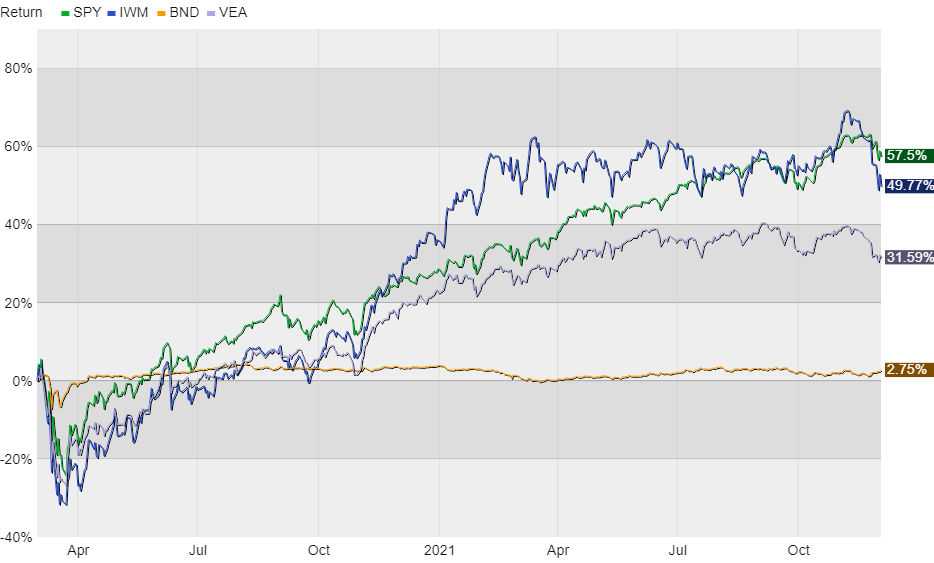

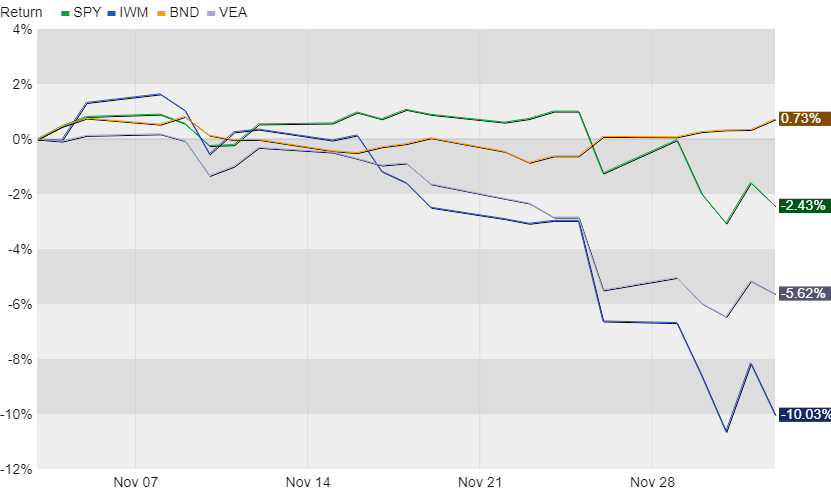

No rest for the weary. Isn’t that what people say as they push through a growing onslaught of obstacles? However one uses the adage, I think it’s appropriate as we head into the end of another eventful year.

In any other year we’d have deadlines for saving, gifting, harvesting losses and gains, and a host of other investment-related issues. Those are typical and can be planned for. But this year-end, on top of everything else we’ve been enduring, we also have to contend with what’s shaping up to be another eleventh hour set of major changes to our tax code.

While Congress has missed its own deadlines for the Build Back Better legislation, some senators are making noise about a vote occurring by Christmas. If that happens, and if the House plays along with the Senate’s version, we could be looking at the so-called social stimulus bill being signed into law right as the year closes. Most of the provisions don’t start until next year, but some, such as a dramatic increase to the cap on deductible state and local taxes (known as the SALT cap) could be retroactive for this year.

This matters because many property tax payers in expensive areas like ours would get to deduct more, or even all, of their property taxes whereas the current cap is $10,000. The Build Back Better version passed by the House raised this cap to $80,000, well within range of local median home values. This also matters because a larger tax deduction can create room for planning opportunities like Roth conversions, or even generating extra spending cash in retirement by selling appreciated investments. These would have to be done by year-end and would only work for some folks if the SALT cap was raised substantially. The final dollar amount of the cap will continue to be hotly debated in the days and weeks ahead, but there at least seems to be some consensus that it should be raised.

The problem, of course, is the waiting. Since we’re not likely to know when or even if Congress will send a bill to the president’s desk for signature this year, how does that impact our decisions today? I’m an advocate for making the best decisions now with the information you have available and not becoming a victim of analysis paralysis, but I’m still holding off for a bit to see how this plays out in D.C. After all, if it’s as simple as selling investments prior to market close on the 31st, I can do that in minutes.

But for anything requiring the processing of paperwork, the longer the wait the lower the chance that anything gets done. Typical processing cutoffs are around the 15th, or maybe Friday the 17th this year, well before Build Back Better becomes law. Big firms like Schwab and TD Ameritrade have pushed their cutoffs to earlier in December anyway, so we’re trying to cram in as much as we can at this point. Further waiting is unfortunate because any 2021 planning opportunties created by the legislation are likely to be a victim of the calendar.

On top of this back office stuff and pending legislation, we’re also living through the first meaningful spike of inflation in decades, looming issues with the debt ceiling again, and of course tons of uncertainty having to do with the pandemic. Each of these are big issues on their own, but also weigh down the Build Back Better legislation itself.

Here’s a recent podcast on these topics from Michael Townsend, Schwab’s Washington-based commentator. In a little over 20 minutes he breaks down the news from D.C. that’s important for investors to know.

https://www.schwab.com/resource-center/insights/content/content/washingtonwise-investor-episode-52

Finally, I want to wish you and your family Happy Holidays. It’s been another challenging year and connecting with those most important to you seems that much more important because of it. That said, I’ll be taking the next couple of weeks off from writing this blog. This creates more time to spend with family and opens up additional time for working with clients as we react to whatever Congress does, or doesn’t do, in the waning hours of the year.

Have questions? Ask me. I can help.

- Created on .