I don’t know about you but I’m running out of words to describe the times we’ve been enduring these last months. Challenging? Uncertain? Scary? Apocalyptic? Whatever we call this, it’s just plain tough to handle. And with the new local fires emerging it seems inappropriate to write about anything financial right now.

We’re ending the quarter this week and next Tuesday I’ll post my regular update. Until then I wish you and your family safety and good luck. These are (insert your own descriptive term here) times indeed, and we’re all going to have to dig deep to get through them.

While it may be small consolation with everything that’s going on, know that we’re still hard at work for you and are available to help whenever you need it, wherever you are and wherever we are.

That old saying about the last straw breaking the camel’s back has been on my mind a lot in recent days. How much is too much? It’s tough out there and things only seem to be getting tougher. But now it’s a growing number of conversations and news stories about folks just being done with it and planning to move out of the area. Many say they’ve been at the tipping point for a while and the current smoke situation is that final straw that feels like a ton of bricks.

All this has me considering the thought process behind relocating. It’s a complicated thing, upending your life. There’s lots of risk but big potential rewards. And deciding to move involves a series of tradeoffs that are intensely personal. So this is a big topic, but I’ll highlight some of the core financial issues now and in the coming weeks.

Let’s look at a common question when you’re moving out of state: to sell your home or rent it.

If you’ve owned your home for a while you likely have a good amount of equity. This is great because you can transfer it, so to speak, to somewhere on a long list of states with cheaper housing prices and probably overall lower cost of living. We pay a premium to live here and it’s no surprise that our housing cost is over twice the national median and over 50% higher than Austin, TX, a popular would-be destination for folks leaving Sonoma County.

To illustrate how leveraging this Sonoma County premium could work at the household level, here’s a scenario using median home prices and typical homes here and in Austin.

Holy cow, there’s a lot going on right now. In the news it’s social unrest and violence in the streets. Covid numbers are showing improvement, but still nearly 25 million Americans are unemployed or underemployed. Locally it’s two weeks of fire destruction, horrible air quality, and now stories of possible “smoke taint” for our region’s grapes.

According to the Press Democrat, the 2019 Napa, Mendo, and Sonoma County harvest was worth over $1.6 billion, with almost 40% of that being picked right here. Time will tell how hard this hits our grape growers but it’s not likely to be good news. And to top it off, it seems like every third person I talk with is considering moving. Where to? Lots of places. What else could be in this list of negativities? Probably a lot. These are challenging times, no doubt about it.

In lighter news, the major stock indexes are positive for the year after brutal losses during Spring. We’ve discussed previously how this rally has been due to a variety reasons but led by a relatively small number of stocks. The so-called FANG+ index is a good example. It’s made up of Facebook, Amazon, Netflix, Google, and includes stocks like Apple and Tesla. This index has doubled in value since the March lows. The latter two companies have now split their stock after a massive runup of 75% and nearly 500% year-to-date, respectively. Exuberance for certain companies seems to be getting irrational, so to speak, especially since a surprising number of high-quality stocks are still down for the year. But again, there are a variety of reasons for this and they’re not all crazy.

