We live in busy and interesting times, that’s for sure. Take the last week or so as an example. All at once we had the impeachment trial in the Senate, Brexit looming (it happened last Friday, by the way), and the coronavirus outbreak in China. We also had some strong but contradictory economic numbers percolating too.

But it was China that tended to dominate the market’s attention, especially last Friday when the Dow Jones Industrial Average slid 600 points, or a little over 2%. The S&P 500 fared a bit better but both indexes ended the volatile week down 2% or so. The main emerging markets index (of which China is a large portion) was down over 5% for the week.

Due to the outbreak the Chinese government had extended holiday closures of local stock markets through last week. Here at home risk associated with the virus had largely been priced into our markets since we weren’t on holiday. But investors in China hadn’t yet had an opportunity to “trade” the situation. As soon as they did yesterday, they sold, sending stocks in China down about 8%, an impressive single-day decline for any country. This let Chinese stocks catch up with commodities like oil, for example, which have been in freefall on fears that the outbreak will cause Chinese demand to slow.

The week of market turmoil also caused the yield curve here at home to invert… again. Although the inversion was slight, it’s still technically a recession indicator. The inversion has since reversed as of this writing as fears about coronavirus dissipate and investors sell bonds to buy more stocks. Still, the bond market has taken notice and currently expects one or two interest rate reductions from the Fed this year.

Fortunately for markets the outbreak came at a time when some of our economic indicators have been turning positive. The Institute for Supply Management tracks manufacturing activity across the country. The index had been contracting for several months but showed a surprise uptick in January, rising from 47.2 to 50.9. Readings below 50 indicate a recession for the sector, so this is a positive change after being weak for a while.

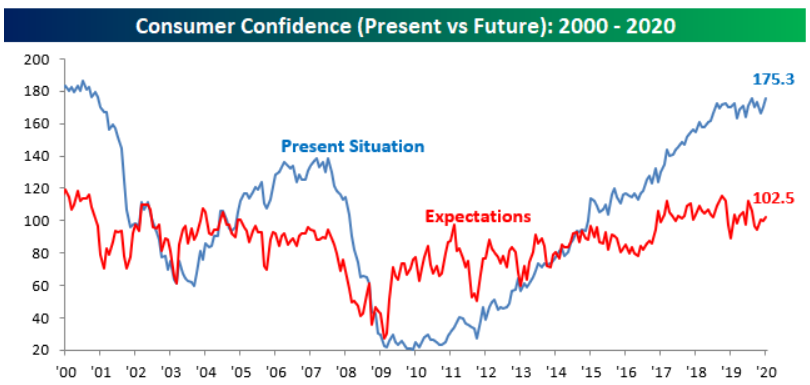

We also learned last week that consumer confidence has continued to rise well above its long-term average. Interestingly, at the same time consumers are reporting optimism, they’re also feeling less confident about their prospects. Your guess is as good as mine in terms of explaining this dichotomy, but it seems like a negative if one feels satisfied today yet doesn’t think it will last. That has to start showing up in our consumer-driven economy at some point, right?

While our economy seems to be trucking right along and defying gravity a bit, and markets have snapped back from last week’s losses, more short-term volatility should be expected as issues like coronavirus and Brexit play out in coming weeks. As we’ve seen in recent years, volatility bursts back onto the scene at unexpected times and in unanticipated ways. It’s important to remember that sometimes the best thing to do about market turmoil is absolutely nothing.

As we discussed last week, the purpose of the recently passed Secure Act was to make it easier for workers to save for retirement. Pretty much everybody acknowledges there’s a retirement savings shortfall in our country, so every little bit helps. The downside, however, is that laws making tax deferred savings easier must be paid for, and this was largely accomplished on the backs on those set to inherit retirement accounts.

Remember that IRAs, 401(k)s, and other types of retirement accounts weren’t originally intended to pass on wealth to heirs. They were meant to fund retirement and perhaps help with a surviving spouse. As we’ve seen over time, too-good-to-be-true-for-long tax loopholes eventually get closed. This is what happened several years ago with the Social Security “file and suspend” loophole that created a cottage industry of books, seminars, and so forth that for years helped folks “maximize” their benefits.

I’m a firm believer in understanding the rules of the game and playing the game hard, but I also try to acknowledge when something has to give. The victim this time around was the concept of “stretching” inherited retirement accounts.

Beneficiaries used to have two main options for retirement accounts they inherited. If the deceased owner was taking required minimum distributions (RMDs), heirs could start taking them on their own the year following the account owner’s death. Or, they could choose to clean out the account within five years. With some good investment management and proper planning, it was possible to try to stretch some of the money for decades, or even into the next generation. This also allowed more control over the timing and amount of taxes. No longer. Those inheriting retirement accounts will now have just one choice, to draw down the balance within ten years.

While these changes impact a broad array of beneficiary scenarios, here’s one that’s likely to start coming up:

Too much income too soon…

Jane’s mother passed away and left her a 401(k) worth $300,000 and a Roth IRA worth $150,000. While she’s mourning the loss of her mother, Jane is 60 and wondering how the extra money and extra taxes will impact her retirement plans.

