Well, what else can I say other than it’s getting scary out there. At this point we’re all aware of the almost hour-by-hour nature of the evolving virus situation and the new addition to our lexicon: social distancing. This concept will have broad and unanticipated impacts on our local and national economy. The past few days also brought sweeping changes from the Federal Reserve to help grease the financial skids, so to speak, as we prepare for a virus-induced recession.

In terms of your portfolio, it’s time to hunker down. But this doesn’t mean selling everything and burying cash in the yard. Instead, it’s time to focus on fundamentals and trying not to do anything rash. The stock market will find a bottom, likely before the virus situation stabilizes.

This is a psychological challenge for those of us who are independent problem solvers and doers. We see a problem and want to fix it. The problem now is that there’s very little to do in this situation (besides rebalancing as needed, which I’ve discussed already). What you can do instead of focusing on market movements is focus on your health and wellness and getting behind this whole social distancing thing.

While this is all feeling very 2008-ish in terms of market volatility, it’s important to remember our current predicament is fundamentally different in many ways. For example, businesses and consumers entered this situation on a stronger financial footing. Many states have healthy emergency funds. Property values aren’t unnaturally high. Unemployment is very low. The global financial system is healthy. This is all a positive contrast to 2008.

But like 2008, some of the best market days have come right in the middle of the worst days. Last Monday was horrible. Thursday was one of the worst days in recent memory and Friday was the best since 2008. Then yesterday was downright nasty, the fourth worst on record for the Dow. What’s an investor supposed to do except hold on for dear life?! While it’s probably hard to reconcile, we know throughout the long history of the market that missing the best days makes it incredibly hard to keep pace over the long term. We simply must endure the worst to also get the best.

It's important to remind ourselves of this as we go forward into the unknown unknowns of this outbreak. Among the many things we don’t know, just one has to do with the economic cost of social distancing. Yesterday JPMorgan sent out a note discussing its potential impact on the Leisure and Hospitality industries, which account for over 18 million jobs. Some of these are “corporate” jobs where laid-off workers get some support, but many are small businesses that will simply have to close until this all blows over. What will the owners and their employees do to recoup lost income? How will this affect their spending habits and what will the impact be on the broader economy? While this situation is temporary, it will be painful in various ways for most Americans.

Government can help here with a “shock and awe” fiscal stimulus package. This would coordinate with the Fed’s action this past weekend to drop short-term interest rates to effectively zero. The Fed is also restarting its quantitative easing program (QE) employed during and after the Great Recession. The idea with QE is that the Fed pumps money into the financial system by buying hundreds of billions worth of Treasury and mortgage-backed bonds of various maturities. This, and other Fed programs, is the extra grease I alluded to earlier.

Policy coordination between fiscal and monetary stimulus is the missing link at this point. That’s what investors and the American people are waiting for (among other things, of course). Broad stimulus coupled with extremely low interest rates and QE would reduce some of the rampant uncertainly out there while we do whatever we need to do to let this virus play out.

In the meantime, markets are likely to stay extremely volatile. We almost need new words to describe the current environment since “volatile” and “uncertain” don’t seem to do it enough justice. Put simply, unless a major stimulus package (or a miraculous reduction in coronavirus cases) is announced, this market situation will get worse before it gets better. There could be such a package as early as today, so fingers crossed for a good one.

Buying opportunities could become plentiful should the markets take another leg down, so I’m preparing for that on your behalf. And if you’re wondering, fortunately my work for you doesn’t have to stop due to social distancing or even a shelter in place order. So long as the Internet keeps functioning, I have full access to markets, your portfolio, your plan, and well… everything.

Last week was the fastest fall from a recent record high in the stock market’s history. Think about that for a moment. The average stock fell faster last week from its recent high point than anytime during the financial crisis or even the Great Depression. Those losses were deeper, of course, and took longer to play out while last week was all about speed. And the cause wasn’t a mortgage crisis or other financial calamity… it was the flu.

