Actual vs Expected

As I mentioned a couple of weeks ago, the inflation impact from new tariffs is taking longer to show up than many speculated back in April. The impacts have been starting to show up, however, at least as of June’s CPI numbers. This is causing further speculation that tariff pressure is building and won’t really start being felt until later this year. Although risk of an outright recession is low, these changes will eventually impact business and consumer spending, causing the economy to slow, and so forth – it’s just a question of by how much and when.

This is also affecting assumptions about when the Fed may reduce interest rates. According to the CME FedWatch tool, there’s very little chance the Fed lowers its rate benchmark at its meeting this week. However, the market is pricing in a couple of rate reductions from September through year-end. The interest rate traders whose actions create these probabilities could be wrong, but it’s a good view of what investors are focusing on right now.

There’s still a lot of uncertainty around all this but news from recent days of “preliminary” trade deals with Japan and the EU helps to reduce tariff-related anxiety somewhat. My understanding is that our average bilateral tariff rate with the EU will go from about 1% last year to 15% on imports and 0% on US exports. Maybe the real-world numbers end up averaging less, but that’s a large increase in a short time on over $6 billion of imports (the total in 2024). Now there’s talk that the Trump administration’s tariff “floor” is 15%. Analysts suggest that 10% and below could be more-or-less absorbed by the economy here and abroad but the higher tariffs go tilts the scale more. Who’s going to pay for that? The cost won’t be borne entirely by Europe and our other trading partners. That said, the outlook isn’t all doom and gloom because our economy has time and again proven to be incredibly resilient.

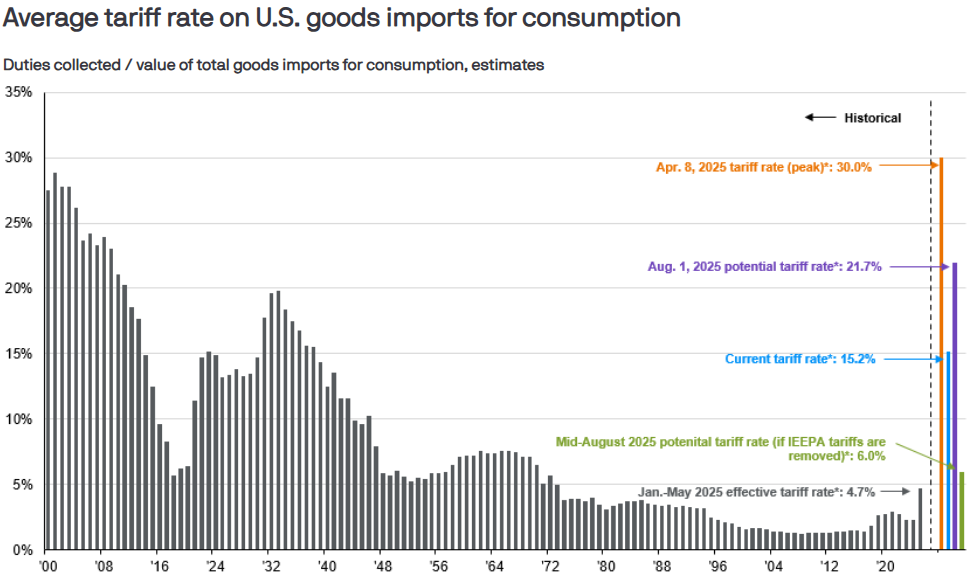

Along these lines, here’s another piece from JPMorgan that I received yesterday. The article has some reminders about tariff-related dates and a good visual of where average tariffs have been and where we appear to be headed.

From JPMorgan…

Peak policy uncertainty is likely behind us, with the average effective tariff rate recently settling near 15%, and markets have primarily shifted focus away from policy.

August could be another busy month of tariff deadlines. Peak policy uncertainty is likely behind us, with the average effective tariff rate recently settling near 15%, and markets have primarily shifted focus away from policy.

However, several key dates in August will be key to watch:

August 1st: New “reciprocal” tariffs on several countries, including major trade partners, are set to come into effect: 25% on Japan and Korea, 30% on Mexico (non-USMCA), 30% on the EU, 35% on Canada (non-USMCA), 50% on Brazil, and 50% on copper (in addition to previously implemented tariffs). With these measures, the average effective tariff rate could rise from 15% to 22%, based on 2024 import levels, marking the highest estimated rate since early April.

August 12th: This marks the deadline for negotiations with China, although an extension is possible. While 100%+ tariffs are unlikely to come back, the U.S.-China relationship is strained, with the deadline bringing a new chance for escalation. On the bright side, China has increased access to rare earths, with U.S. rare earth magnet imports from China surging 660% from May to June, which has helped ease tensions.

Mid-August: The Federal Circuit Court of Appeals may announce its ruling on the legality of the President’s use of IEEPA for some tariffs. A decision favoring the administration could uphold “reciprocal” and fentanyl tariffs of 10% or more. If the court sides with the Court of International Trade, which initially struck down the tariffs, the average effective tariff rate could drop to just 6%. However, other legal pathways exist for the administration to implement its tariffs.

The administration is hinting at a new baseline tariff of 15-20%, but this will depend on how the above unfolds.

What does this mean for investors?

Markets have appeared unfazed by the latest tariff threats. The S&P 500 hit a fresh high on July 21st, up 7.2% YTD, with markets refocusing on long-term themes like AI. However, the June CPI report indicates that tariff impacts are emerging and may intensify over the next few months, even before tariff rates potentially move higher. The impact on corporate earnings remains unknown – businesses may pass on the cost of higher tariffs to preserve margins, but price hikes could reduce sales in this environment.

There are plenty of other reasons to be optimistic about U.S. economic resilience and corporate earnings. However, it is still a good time to focus on active management and diversification as well as avoid overconcentration, which can help investors navigate the choppy waters of more tariff news.

Have questions? Ask us. We can help.

- Created on .