Student Loans and Home Ownership

This week let’s look at a couple of important issues getting some press lately: rising student loan delinquencies and the decreasing affordability of home ownership. Both aren’t necessarily new problems but both keep getting worse.

Student loan repayment was mostly paused early in the pandemic and became a political football in the years since. Understandably, millions of borrowers stopped paying on their loans back then and got used to it. This forbearance ended over a year ago with a one-year “onramp” allowing borrowers time to restart making payments without having late payments hit their credit report.

That onramp ended last October and now we see reports for the first quarter of 2025 showing that about a quarter of borrowers who were required to make payments were behind during Q1. This means, among other things, that these borrowers are seeing big declines in their credit scores.

According to a report by the NY Fed, most newly delinquent borrowers already had poor credit, with scores lower than 620. But a big chunk of borrowers, about 36%, had decent scores in the 620-719 range. Unfortunately both groups saw large credit score declines that rose the higher a borrower’s score was before becoming delinquent. Those 620-719 borrowers, for example, saw an average decline of 140 points – something that has real-world implications like dropping them into subprime auto loan territory and takes a few months to a few years to recover from. The report also said most delinquent borrowers are in the south and over age 40, and more older borrowers were seriously past due at 90+ days, so they’re having a tough time.

Making matters worse for seriously delinquent borrowers is that the US Dept of Education and the US Treasury have restarted the collection process this month. This includes garnishing wages, Social Security payments, even claiming would-be tax refunds.

If you or someone you know is in this predicament, one idea is to look at your retirement savings or other investments (assuming these exist) for cash to help pay off or pay down student loan debt. Maybe you’re out of work or your taxable income is otherwise a lot lower than normal. You’ll want to talk with a tax person as well, but you could take a distribution from your account, pay the tax and perhaps also a penalty. This would hurt your savings but taking the hit might ultimately be better than paying excess interest and continuing to damage your credit score. You could also look at consolidating your debt somewhere, but that can be a nonstarter if you’re already having trouble making your payments.

Okay, the second item is the affordability of home ownership. Home ownership peaked nationally at almost 70% of the population in 2004 but the average since at least 1960 is still over 60%. It’s about 55% in California and 75% in less expensive states like South Carolina, according to the US Census Bureau. Still, affordability is at a 35-year low across the country.

Inventory is low compared to population growth so prices are high. According to JPMorgan and Zillow, nationally we have a shortage of roughly 4.5 million homes based on population growth. That sounds funny when compared to news stories about the housing market slowing down lately due to rising inventory, but it’s different perspectives covering different timeframes.

Mortgage rates are at about the long-term average of 7% but still seem expensive compared to recent history. Underwriting standards are stringent, with about $110,000 of annual income needed to qualify to buy the average home in most states, according to a report from Bankrate. Add that to higher purchase prices and private mortgage insurance on first-time homebuyer programs and home ownership can be prohibitively expensive, especially for first-timers.

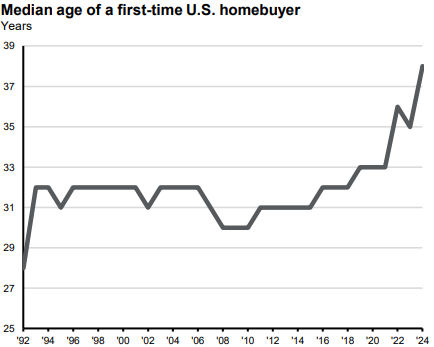

Among other things, this means buyers have to be a lot more established and usually older before the dream of home ownership can become reality. The following chart from JPMorgan shows this increase over time.

Reading about this reminded me of when my girlfriend (and long since my wife) and I bought our first house in the late-90’s at age 19, well below the average at the time shown in the chart and half of what it is currently. I think we put down 3-5% on an old bungalow in Sonoma, CA that may not have had any right angles in it. Our loan was part of an FHA first-time homebuyer program. I recall our interest rate being 7.5% and, plus the private mortgage insurance and other monthly costs, we barely scraped by. Still, we loved being homeowners. We did a ton of repairs on our own, learned from mistakes, and eventually sold the house to start the typical move-up process. We’ve benefitted from being owners versus renters over three decades but earned every penny through sacrifice and stress.

There are many financial planning issues related to home ownership but I’ll close with the thought that home ownership isn’t for everyone and doesn’t have to be. Some people will never afford to own a home and others might simply prefer not to. It’s just kind of sad that homeownership seems to be out of reach for so many.

Have questions? Ask us. We can help.

- Created on .