Now, I’m not trying to make light of the coronavirus outbreak. To date the virus has infected over 90,000 people around the world and claimed almost 3,000 lives, according to evolving reports. We’ve also had the US’s first deaths from the virus up in Washington state. And now we’ve learned about confirmed cases closer to home. Unfortunately, more are sure to follow.

The outbreak and its potential domestic impact are serious issues, but is it worth a one-week market correction of over 12%? I recall a day last week when only eight stocks in the S&P 500 were positive. Are all the other stocks really worth that much less? Obviously, sellers didn’t discriminate and I’m sure many people simply sold everything. A Wall Street Journal article from this past weekend told of 401(k) plan participants across the country trading 11x normal in their plans at work. Big short-term swings are part of the investing landscape, but last week sure seemed overdone.

In truth, the stock market had been riding high for quite some time and many investors were looking for an excuse to take profits. It could have been caused by anything. It wasn’t slowing global growth (pre-virus, of course), the trade war, or even impeachment. Investors largely looked through those issues and moved on. But the visceral fear of a foreign virus crossing oceans proved the right mix that caused just enough angst to create a panic.

It’s important to allow for market corrections from time to time. We experienced a nasty one just two years ago and stocks came roaring back. Fortunately, this outbreak is taking place when our economy seems to be getting stronger, or at least is not at imminent risk of recession. We had a couple of recession head fakes last year, but consumers and businesses have been reporting increasing levels of confidence. Maybe the virus changes this trajectory?

If US consumers and businesses start altering their habits due to the coronavirus, economists like former Fed Chair Janet Yellen say this could potentially tip the economy into recession. Along these lines, just this morning the Fed surprised markets by announcing it was lowering short-term rates by half a percent. Investors had been anticipating a reduction like this, but not until later this year and certainly not due to a virus. This kind of reduction is a double-edged sword, so it will be interesting to see how markets respond.

Amid all the stock market declines high-quality bonds have been up. This was expected and, by the way, is a big reason why we want to own them in the first place. For those of you who are currently retired, you can pick from your bonds to fund cash needs instead of selling stocks when they’re down. If managed correctly, the right kinds of bonds can be a store of cash to get you through a prolonged downturn for stocks. This is also why we don’t favor the riskier kinds of bonds that tend to behave like stocks when they’re taking a beating.

Because of all the buying in the bond world, yields are now down to historic lows (yields down = prices up). As of this morning, if you bought a 10yr bond from the government you’d be locking in a whopping 1.04% annual return. This has helped lower rates on mortgages, for example, so it might be a good idea to call your mortgage broker and ask about refinancing!

In all seriousness, we’re not out of the woods yet in terms of the virus’s potential impact on our economy. And the Fed’s decision this morning is a complicating factor. Even though stock prices rebounded strongly yesterday (the best single day in years!), there could be more wild swings and scary news from the firehose in the coming days and weeks.

For my part, I’ll be trying to sort through all the noise while continuously monitoring your investments and rebalancing as needed. My suggestion for you, for whatever it’s worth, is to continue keeping a cool head and to monitor websites like www.cdc.gov for useful information about what, if anything, to do about the virus.

It’s scary out there in cyber land. Crooks are lurking around every corner and its easier for them to strike as we demand more convenience from our devices. Or, at least that’s how it sounded while I attended another continuing education seminar on cyber security a couple of weeks ago. The content was geared toward advisory firms, but the details are applicable to anyone with a computer or smartphone.

Some of the high points dealt with changing recommendations about password formats and the importance of using password managers.

While experts used to recommend passwords ranging from about 8-10 characters, they now suggest that “length is strength”. Length is better than complexity, though I don’t fully understand the technical reasons why. It seems the longer the password the longer it takes a hacker to crack it, and they might move on to someone else’s password instead. A simple way to accomplish this is to use sentences as passwords, such as “ilikeitwhenthegiantswin”, or something that’s easy for you to remember but long enough to be difficult to crack.

