Updates on a Few Areas

This has certainly been a rocky year so far for investors. It seems like it’s been a while, so I wanted to give you a quick update on where we stand in a few areas.

Inflation –

Official numbers for August that came out this morning were expected to show inflation declining a bit because oil and gasoline prices have been dropping. But this was more than offset by increases in housing, food, and medical care, according to the Bureau of Labor Statistics. For example, food prices were up 11.4% in the past 12 months, the largest increase in over 40 years. All told, inflation was running at an 8.3% annual rate in August.

Stock and bond markets were set to rise with the expected inflation decline, so news of continued high inflation turned the stock market on its heel.

The Markets –

Year-to-date through last week the S&P 500, the standard index for US stocks, was down almost 14%. The tech-heavy NASDAQ index was down 22%. Foreign stocks, both developed and emerging markets, are down 19%. And medium-term bonds, what most people have in their portfolios, are down maybe 8-15% depending on type.

The worst performing sectors were Communication Services and Technology, down 28% and 21%, respectively. Had you perfect foresight (or dumb luck) to be all-in on the Energy sector at the just-right time, you’d be up 48% this year. That sector along with Utilities, which is up nearly 10%, are the only two positive sectors out of the 11 that make up the US stock market.

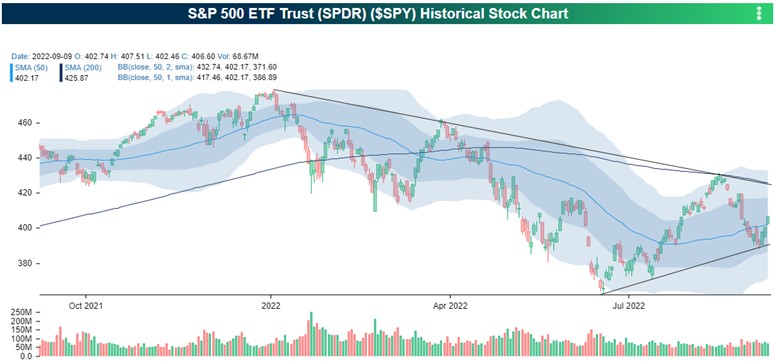

Stocks have been rangebound lately, as market technicians say, moving up and down between shorter-term averages but lacking the oomph to take lasting steps forward.

The following chart comes from my research partners at Bespoke Investment Group. (The small print isn’t that important, so don’t worry if you can’t read it. Just focus on the trend lines to the right.)

Gyrations in the markets have largely been caused by fears about the Federal Reserve raising interest rates too quickly to fight off inflation and sending the economy into a recession. And these fears were stoked yet again this morning with inflation running hotter than anticipated. Fundamentally, the various narratives around this have been about jobs and the health of the consumer, and how this could change as the Fed raises rates.

