Maybe next year…

For many months analysts have been saying a recession is on the horizon. They’ve detailed the reasons why and I’ve reiterated certain points at various times. Recession should occur within such and such months because it always has when indicators X, Y, and Z have looked like this, and so forth. I can’t tell you how many comparison charts I’ve seen in the past couple of years that offer a compelling case for a near-term recession. It’s out there somewhere, no doubt about it. But, as explorers of old quickly figured out, the horizon line never gets any closer.

Even though our economy continues to sail along nicely, dour predictions continue. Current expectations are for a broad-based slowdown sometime during the second half of next year. Whenever a recession occurs, and one will occur eventually because our economy is cyclical, what’s more interesting right now are the variety of explanations for why our economy has been so resilient.

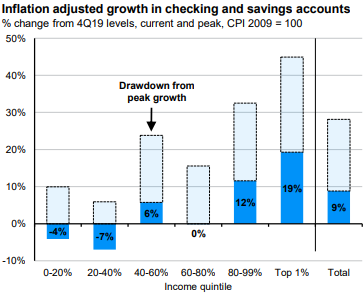

One of the charts I shared last week offered a reason: wealthier households flush with cash are still happily spending. This surprised analysts because the consumer is supposed to be so unhealthy right now. Government subsidies ending and student loan payments resuming were supposed to cause consumption problems, and they have. However, the thinking is that a host of other factors, from homeowners having locked in low mortgage rates as incomes and home equity rose, along with remnants of Covid-era stimulus payments, continue to free up spending cash for many (but not all) households.

Here's a look at that chart from JPMorgan again.

Then this week it’s another article from the Wall Street Journal about how Americans can’t stop spending and offers reasons why with profiles of real people. This is fascinating because it dovetails perfectly with the chart from last week.

I think the bottom line is that economists and analysts are leaning on this sort of data in real time because, as with so much else post-pandemic, past isn’t always prologue. Eventually consumers will spend less and that will impact the economy. Until then we seem to be in good shape. But how long that lasts is truly anybody’s guess.

I’m only including snippets below but a link to the article will be at the end. As before, let me know if you’d like the whole thing and I can send it to you from my account if you run into the WSJ’s paywall.

Snippets from the WSJ…

Americans’ prolonged spending spree has confounded economists and resulted in a surging U.S. economy. What’s keeping their feet off the brakes?

A strong labor market, resilient savings stockpiles and rising values of their homes have consumers feeling good and willing to spend. Despite complaints about high prices, they are taking their children to concerts, packing movie theaters, booking luxury vacations, buying cars and covering the costs of rent and dinners out.

Strong spending caused economists to be wrong about a 2023 recession, though they still predict cutbacks ahead.

There are signs that Americans’ elevated spending habits aren’t sustainable. Some 60% of Americans said they have fallen behind on emergency savings this year, according to a Bankrate survey. In September, they saved 3.4% of their income, about half the rate they saved in the fall of 2019, the Commerce Department said. And long-term interest rates—which make it more expensive to buy homes and cars and to borrow money—may only now be reaching the point where they will slow Americans’ roll.

Nevertheless, many of the factors that have driven the 2023 spending binge remain intact.

Americans are feeling rightfully confident about their job prospects and paychecks.

“The strength of the labor market and the strength of household balance sheets has helped Americans weather some of that storm” of inflation, said Daniel Zhao, an economist at the jobs website Glassdoor.

The cost of financing a home has marched higher since 2021, putting the average 30-year fixed mortgage near 8% and keeping many would-be buyers on the sidelines. Plenty of Americans who locked in low mortgage rates, though, have extra cash.

Roughly 90% of mortgaged homes have a rate below 6%, according to calculations from Mark Fleming, chief economist at First American Financial Corp. About two-thirds of American households own their home, according to the Census Bureau.

The pandemic gave Americans the opportunity to stockpile savings, and many are still benefiting from that cushion.

Overall, Americans accumulated more than $2 trillion in savings above the prepandemic trend by August 2021, according to estimates from the Federal Reserve Bank of San Francisco. Recent estimates of the remaining excess pandemic savings range from $190 billion from the San Francisco Fed to between $400 billion and $1.3 trillion from economists at RSM.

Pandemic-era savings also went to paying down debt, said Jonathan Parker, a professor of finance at MIT Sloan. That gives consumers room to borrow, even if they have burned through some of the extra savings, he said, adding that, “People have a fair bit of debt capacity before they start hitting constraints.”

Prices for many items are rising more slowly than they were a year ago. But consumers remain fixated on how much lower they were before the pandemic, a mindset that may be driving some people to buy a car or fix their home while they can still afford it.

The experience economy continues to boom, with Delta Air Lines reporting a record 30% jump in earnings in the quarter ended in September and Ticketmaster selling more than 295 million event tickets in the first six months of 2023, up nearly 18% year over year.

Again, here’s the link to the article that includes profiles and some interesting charts.

https://www.wsj.com/economy/consumers/5-things-us-economy-8a588781?mod=hp_trending_now_article_pos3

Have questions? Ask us. We can help.

- Created on .