You can make using longer passwords even easier by employing a password manager, such as Dashlane or LastPass. These subscription services use encryption to store your passwords and then work with your web browser to autofill your credentials once you’ve logged into the password manager’s website. So, at least in theory, you could create all sorts of crazy passwords and not need to remember them. Free versions are available, but it’s worthwhile to pay perhaps $10 or less monthly for more functionality. There are numerous practical benefits to this. But an important one is that by not physically typing your logins all the time you’ll be making it more difficult for hackers to monitor your keystrokes (which, apparently, is laughably easy for them to do).

It’s a little paranoid perhaps, but I don’t have any presumption of privacy while online, so taking extra steps like this provides piece of mind. Longer passwords and, ideally, the addition of a password manager is low hanging fruit when it comes to shoring up your personal cyber security. I’ll be addressing more methods in the coming weeks.

In the meantime, here are some helpful tips from the FBI’s cyber site. Some may seem obvious. But hackers often use the obvious ways in, such as duping you into clicking a bad link in an email, so don’t take the simplicity of these suggestions for granted. As technology races along, we all need to do a little (or a lot) more to protect ourselves.

As I was writing this yesterday morning, major market indexes had opened way down on virus anxiety and the relationship complexities between oil producing countries. So-called circuit breakers set to briefly halt trading during times of market stress had been tripped. Recession fears had quickly been rekindled amid an otherwise strong economy. In short, it was a “wheels are coming off” kind of Monday.

After a day like that, not to mention the past couple of weeks, the reasonable question is what on earth are we going to do about it? The answer, as you can probably imagine, is that we’re going to follow our plan. We’re going to focus on controlling what can be controlled. And we’re going to remain rational even as a growing number of people around us seem to be, well, losing their minds just a little bit.

What does this actually mean for your investments? What follows mostly applies to those clients who trust me to manage their investment accounts.

As we’ve discussed previously, we’ve positioned your portfolio to be diversified and, based on your plan, to be able to weather market craziness. This doesn’t mean you’ll experience none of the market’s downside. We all know that’s not possible when we’re also trying to get the upside.

Instead, your market exposure becomes a matter of proportion. If, say, the stock market falls by 10% and your portfolio has 60% of it’s money in stocks, you’d expect to fall by about 6%. Diversification and portfolio construction can help push these numbers a bit in your favor, going down even less and rising a little more, but there’s no free lunch here. I know you know that, but it’s helpful to remind ourselves at times like these, right?

What also helps is the other 40% (or whatever your portion is) being invested in “core” bonds. These are primarily Treasury bonds issued by the government and other bonds issued by high quality companies. Now, investors fearfully selling stocks often flock to bonds, but the buying in the past few weeks has been pretty extreme. Core bonds are up over 6% so far this year, well beyond typical expectations.

Bond prices have risen so much that yields (the implied investment return for new buyers) have hit historic lows almost daily for the past couple weeks. Every Treasury bond from one month out to 30 years yielded less than 1% yesterday and the 10yr Treasury, a key benchmark, fell to less than half that. Would you lend the government money for 10 or even 30 years for that piddly amount of interest? No way. You’d only buy bonds like that out of fear, or perhaps because you’re an institution and simply must put your cash somewhere. In short, panic selling of stocks begets panic buying of bonds.

The combination of stocks falling while bonds are rising means that, proportionally, your returns are better than the stock market over the past several weeks. We’ve made assumptions about this relationship within your plan and have stress-tested various “bad” scenarios as well.