Volatile markets, recession fears, trade war rhetoric, flagging manufacturing, and rising interest rates were on the minds of investors as we entered 2019. We had just seen a market rout in December and some investors were starting to head for the hills. But then to keep investors on their toes, some of these issues turned around abruptly and economic headwinds became tailwinds.

This shift in outlook led to an impressive year for stocks that continued during the 4th quarter (Q4). Here’s a roundup of how major markets performed in Q4 and for the year, respectively:

Large Cap Stocks – up 8.6% and 31%

Small Cap Stocks – up 10% and 26%

Developed Foreign Markets – up 7.4% and 22%

Emerging Markets – up 11.3% and 17%

Core Bonds – flat during Q4 and up 8.6%

Stocks behaved so poorly so quickly in late-2018, that a turnaround was to be expected. The S&P 500, a common benchmark for the US stock market, had declined almost 20%. But the turn of the year was almost like flipping a switch. Stocks surged in January, up almost 8% that month alone and were ultimately up ten months out of twelve in 2019.

Individual investors had been decidedly bearish but eventually began to turn more optimistic. While still far from being exuberantly bullish, investors showed more interest in stocks as the year progressed. Positive headlines about our trade dispute with China helped with this in Q4, even though no major deal was agreed to.

The Fed helped to juice up returns with three rate cuts during the year. The rate-setting body reversed its “hawkish” tone and indicated it won’t raise rates until inflation is significant and persistent. That could be awhile.

It’s never easy to see stock market indexes like the Dow opening down 400 points or more, especially on a Monday. Not a good way to begin the week, that’s for sure. This is especially true after a prolonged period where stocks mostly just went up. But as with any market swing it’s best to step back and assess the situation instead of simply reacting. Other investors do that enough for us anyway, so we don’t want to join them and make things worse.

So far this week (and toward the end of last week as well) stocks are primarily reacting to the outbreak of coronavirus in China. This brings back memories of the deadly SARS virus in 1993. That outbreak spread around the globe for about six months and claimed almost 800 lives, according to the CDC. The Chinese were criticized at the time for being slow to respond and opaque about the process. China’s government seems to be much more proactive this time around, shuttering roads, rails, airports, and even extending its New Year holiday season to keep people off the streets.

This situation is obviously very concerning and potentially dangerous. We don’t know how long or how widespread this outbreak will be. Hopefully it won’t be as bad as some are suggesting. But from my limited perspective, it’s interesting to watch how markets respond to situations like this. The Chinese economy is the world’s second largest, so any significant disruption in its system is going to create ripple effects throughout the world, which is part of the reason we see markets dropping in the short term.

Along these lines, I wanted to share the following excerpts of commentary I received from my research partners at Bespoke Investment Group yesterday morning. The first snippet is about the market reaction and the second is about the virus itself. The bottom line at this point, I think, is that stocks had been up for awhile without a meaningful decline and needed an excuse to fall a bit. The outbreak, and other issues, certainly provided it.

As you may have heard, right before the end of 2019 the government gave us the SECURE (Setting Every Community Up for Retirement Enhancement) Act. There’s a lot to it, but I’ll try to stick to the high points that are likely the most relevant to you.

No more stretching…

Let’s look at what will probably have a negative impact for many families. If you are planning to leave a retirement account to your kids or grandkids, they will generally no longer be able to take the proceeds over their life expectancies. This was known as “stretching” and allowed non-spouse beneficiaries to slowly withdraw (and pay taxes on) inherited retirement account balances that they didn’t necessarily need right away.

Going forward they’ll have to draw down the balance within ten years, paying taxes at a faster rate than would normally be the case. I recently read that this could generate almost $16 billion in tax revenue for the Treasury over the next ten years. This, at least in part, is how Congress paid for other changes in the new law.

Here are some important details:

1) This doesn’t apply to leaving retirement accounts to your spouse. The surviving spouse simply treats it as their own. This hasn’t changed.

2) The ten-year window doesn’t apply if you have already inherited a retirement account, just newly inherited accounts going forward.

3) If your estate planning documents leave your retirement account to a trust for the benefit of heirs, you should re-evaluate that decision. The reasons have to do with taxes and potentially different stretch provisions available to some types of trusts.

4) If your traditional (non-Roth) retirement account balances are likely to create distributions for your heirs that could cause them to pay higher taxes than you currently do, Roth conversions to prepay their taxes could help.

As has been my practice over the last few years, I’m taking a brief break from writing these Tuesday morning posts to spend a little more time with family and friends over the Holidays. I’ll be back with another post in early January. There’s a lot to talk about but it will have to wait until then.

I’m still working, of course, so let me know if you have any questions or need any year-end assistance.

Otherwise, we have a lot to be thankful for and this is best celebrated in person. I hope you’re able to spend time in the coming days with the people who are most important to you.

From my family to yours, Merry Christmas and Happy Holidays!