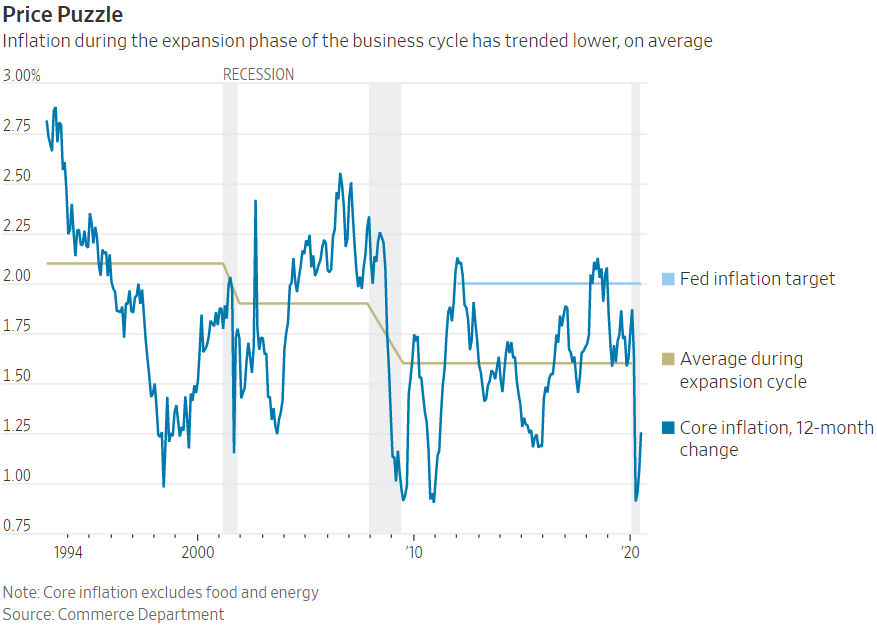

One reason is news from the Federal Reserve last week. The central bank announced changes to how it views its inflation-fighting mandate (it has two mandates - the other is to promote maximum employment). We need some inflation to keep the lights on in our economy, just not too much. We also need the Fed to help us expect where inflation might be headed.

To help set clearer expectations, the Fed announced a specific target for annual core inflation (“core” removes food and energy prices) of 2% back in 2012. The problem, of course, is that since then our economy hit the target just a couple of times and only briefly (see the chart below from The Wall Street Journal). This, after the Fed added gobs and gobs of money to the financial system coming out of the Great Recession. Perhaps the Fed wasn’t being aggressive enough? Perhaps the focus needed to shift?

Well, last week the Fed announced its findings after looking at these issues as part of a review it began last year. It’s main outcome: Going forward the Fed will treat its inflation target as a longer-term average, letting inflation run higher for a time to balance out below-target periods. This is important because the Fed has already said it plans to keep interest rates low for a year or so as we emerge from the virus-induced recession. This change means that low rates could last much longer than that. The Fed may also get aggressive in pushing Congress for more stimulus spending and other regulatory changes.

All of this should stimulate the economy and continue to underpin the stock market (as of this writing on Monday the S&P 500 just ended its best August in decades). Low rates also punish conservative savers and an overly accommodative Fed can help create asset bubbles, so “low for longer” isn’t without risk. But we’re still digging ourselves out of an economic hole and need all the help we can get.

It’s tough out there in many ways right now, so I think it’s good to know that our nation’s central bank is innovating to help support the economy. They can’t find a coronavirus vaccine, re-open a closed business, or put out wildfires, but they can make borrowing money as cheap as possible. The Fed is also looking into how it can impact the social justice discussion, so that’s positive too. Let’s take good news where we can get it, right?

Last week we looked at some of the issues related to relocating amid all the uncertainty we’re facing. This is a popular topic these days. We focused on the question of selling your home here and transferring your equity to the new location, often leaving you with a good amount of cash.

We also touched on the idea of renting in your new location. Although this is likely anathema to many long-time homeowners (myself included), renting for a while has its benefits. The idea is to give yourself space to figure things out, investigate the new area and decide where you really want to be before pulling the trigger on buying a home. It takes time to determine which side of town you like best, the traffic patterns, where the nice parks are, and so forth. And since many housing markets around the country aren’t as active as ours, you’ll want to avoid feeling stuck in a hastily bought home in a less-than-ideal location.

Zillow, for example, says that on average nationally it takes about two to three months to sell a home (including the escrow period). Our area typically takes less than two. But beachy areas in Florida and South Carolina can take four months or more. Also, some of these markets are currently categorized as “hot” but are expected to flatten out or decline over the next year. So, while it’s possible to sell for a profit if you realize you made a mistake, it’s more likely you’ll need to hang onto your new home for a while. I think it pays to be cautious by trying to rent before buying unless you already know the area.