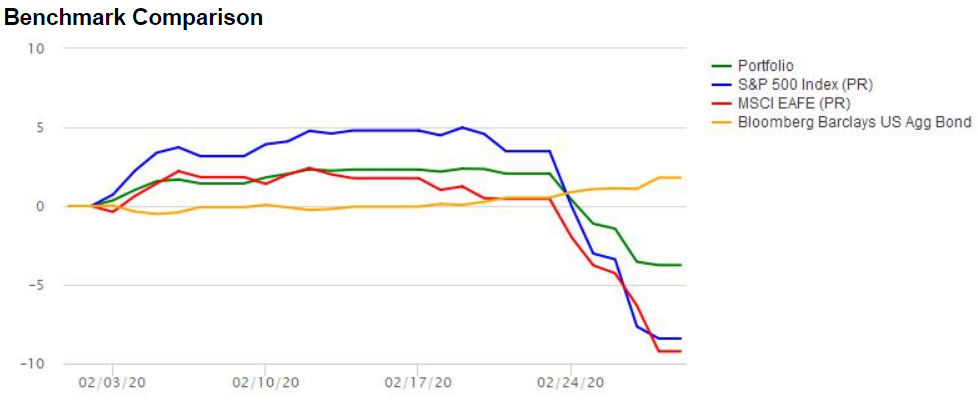

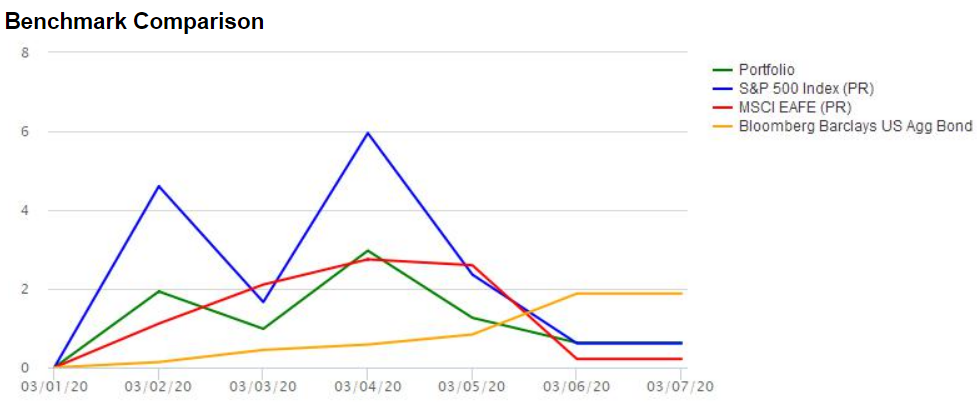

The following examples are from a typical client’s actual experience during the month of February and the first week of March. You’ll see how the green line (the client’s portfolio) hovers within the other colors (each of which is a market index). Essentially, this is what we’re shooting for over the long term and during nasty phases like the one we’re in now. The adage about investing being a marathon (even an ultramarathon where the middle is a great place to be) and not a sprint absolutely holds here.

This is important because the economic outlook is evolving rapidly. Several analysts, including my research partners Bespoke Investment Group, are now calling on the powers that be to provide immediate economic stimulus to avoid a recession this year. This abrupt change to the outlook was brought on by continued fears of contagion, both literally regarding the coronavirus and figuratively regarding economic impact from our neighbors’ actions (or inaction) to avoid it. Recent moves by OPEC and Russia that are driving down the price of oil don’t help the mood either.

So unfortunately, this kind of volatility could persist while these issues shake out. In the meantime, I’ll stick to our plan and manage your portfolio accordingly. This can, and probably will, include some buying of stocks assuming they fall sufficiently. This isn’t an exercise in trying to “time” markets but is part of my disciplined rebalancing process.

It’s sexier to talk about points than percentages when it comes to how the news media handles market movements. Take yesterday as an example. Markets fell due primarily to concerns about the spread of coronavirus. For most of the trading day the Dow Jones Industrial Average (the Dow) was down over 900 points before ending the day down slightly over 1,000.

That’s a big decline by anyone’s standards, but the news media leads with the point loss because it seems like such a large number, and it is. But if you dig a little deeper, you’ll see that since the Dow has grown in recent years, the percentage decline associated with the point drop was only about 3.6%, less than you might expect after hearing a dire number like 1,000. This is part of the reason you probably didn’t hear about how the S&P 500, a better indicator for market performance, performed about the same yesterday… though it was only a 112-point loss. Which sounds more newsworthy even though both were nearly the same percentage decline?

Point/percentage declines like we saw yesterday are not uncommon. They are utterly unpredictable, but markets do come back from them. For example, on so-called Black Monday in 1987, the Dow crashed about 23% in one day, or 508 points. During the Great Recession, the Dow frequently fell over 7%, or around 700+ points, on several different days. The Dow even dropped over 1,000 points, or about 4% or so, a couple of times just two years ago on global growth fears. Stocks eventually continued rising to the levels we see today.

