Inflation on the Menu

"Inflation hasn't ruined everything. A dime can still be used as a screwdriver." - H. Jackson Brown, Jr.

"It's tough to make predictions, especially about the future." - Yogi Berra

The Federal Reserve is meeting today and tomorrow for it’s regular review of the economy and what, if anything, to do about it. This is also one of the meetings when the Fed announces its member’s economic projections. Nobody expects the Fed to raise interest rates at this meeting, but everybody will be watching and listening for clues on when they plan to start doing so, and if they’ll begin earlier than anticipated.

As we’ve discussed before, the Fed is viewing the recent spike of inflation as something they’ve planned on, a goal realized, and something that’s also likely to be short lived. In other words, the Fed added a bunch of fuel to stoke the economy’s fire during the worst of the pandemic and a flareup was to be expected. Eventually the flames will settle, and we’ll be back to the slower burn we’ve grown accustomed to. Or at least that’s the plan. The Fed has a tough job, no doubt about it.

It took a while to kick in, of course, but we now see the fiery part of this playing out around us every day. Grocery and gas prices seem higher. New and used cars and trucks are more expensive. Housing costs are soaring. There are tons of anecdotes of increased demand just as a wide variety of supply chains across the globe struggle to keep up. Name the industry and it’s being impacted. There are even reports of long lines awaiting visitors at national parks. Lots of activity after a prolonged lack of it equals inflationary pressures, but will it last?

Across the country people (generally speaking) have less debt, more cash, and are feeling the so-called wealth affect that comes from soaring home and stock market values. Much of this is psychological, but how we feel about the economy is important because it impacts how we spend. And if consumers feel like prices will be more expensive in the future, they’ll buy now, stoking more inflation.

Workers are also feeling their oats a bit as our economy picks up. Nationally, the unemployment rate has continued to decline in part because more people are dropping out of the labor force. They’re retiring early, exploring opportunities, taking a crack at the Great American Novel from a beach in Fiji, and so forth. And a growing number of those who plan to remain employed are switching jobs.

While all this is important for the economy and impacts inflation, the latter point, the job switching, is something the Fed watches closely. The so-called quit rate is measured in the Job Opening & Labor Turnover Survey (JOLTS) and is a key indicator for how healthy the labor market is. It’s seen as positive when workers feel confident enough to jump ship and head to another employer. And since they typically do this for more money, this activity helps drive wage growth within the economy and has a direct impact on inflation. A high quit rate isn’t a problem if it’s a blip, but if it persists those extra costs for employers have to go somewhere, like increased prices for consumers.

This week I wanted to share some snippets of analysis and a few charts about JOLTS and the employment situation from my research partners at Bespoke Investment Group. Yes, looking at JOLTS data is a bit wonky, but the Fed will undoubtedly be looking at the same information, so it’s helpful to have a general understanding of the numbers.

Continue reading...

From Bespoke (emphasis mine):

This week’s Job Openings & Labor Turnover Survey data for April from the BLS [Bureau of Labor Statistics] blew the doors off expectations, with a huge 12.5% increase in private openings after an 8.4% increase in March.

Hiring rates are accelerating and discharge/layoff rates are at record lows, but quit rates are soaring as workers swap jobs to take advantage of higher wage rates.

All-told, at the top level, the JOLTS data shows a labor market that is reorganizing itself in the wake of the pandemic, sorting through the chaotic process of re-setting wages higher and re-allocating workers across businesses and industries.

The extremely high turnover that the JOLTS data shows is one reason that wage growth has been so high of late.

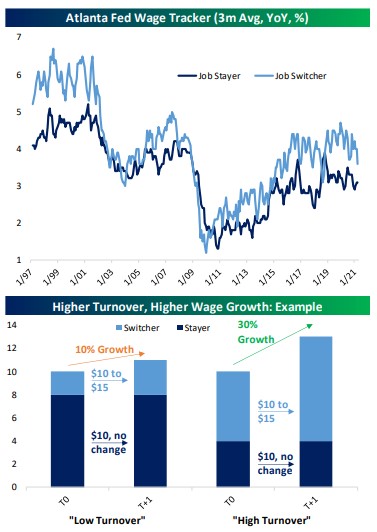

We can see this in the Atlanta Fed wage growth tracker data in the first chart [below].

This is because the wage offered to attract a new employee is the marginal wage for all workers, which must by definition be higher than the average wage for equivalent workers if employment is rising and unemployment is falling (as is typically the case).

To use a numerical example, the chart [below] assumes workers who do not switch jobs receive no change in pay, while workers who do switch move from $10 to $15 per hour.

The switching behavior generates 10% growth in total average wages (20% of workers switch, getting 50% more pay).

