It seems as if a recession has been right around the corner for many months now, if not a year or so. First a recession was inevitable given the run-up in inflation we saw last year. Then it was imminent due to the Fed raising interest rates so much so quickly to fight inflation. And then bank failures earlier this year were supposed to cause banks to stop lending and consumers to stop spending, crashing our economy.

Well, so far an outright recession continues to only loom on the horizon. According to experts, recession chances for the rest of this year have fallen to 33% and 59% by next summer.

Maybe this is what a soft landing looks like. The term originated in this context during the Nixon-era economy and following the 1969 moon landing, according to the Wall Street Journal. A soft landing is the elusive state where a too-hot economy is cooled down by higher interest rates while still avoiding a recession. Historically, the Fed has rarely been able to engineer this outcome because it usually raises rates too quickly and shocks the system. But maybe a soft landing is more possible in the post-Covid world, whatever that means. Fed Chair Jerome Powell has himself recently acknowledged the Fed “is navigating by the stars under cloudy skies”, so uncertainty around all this is high. (And at least he’s honest about what he doesn’t know, which is a good sign.)

Technically, the Business Cycle Dating Committee within the National Bureau of Economic Research is the government office that “calls” recessions and doesn’t do so until well after the fact. However, the various data they tend to watch seem to be trending fine. GDP growth appears stable. Unemployment is very low. Inflation has been reducing the purchasing power of wages, but CPI, the typical inflation measure, has been trending lower for months. NBER looks at other indicators too but tries to pinpoint when the economy has peaked before suffering a meaningful decline in activity lasting at least several months, which bottoms out before improving. Their analysis requires a lot of data that’s only available in hindsight, so we often find out we’ve been in a recession after it’s already over.

How helpful is that? I contend that whether our economy falls into recession or not is largely academic. It’s important to know but not especially relevant for most Americans. The stock and bond markets work well ahead of the economists at NBER and households, all of us, live it day to day anyway. We have to deal with the impact of inflation and higher interests rates in real time, so economists can call it whatever and whenever they like. And parts of the economy can do fine during a recession while others get their teeth kicked in; the impact isn’t felt uniformly. Various surveys of regular Americans show that anxiety about the economy and inflation is already high and disproportionately felt by those at the lower end of the income spectrum. People say they’re planning to spend less but not yet. It’s sort of a variation on the acronym NIMBY… my backyard is fine, but everyone else’s looks horrible. This dynamic has to be part of the reason why the economy is still doing well.

My point isn’t to diminish the work of NBER and other economists, but to suggest that our own household trends often trump those of the broader economy. The takeaway is that regardless of the macro environment we should frequently assess the risks we face at the micro level in our own households should the economy slow.

Here's a handful of categories to consider whenever experts wring their hands about recession risk.

What’s my liquidity position?

If my sector and industry or yours, whether it be construction, retail, and so forth, gets hit especially hard during a recession, do I have enough cash to get by for how long… six months, a year? Is this cash-cash, as I call it, that’s available in a bank or brokerage account, or is it stashed in my 401(k) and accessing it would come with taxes and maybe a penalty? Conduct a mental fire drill to determine how much cash you can get ahold of in what timeframe and with what, if any, sort of penalty. Is it enough for whatever doomsday scenario you have in mind?

What’s my debt situation?

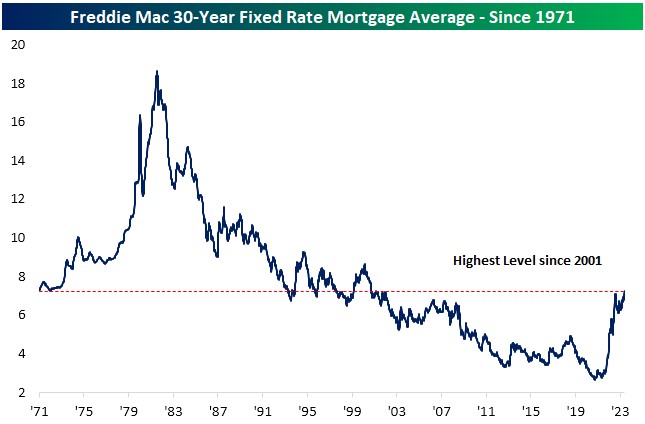

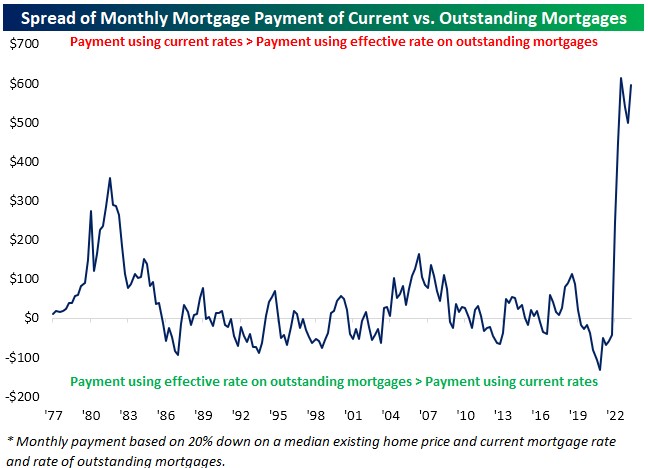

Rates have already gone up, of course, so any adjustable-rate debt is likely resetting and getting more expensive in a process limited only by annual caps. If I had any adjustable-rate debt, I’d evaluate refinancing into something fixed while the economy, and presumably my little corner of it, is still strong. The Fed is in pause mode with rates and that’s expected to continue when they meet again this week, so I could hold out to refi based on a guess about when rates go down. But then I remind myself that rates would likely only be lower if we’re in a recession and my access to credit might have changed.

What’s my work situation?

Being self-employed has it’s benefits but when business conditions suffer I can’t simply rely on someone else to pay me. I also can’t lay myself off to save the business some money. Regardless, gauging the solidity of our prospects is a moving target, at least to some degree, and gets back to considering our liquidity and debt positions mentioned above. Having readily accessible savings coupled with a manageable and sustainable debt load should take the edge off of getting fewer hours at work or even having to look for a new job.

How are my investments situated?

Do I have more than 5-10% of my long-term savings invested in one company? Am I loaded up too much in one sector of the economy that could suffer during a recession, such as Technology or Consumer Discretionary? Are there other parts of my portfolio that are too risky? Try to shore up what appears shaky but be wary of making wholesale changes without good reason. While it’s valuable to review how our investments are situated we should avoid being overly reactionary.

If you have good answers to these sorts of questions you’ll be able to weather most of what the economy throws at you. If not, as is the case with many of us, you’ll have more time to put your house in order if you start now.

Have questions? Ask us. We can help.

- Created on .