This point fixation is a psychological challenge for investors (and the news media) and is one of the many reasons it’s so hard to be a successful long-term investor. I’m suggesting that while points are interesting, it’s the percentage changes that really matter. For example, on any given day it’s normal for stocks to rise or fall by 1%. That, by itself, is a boring number. But if it’s reported as the Dow “tanking” by 290 points, that sounds more interesting and gets reported as such, even if it’s the same thing as falling 1%. I think if percentage changes were quoted instead, the average investor could find it easier to stay calm amid what are often chaotic times.

So, long story short, take a deep breath when you hear big point declines being tossed around by media outlets. Nobody likes losses, but the actual losses you sustained are probably less than you imagine, especially if you’re well diversified.

All that being said, we’re still in the thick of it when it comes to fears about the coronavirus. Stocks are down a bit again this morning and bonds, where investors typically go during times of stress, are rising. If you’re interested, here’s some information put out by my research partners at Bespoke Investment Group yesterday morning regarding the virus.

You never know what’s going to happen to you. You’ve heard this a thousand times and I don’t have to tell you about the impermanence of life. But while we can’t control the future and the timing of our own demise, we can (mostly) control where our money goes after we do.

We accomplish this by naming beneficiaries on as many of our accounts as possible. They can be added at the bank, on our life insurance policies, and our retirement accounts at work and elsewhere. Not doing so automatically sends an account through the probate process after your death. There’s limited ability to control things in probate, so folks generally try to avoid it.

Naming beneficiaries is so simple that people often overlook it or forget to keep them updated. And passage of the Secure Act at the end of 2019 puts added emphasis on double checking your beneficiaries. Among other things, the Act now requires that non-spouse beneficiaries withdraw all the inherited money within ten years, with a boatload of taxes to go along with it. We discussed some of the implications with this a few weeks back, so I won’t bore you with the details again here.

Instead, let’s think more broadly about reviewing your beneficiaries. It’s a bit morbid perhaps, but for a successful review you need to wrap your mind around two potential scenarios; one, you’ve been “hit by the bus” while crossing the street and it’s lights out immediately, or two; you’re suffering from some sort of mental incapacity that precludes you from doing anything on your own.

In either case you’ve got what you’ve got in terms of named beneficiaries. Still have your ex-wife listed as beneficiary on your retirement accounts? Or, maybe you haven’t listed anyone at all even though you’re remarried and have children from both marriages? Maybe you simply wish you had done something different with beneficiaries. The bottom line is that you have to address this before death or incapacity, not after.

It’s important to remember that each account you own stands alone. You might have a will or maybe you spent thousands working with an estate planning attorney to craft the perfect trust document. But if you never actually updated beneficiaries on your IRA, for example, that account doesn’t automatically fall under the trust. Again, it’s on its own and would go through probate or, if you have stale beneficiary designations, directly to whomever is named, even if you’d currently (from the grave, I guess?) disagree.

While it might sound a little strange, there’s benefit to these accounts being separate. It gives you the opportunity to get creative. For example, most of us with a spouse and kids simply follow the “spouse gets everything, the kids get what’s left” school of thought. The Secure Act adds complexity here, but not for regular brokerage or bank accounts. Maybe one of your kids needs the money more than another. You could name the kid with lower income as beneficiary of your IRA while the other is named on your brokerage account (for its preferential tax treatment and no ten-year rule). Maybe one of your kids gets the Roth IRA (which would be tax free over ten years) and the other gets your pension (taxed as ordinary income). There are lots of ways to customize this.

But then as we all know, things change. Maybe over time your kids swapped their financial status, or maybe they’re both doing great and you’d like to add a charity or two as beneficiaries. This is why it’s important to check how you have things set up from time to time. You might find that choices you made five or more years ago no longer apply.

Again, and at the risk of being overly redundant, nobody but you can update your beneficiaries. We can help you think about the process and assist with the paperwork, but we can’t do it for you. We used to aim to review this every few years or so, but we’ll now be doing so annually with our ongoing clients. It’s simply too important not to.