Ebbs and Flows

The investment management and financial planning business is endlessly fascinating. Every day is full of news stories, research and analysis, and data, always more data. Some of the more interesting data has to do with monitoring how folks across the country are investing their hard-earned savings. Firms like Morningstar and the Investment Company Institute track purchases and sales of mutual funds and exchange traded funds (ETFs). This "fund flows" data is extremely interesting to follow.

For some time now there has been a distinct shift in the stock fund realm with investors selling relatively expensive actively managed mutual funds in favor of less expensive passively managed funds and ETFs. This is an ongoing process that shows up clearly in the fund flows data but, ironically, does not fully extend to bond funds. As a reminder, "active" funds try to outperform a benchmark, such as the S&P 500, while "passive" funds try to match the benchmark's performance.

While actively managed stock funds had net redemptions approaching $400 billion over one year through March, actively managed bond funds were up by about $115 billion, according to Morningstar. In terms of net purchase ranking, the top five stock funds were all passively managed while the top five bond funds were all active. Money still flowed to passive bond funds during the period, but investors showed a clear preference for the active version.

This trend seems to be getting more pronounced. Especially over the past several months investors have continued plowing money into bond funds. This, even as the stock market has been on a bit of a tear since the November election and the Fed has been raising interest rates. Both of these factors would typically mean headwinds for bonds.

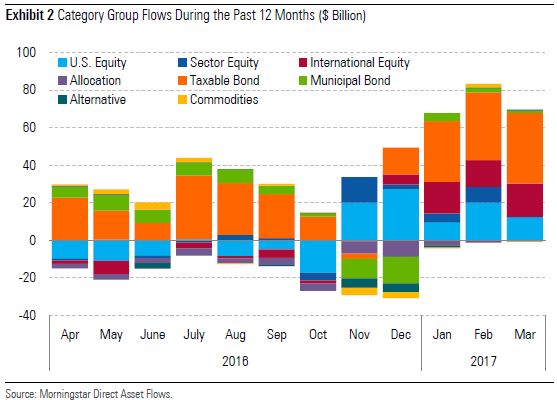

Investors sold bond funds (on average) in November and December but began adding substantially to bonds in the first three months of the year. This trend has continued into June with investors favoring medium-term bonds of higher quality and they have been net sellers of high yield (aka "junk bonds"). In fact, medium-term bond funds are outpacing stock funds in net flows over the past year, indicating that, at least in terms of where they're putting investment dollars, individual investors are more bullish on bonds than they are on stocks.

This is interesting and counterintuitive because the Fed is raising interest rates (bond funds often decline in value as rates rise) and the stock market has been doing well. Through last week, according to JPMorgan, the S&P 500 is up over 9% and so-called core (high quality) bonds are up 2.7%. Municipal bonds are up about 4% and high yield is up 5%. Investors often chase performance but, at least for a while now, many investors seem willing to accept the relatively low return of bonds in lieu of taking on more stock market risk.

This could be part of another trend in that, on average, investors aren't overly optimistic about the stock market and are generally either bearish or neutral about its growth potential. As I have mentioned in prior posts, bearish sentiment on the part of individual investors has been persistently high. According to a weekly survey published by the American Association of Individual Investors, the bears have outnumbered the bulls for 128 straight weeks.

Another aspect to this could have to do with demographics. As more investors get closer to retirement it's standard operating procedure to reduce exposure to stocks and add to bonds to increase stability and cash flow. At least in theory this would be done in any interest rate environment, so the Fed raising rates might not factor in very much to the decision. Additionally, if investors are doing what they're supposed to and rebalancing to bonds as stocks rise, that would accentuate this shift as well. But it still seems like, on average, investors are favoring bonds a little too much.

As time goes by and (presumably) the stock market continues to rise, it will be interesting to see if investors start to lose interest in bonds and move more toward stocks. If and when they do, it could indicate an overheating market since the recent runup has happened largely without the help of individual investors who usually show up late to the party. In the meantime, it will be beneficial and instructive to monitor the ebbs and flows of investor sentiment and how they allocate their investment dollars.

Have questions? Ask me. I can help.

- Created on .