topics and noted a difference in spending expectations for those 45 and older, who expect to spend more than their younger cohort when compared to 2022. Maybe part of this depends on who already owned a home before inflation and mortgage rates shot up?

Here's a link to the Conference Board information if you’re interested.

https://www.conference-board.org/press/consumer-holiday-spending-2023

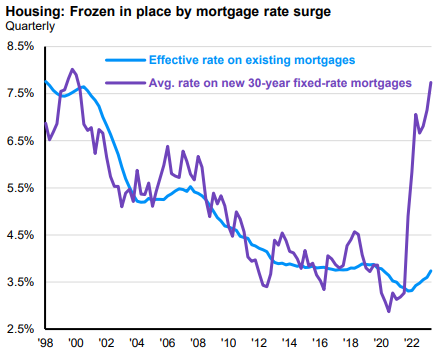

We’ve discussed these metrics before but the following chart from JPMorgan shows the spread between the cost of a mortgage on a home bought now versus existing mortgages. The difference in cost looks huge and it is, but what’s interesting is that according to JPMorgan fewer than 4% of American households bought a home last year. This suggests that the increase in mortgage rates from below 3% a few years ago to over 7% now hasn’t had a direct impact on the financial lives of the overwhelming majority of American homeowners. And since these folks are the ones doing much of the spending in our economy, the wealth effect that comes from rising asset prices coupled with comparatively great mortgage terms helps support this. Now, this consumption is expected to slow into the new year for a variety of reasons, but it’s not expected to crash due to unsustainable debt loads as it did before the Great Financial Crisis, for example.

Okay, now here are the article snippets I mentioned.

When the Federal Reserve is concerned about inflation, it raises interest rates to slow the pace of economic growth. If the Fed raises interest rates a lot, it may cause a recession – known as a hard landing. However, if the Fed can raise interest rates just enough to slow the economy and reduce inflation without causing a recession, it has achieved what is known as a soft landing. But there is no official definition of a soft landing. The National Bureau of Economic Research (NBER), often considered by economists as the quasi-official arbiter of dating recessions, does not define hard or soft landings. Many economists consider a mild recession with a small increase in the unemployment rate as soft – what Fed Chair Jay Powell once described as a “softish” landing.

Soft landings are the equivalent of “Goldilocks’ porridge” for central bankers: following a tightening, the economy is just right – neither too hot (inflationary) nor too cold (in a recession).

The classic example of a soft landing is the monetary tightening conducted under Alan Greenspan in the mid-1990s. In early 1994, the economy was approaching its third year of recovery following the 1990-91 recession. By February 1994, the unemployment rate was falling rapidly, down from 7.8% to 6.6%. CPI inflation sat at 2.8%, and the federal funds rate sat at around 3%. With the economy growing and unemployment shrinking rapidly, the Fed was concerned about a potential pick-up of inflation and decided to raise rates preemptively. During 1994, the Fed raised rates seven times, doubling the federal funds rate from 3% to 6%. It then cut its key interest rate, the federal funds rate, three times in 1995 when it saw the economy softening more than required to keep inflation from rising.

The results were nothing short of spectacular. Alan Blinder, former vice chairman of the Federal Reserve, noted that this was the “perfect soft landing that helped make Alan Greenspan a central banking legend.” Economic performance for the remainder of the decade was strong: Inflation was low and steady, unemployment continued to trend downwards, and real GDP growth averaged above 3 percent per year. Greenspan wrote in his memoirs that “the soft landing of 1995 was one of the Fed’s proudest accomplishments during my tenure.”

That depends entirely on how one defines a “soft landing,” a term for which there is no consensus definition. [Blinder…] says that if GDP declines by less than 1%, or the NBER doesn’t declare a recession after at least a year of a Fed rate-hiking cycle, he considers that a soft landing.

Here's a link to the full article. Check it out if you’re interested because it also includes a table showing pre-Covid recessions back to 1965 and whether the landings were “hard” or “soft”.

https://www.brookings.edu/articles/what-is-a-soft-landing/

Have questions? Ask us. We can help.

- Created on .