More Info About Retirement

Before we begin, just a heads up that I’ll be missing next week’s post but will be back at it the following week.

Staying with the retirement theme from last week, let’s review the annual update to the Employee Benefit Research Institute’s Retirement Confidence Survey. Many of the sponsors of this survey are insurance companies or those engaged in selling annuities so there’s that bent to the research if you dig into it, but the report is still a good temperature check on how Americans are planning for and living in retirement.

I’m providing a link to the EBRI site below and to another industry-related site that summarizes the findings. This way you can dive into the details if you’re interested. Otherwise, here are some notes and charts that I think are most relevant.

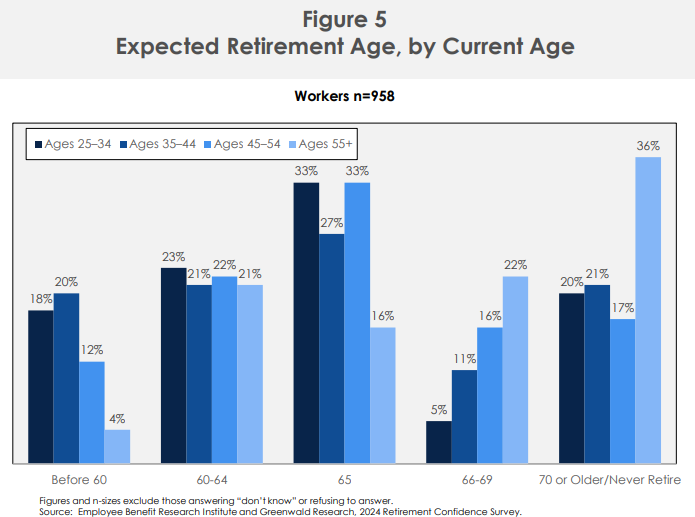

When People Plan to Retire

You’ll see in the chart below that workers younger than age 55 most often report a target retirement age of 65. This has to be arbitrary and more or less tied to that age being the original Social Security full retirement age. Work until 65 and then retire – it’s baked into our cultural perspective. Why else would so many younger workers peg that age versus retiring between 66 and 69? What’s ironic is how the Social Security baseline age is now 67 and will likely be closer to 70 when younger people retire anyway. Interestingly, there’s a sizeable contingent of those over 55 who say they plan to work until at least age 70 or may never retire. I couldn’t tell from the report if this latter group skewed heavily to those with less savings, but it dovetails with our recent discussion of high labor force participation rates for older people.

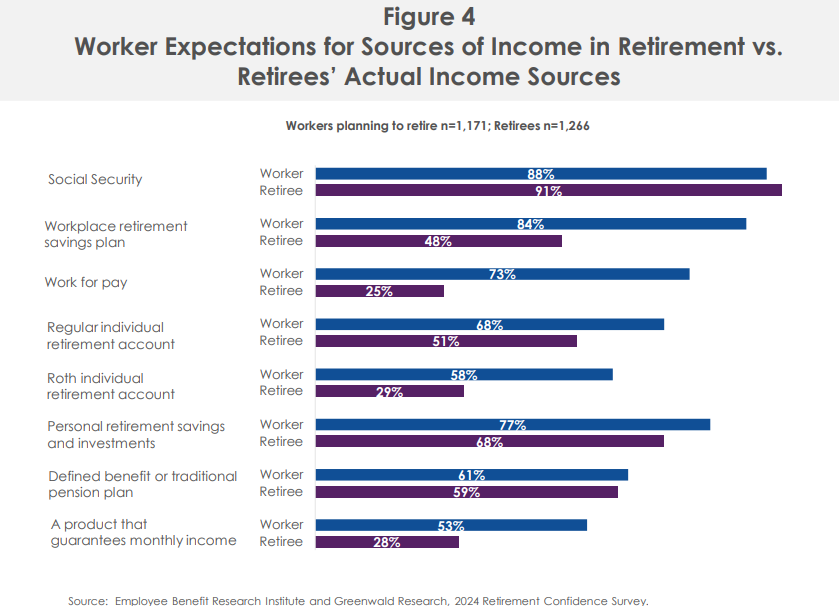

Income During Retirement

The report compares current workers and retirees. Both plan to and actually rely on Social Security as an income source. However, more workers plan to leverage their workplace plan while retirees say they use more personal retirement savings and investments for retirement income. I’m not sure if that means retirees have the old workplace plan and aren’t using it as much or if they’ve moved the money into an IRA and that makes it “personal” in the context of the report. Whichever it is, some form of personal savings is obviously necessary to enable retirement because Social Security isn’t meant for full income replacement.

Some of the expectations versus actual results were interesting, such as with “Work for Pay”. Almost three quarters of workers report planning to work during retirement versus 25% of current retirees who actually work. Perhaps during mid-career it’s easier to think of a working retirement in the hypothetical sense but actually doing it after a full career is something else entirely. Otherwise, using annuities (or “a product that guarantees monthly income” – they do whatever they can to avoid saying annuity) is popular for planning but not necessarily for doing. Also in that camp were relying on disability benefits and a personal support network in retirement. These latter two didn’t show up in the chart below but I thought it interesting that they were included in the survey at all.

Other notes –

Almost two-thirds of workers feel confident or very confident about their ability to live comfortably in retirement. But nearly as many say preparing for retirement stresses them out!

Maybe this stress is due to nearly two-thirds of workers reporting having less than $250,000 saved, and a sizeable chunk of these folks having less than $25,000. How can so many of these workers report being so confident?

More than half of respondents said they are working with a professional advisor or at least plan to. That’s good so long as they get high quality objective advice from a “professional”, but I do worry about that. Obviously my opinion is biased, but how can workers receive the good advice they expect when the country’s “advisor” population is primarily comprised of salespeople? Otherwise, it’s a grab bag of information sources including family and friends (the most popular option for financial advice, by the way), employer-provided education, financial gurus, and even ChatGPT.

Debt, and large amounts of it, was reported as a major hindrance to confidence levels for workers and retirees. Debt can be a helpful tool, think of Archimedes and his lever. But overusing debt is one of those problems that only shows up after the fact and can be incredibly damaging to your financial health. Make paying down/paying off debt part of your retirement planning strategy and you’ll have a head start on being happier than two-thirds of people who respond to surveys like this.

Here are the links that I mentioned above.

https://www.ebri.org/retirement/retirement-confidence-survey

Have questions? Ask us. We can help.

- Created on .