Jobs and the Consumer

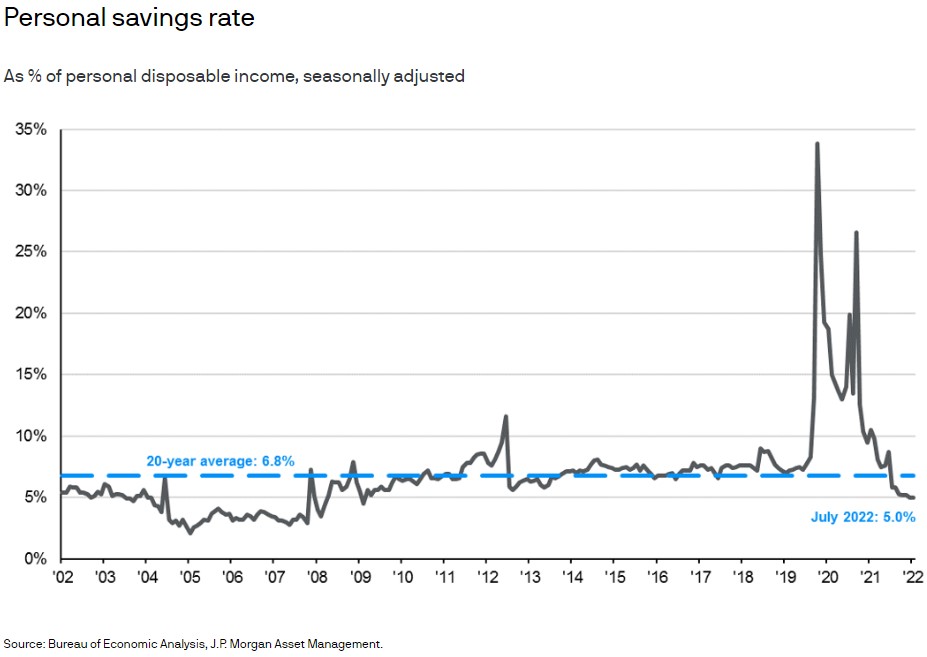

Here are some updates from JP Morgan Chase. The big bank has an interesting perspective on consumption because they can analyze government data like everyone else, but can also look into bank customer transactions, balances, credit use, and so forth.

This first chart shows how much Americans are saving and how this has changed over time. You’ll clearly see the massive spikes caused by staying home and changes in buying habits during the pandemic coupled with the timing of government stimulus. Payments stopped abruptly late last year, and we can see how that cratered the savings rate. Many economists assume the savings rate won’t deteriorate much further if the job market remains solid, but that’s obviously a big open question.

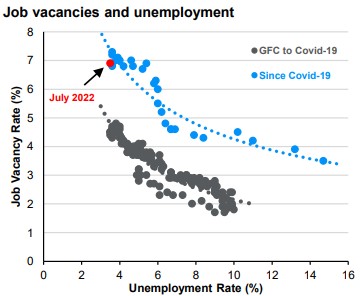

With the Fed trying to slow the economy to fight inflation, how long before the job market starts getting squeezed? This next chart shows something called the Beveridge Curve. While this might sound like a visual representation of the angle at which one’s beer meets one’s mouth, it actually shows the relationship of job openings to the unemployment rate. This concept is important because it’s often pointed to by those expecting a soft-landing for the economy versus outright recession.

The main takeaway from this comparison between the before-times of the Great Financial Crisis up to Covid, and then post-Covid, is there are a lot more available jobs now and the unemployment rate is much lower than when we were coming out of the GFC. Seems positive, right? Soft-landing proponents see the job market as having room to slow before becoming a drag on growth. And they’re quick to point out that we’ve never had a recession when the job market has been strong. But naysayers suggest that the Beveridge Curve, as with many traditional economic metrics post-Covid, means less because much of the job market remains destabilized. Only time and data will tell who’s right.

The Housing Market and Interest Rates –

Mortgage rates are linked to the bond market. The 10yr Treasury bond, a key benchmark, rose again last week to about 3.3% after a volatile summer. This brought the average rate on a new 30yr fixed mortgage to about 6.1%, a hairsbreadth below a summer high of 6.2%. That’s double where it was this time last year. This increase in rates has pummeled the refi industry and is adding a lot of pressure to housing market.

According to Redfin, there’s been a drop-off in a range of real estate activity. Demand still seems to be there but with still-elevated house prices and rising cost of debt, more buyers are feeling priced out of the market (again). As with the Beveridge Curve example, perhaps there’s room for home prices to move lower without impacting the so-called wealth effect (and, by extension, consumer sentiment) too much. Add that to the list of open questions.

Here’s a link to the Redfin article if you’d like more detail.

https://www.redfin.com/news/housing-market-update-surging-rates-slow-buying-and-selling/

What to make of all this? A lot of these questions about interest rates, the job market, housing, and recession are likely to carry over into next year. In the meantime I’ll be optimistic and say I’m in the soft-landing camp, although the realist in me is barking a bit. It can be hard to stay disciplined in the face of uncertainty, so don’t let your questions fester. We can discuss your situation and what, if anything, that you could or should be doing differently. Otherwise, it's steady-as-she-goes, as hard as that can be at times.

Have questions? Ask me. I can help.

- Created on .