But what to rent and how? While it might seem obvious, this isn’t a time to think about being on vacation. If you need a vacation, take one. You’ll want to rent as if you’re living in the area full time. This means finding a rental that’s like a home in your target purchase price range and, ideally, even in your target neighborhood. In other words, no beachfront condos with amazing views unless that’s what you’ll be buying.

Last week’s two-day drop in the stock market caught a lot of people off guard and it’s continuing this morning after the holiday weekend. Stocks had been on a tear for a while and some investors were getting a little too complacent. Sounds familiar, right? Periods of relative calm followed by volatility slapping you in the face – that’s been typical market behavior in recent years and is common over the long-term. But it feels worse when markets get extra frothy based on short-termism and thin news.

An example of this short-term thinking is how day trading is coming back into fashion. In recent months “retail” traders have been plowing money into the big tech names, helping to drive prices up to nosebleed levels for certain stocks. The popularity of the Robinhood “freemium” trading platform illustrates this point. The firm makes it incredibly easy (maybe too easy) to buy shares of stock and reported over 4 million trades per day in June, eclipsing more established firms like TD Ameritrade and Schwab. This followed a large spike in trading on the platform during the early stages of the pandemic.

These numbers are reported with a lag, but we can assume this activity continued through the summer as a relative handful of stocks rode the wave of popularity. The narrative here is that younger unemployed folks were bored during the shutdown and started trading stocks with their stimulus money. They did well by getting lucky and got too enthusiastic. That seems overly pessimistic and a little harsh, but I can imagine many of these short-term traders getting caught unawares and dumping shares in recent days. That, plus the rapidly shifting sentiment of computer algorithms and other speculators who make up much of the day-to-day on Wall St, was certainly sufficient to blow some of the froth off tech stocks.

So, in addition to everything else impacting stock prices these days we have to add newbies with itchy trigger fingers trading stocks on their iPhones. At least it provides a clear example of what not to do. Speculation versus long-term investing; know the difference!

Another factor driving stock prices lately was news that Apple and Tesla were splitting their stock. An abundance of splits helped fuel the 90’s tech bubble but had fallen out of favor in recent years. The current price slide notwithstanding, the split news had a big impact on each company’s share price, so it’s possible more companies will want to split their stock. If so, this could be a tailwind for the markets as we emerge from recession.

Along those lines let’s review a few paragraphs from my research partners at Bespoke Investment Group, in which they look at the recent Apple and Tesla splits and what they might say about the makeup of the market.

In recent months Congress and the Federal Reserve have been “printing” trillions of dollars in response to the coronavirus pandemic. That old saying of “a billion here, a billion there, and pretty soon you’re talking about real money” now needs a “t” in front of it. With numbers this large it’s reasonable to assume all that money sloshing around the economy would eventually cause inflation. It could even be unaffordable and somehow wrong, depending on your choice of commentary.

It’s in this context that I recently read The Deficit Myth, by Stephanie Kelton, as part of a book club for financial planners (sounds like a real barn burner, right?). The book had been in progress for some time but was published right as the pandemic was revving up in March. The timing was a lucky coincidence for the author because the topic, Modern Monetary Theory, speaks to just about everything we’re hearing these days related to government spending, deficits, the debt, and the affordability of large amounts of economic stimulus.

MMT, as it’s known, is a big topic and I’ll only touch on some of it in this post. It has also been politicized in some circles for reasons that will become obvious the more you learn about it. As you’d correctly assume, I don’t get political in these posts so none of what I write below should be misconstrued as such.

Probably the most interesting thing to me about MMT as a concept is that it’s, as the name implies, an attempt to modernize the way we think about money at the federal government level. The U.S. has been completely off the gold standard since the 1970’s but most of our elected officials still think of our currency and federal spending in relatively archaic terms, according to MMT economists. It’s the way I learned it originally as well.