But if we make the same assumption around switching, but instead assume 60% of workers switch, average wages are now up 30% over the period of the switching.

This is not meant to be a representative model for the actual fraction of workers switching jobs, actual wage growth for switchers, or total wage growth presently, but it does help to illustrate how more job switching tends to lead to more wage growth.

We can also assume that in a labor market where lots of workers are switching to new jobs, the wedge between the pre-switch and post-switch wages will be much thicker; workers will be given a greater incentive to switch than in a job market where employers don’t have to compete for labor resources.

Of course, this state of affairs won’t necessarily last forever, but it’s possible that we could be seeing a new and higher equilibrium for both turnover of workers and the wedge between current wages and the new wages available to workers when they switch jobs. In that case, a higher base rate for inflation is an inevitable result as labor costs get passed on to consumers.

Also from Bespoke regarding postings of open job opportunities from the employment website, Indeed:

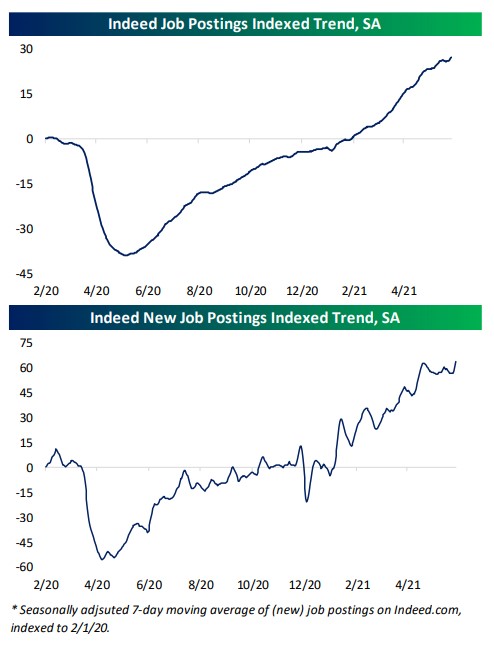

While the JOLTS report was impressive, the data is somewhat lagged. Job search engine Indeed.com provides higher frequency data on postings updated through the end of May.

The data shows seasonally adjusted job postings and new job postings indexed to February 2020.

As shown in the first chart below, postings nationally were 27.25% above the February baseline as of May 28th; a continuation of the steady rebound in the jobs market of the past year.

As for new job postings, things picked up sharply in late May and are running at an impressive pace of 63.42% above the baseline after a bit of a plateau in April and the first half of May.

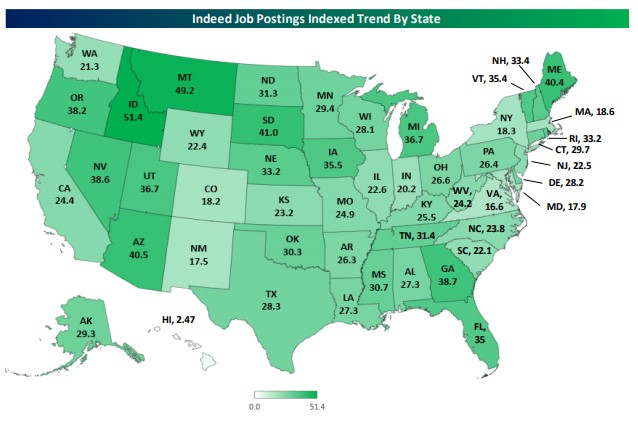

Indeed also breaks down their data by geography on a state level and by the largest metro areas.

Not only does every state now have more job postings than February 2020 right before the pandemic, but every major metro area also has a positive reading.

That compares to our last few updates of this data in which travel centric geographies like Hawaii, and more specifically the Honolulu metro area, were outliers as being one of the only parts of the country to have fewer postings than February 2020 levels.

Another theme of the past year has been smaller metro areas outpacing larger metros in terms of job growth. That has continued to be the case with the average reading for metros with more than 4 million people up 26% whereas the smallest metros (under 1 million) are up 33.5%.

As you can see in the map below, employers are looking for workers everywhere at an incredibly high level. The numbers shown for each state are where job postings stand in the most recent release relative to where they stood in February 2020 on a percentage basis.

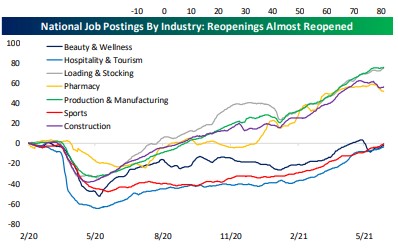

Indeed also breaks down postings by industry to see which are ramping up hiring fastest.

Here’s a link to Bespoke’s website if you’d like to check them out.

https://www.bespokepremium.com/interactive/

Have questions? Ask me. I can help.

- Created on .