Looming Tariff Concerns

I’ve written before about being selective in the voices I pay attention to when it comes to the economy, markets, and so forth. These days we need beacons of rationality in what can otherwise be a sea of disfunction. Anyway, two of these are Bespoke Investment Group and certain analysis and information from JPMorgan. Bespoke is a subscription service I’ve been using for years that provides all manner of analysis but really shines when providing broader context. JPMorgan offers macroeconomic commentary from its investment management arm for free to investment advisors.

Both shops had good commentary yesterday regarding the end of the 90-day tariff pause that helped markets recover so quickly from the April lows. That they’re both echoing essentially the same concern about the outlook for tariffs is interesting.

You probably heard about the Trump administration engaging in more rhetoric and a letter writing campaign with our trading partners last week. That caused volatility to perk up again in the markets although investors, at least on average, still assume that tariff numbers being bandied about won’t actually come to fruition. Regardless, real-world tariffs (our effective-rate referenced below) have been rising and will eventually impact corporate profits and inflation, although recent reports have been solid and Consumer Price Index readings have been coming in below consensus estimates.

Maybe actual tariff impacts are just being pushed down the road several months. Are investors being overly optimistic about this, and perhaps also about the likelihood that larger tariffs will actually stick? It’s entirely possible that markets will continue to grind higher from here. But prices are relatively high so it seems best to plan for more market volatility in the weeks and months ahead while all this gets sorted out. Along those lines, let us know if your situation has changed because that could mean adjustments to your investment portfolio. Otherwise, your first approach should be leveraging your plan and trying to ride out volatility.

Here are the notes I mentioned. First from Bespoke and then from JPMorgan.

Consistent with the decisions released so far in July, after the close Friday, the Trump Administration announced a 30% tariff rate for the European Union and Mexico. That rate of course assumes that the tariffs actually go into effect on August 1. […] the market currently prices the odds of full implementation of the August 1 tariffs at less than 10%.

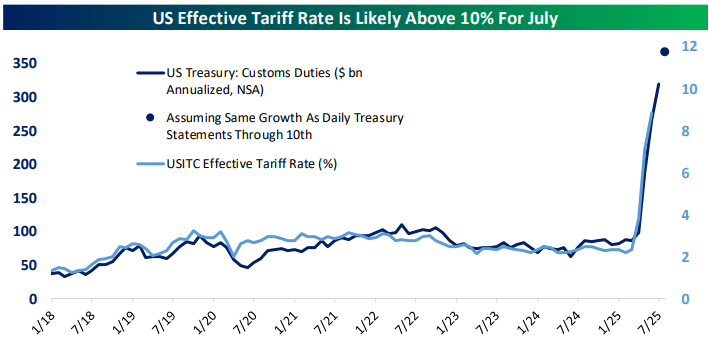

In the background, Friday saw the release of the Monthly Treasury Statement which showed tariff collections of $26.6bn NSA ($320bn annualized) in June. When compared to US International Trade Commission data on the realized effective tariff rate data current through May, we can see that realized tariff collections for the month likely exceeded 10% of imports. We also note that Daily Treasury Statement data current through July 10 is consistent with monthly collections up 15% versus June, which would take the effective rate on imports closer to 12% based on recent history. Again, this is all before the recent wave of letters for new rates effective August 1 (theoretically).

The market will stay at elevated levels as long as marginal buyers are convinced that the rates set out in the letters won’t be the rates that take effect. There is no plausible way the market can trade at 6250 [the S&P 500’s level as of a few days ago] with 30%+ tariffs on Canada, Mexico, and the EU as well as 20%+ tariffs on all other major trading partners. But for those rates not to play out, either a deal needs to be reached or the market would need to sell off; it was market declines that forced a change in approach during April, and it will be market declines that force a change in approach on August 1 as well of no deals can be reached.

We see many investors apply a “it’s all rhetoric” approach to Trump administration policy, and it’s understandable why they do so. Trump himself, let alone other members of his administration, says so much that it’s tempting to discount all the rhetoric as irrelevant. On the other hand, many proposals advocated by Trump in the lead up to the last election that some argued wouldn’t take effect have been borne out. Regardless of whether you think his policies on regulation, taxes, immigration are good or bad, the President has followed through on many that a lot of people assumed he wouldn’t.

The above does not mean that Trump is assured to follow through on his plans to hike tariffs to an effective rate well above 20% on August 1. But the market’s confidence that he won’t is potentially misplaced based on prior experience and is also a signal to Trump that he should follow through. For long-term investors, this is yet another example of why staying invested is so important; there’s no way to model this interplay and over a timescale of years it’s mostly irrelevant. For more tactically oriented investors, the President has created more volatility, but good luck trying to anticipate when and to which sectors the next tape bomb will drop.

From JPMorgan…

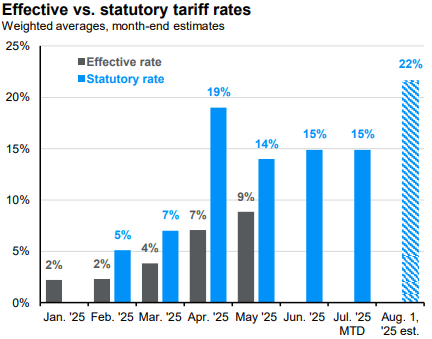

Economic forecasting has been an increasingly tough job due to the ever-evolving tariff landscape. A major source of confusion has been the difference between statutory (or announced) and effective tariff rates. For example, the tariff paid by importers may be 25%, but when you calculate the effective rate by dividing tariff revenues by import values, it often appears lower. This happens due to real-world complexities such as exemptions, quotas, shipping delays, and product mix shifts.

This week's chart illustrates the significant changes in both statutory and effective tariff rates since the start of the year. The gap between these rates is wide due to implementation delays and a dramatic shift in import share composition, both by product and country. Imports from China, which are subject to the highest tariffs at an estimated effective rate of 40%, have plummeted, decreasing by 24% y/y from March to May 2025. In contrast, imports from the Eurozone, now facing an effective tariff of approximately 10%, have surged, largely driven by the frontloading of products like pharmaceuticals.

The data show that importers are actively seeking substitutes from other countries to circumvent these tariffs. The terminal tariff rate is still uncertain, but a rate in the high teens is becoming more likely. The Section 232 [national security-related tariffs] investigations are almost complete, indicating more sectoral tariffs could be introduced, along with the already announced 50% copper tariff. Also, recent negotiations with Vietnam, which initially raised hopes for lower rates, ended with a 20% tariff on products originating in Vietnam, higher than the previously announced 10% during the 90-day pause. This outcome makes other negotiations look less promising. As a result, investors may need to be more cautious and actively manage their exposure to affected companies.

Have questions? Ask us. We can help.

- Created on .