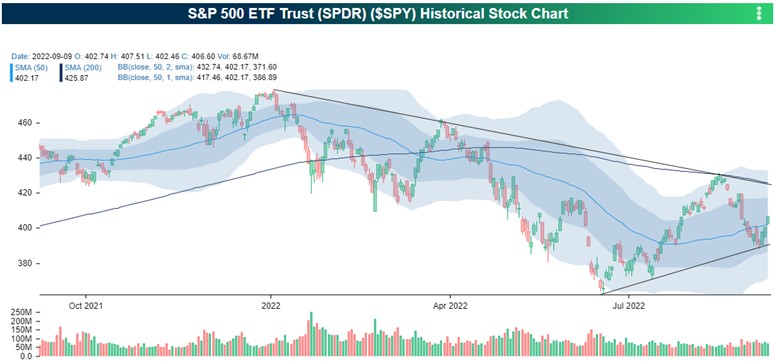

Initially I was going to post another blog about the markets since last week wasn’t great for investors. And after a brief respite we’re looking at another down day as I write this. The mood is still being driven by inflation, recession risk, and the Fed, with the latter expected to raise short-term interest rates by another 0.75% when they meet again this week.

But instead of all that, let’s discuss an article that piqued my interest because it addresses something I complain to my kids (now 16 and 20) about probably a little too often: what I call Death by Subscription.

What I’m talking about here is the insidious nature of the subscription and recurring payment model that’s become so popular. According to Gartner Research, all new software companies and at least 80% of existing companies, offer a credit card-based subscription service and recurring payment option of some kind. Many start with a freemium, or perhaps a trial period, before automatically hitting your credit card, usually every month, and often with no expiration date.

I’m not suggesting that automatic payments are a bad thing. On the contrary, they make my life a little easier by just happening versus me having to click a bunch of links and type out my credit card number or, heaven forbid, write and mail a check. But obviously we have to monitor this stuff and, unfortunately, this is only getting harder. So my problems with this are similar to what the article mentions, such as:

- The average person has 12 recurring subscription arrangements. Millennials have 17.

- Roughly 42% of us have forgotten about subscriptions and more than half of us underestimate our subscriptions by about $100 per month.

- On average, people are letting about $133 per month, or around $1,600 per year, evaporate from their checking accounts via unused or simply forgotten subscriptions.

So I was curious how much money I might be wasting because of this. Interestingly, it actually takes some grunt work to figure out.

Years ago I switched around my personal and business finances to only deal with one credit union for general banking needs and just one credit card for day-to-day purchases. I keep my business accounts separate from personal and this doubles everything, but the important thing is that on a typical day I’m only interacting with two institutions, Redwood Credit Union and American Express. This makes looking at data like this a lot simpler, or at least it does in theory.

I found out quickly that neither company allows me to search for recurring purchases. With algorithms these days I’m sure they could, but they don’t. So to find out what’s recurring I had to manually search my transaction history and write them down.

With Redwood Credit Union I was able to whittle down all of 2021 and this year so far by looking at “debits” and then sorting by less or more than $100, but it was still a lot of transactions to review. After spending maybe 30 minutes doing this I hadn’t found anything unexpected or forgotten about, so that’s good.

American Express had more capability than RCU, as I would expect, but I was still surprised that they didn’t let me search for recurring transactions. I could keyword search for “Netflix”, to see all transactions specific to that company, but my goal wasn’t just to review what I think my current subscriptions are. I also wanted to see if I had forgotten anything. So, unfortunately I had to scroll again, this time through a 33-page document covering 2021 and then a running list for this year, but at least Amex grouped the data by category which made the process a little easier.

Here are my takeaways after an hour or so of fiddling –

- It’s all too easy to lose track of recurring subscription payments, especially smaller dollar amounts. For example, I have three items each month for Apple on my Amex card. One is for Apple Music (that’s a keeper) but the other two are a little nebulous. I think my household doubled up for data storage that we don’t fully use. My iPhone lets me check subscriptions purchased through Apple, so I’ll have to give that a look.

- Streaming services now resemble cable. Netflix, Hulu, and Disney+? That’s about $41 per month combined. Do we need all three? Reviewing this stuff is a reminder that we subscribed to Hulu mostly for one show and the binging is over, so we should cancel it. And we really don’t watch Disney+ that much but a family member lets us use their Prime account and they use our Disney+, so it’s sort of a trade. That’s probably too much information, but it’s one reason for our multiple streaming services. What’s yours?

- Beware the annual auto-renewal as it’s very easy to miss when reviewing monthly or annual statements. For example, I found a subscription from last Fall that would have auto-renewed soon. Maybe I could have cancelled after the renewal and got my money back, but it’s much easier to figure it out ahead of time. I was also reminded of other annuals that I’m happy with and will let those renew after verifying the terms.

There are apps that help with this but, ironically, they’re auto-renew subscriptions too and, in theory, would only add to the problem if you don’t realize some value from them. Rocket Money is one that identifies and monitors your subscriptions. It’s free but requires payment for premium services, and I’m guessing subscription monitoring is one of those.

Some may say this is small stuff and not to sweat it and I get that, at least to some extent. But start adding these subscriptions up and we could be talking about a grand or two annually in real money that’s paying for unused products or services. I think that’s worth 10 minutes a day, Monday through Friday, to monitor your bank and credit card transactions, or at least a few times a year to review statements, don’t you?

Beyond that, this kind of review is part of taking more control of your finances. If you’re spending money, make sure you know what you’re getting in return. Don’t just let it happen. Good luck as you geek out on reviewing your subscriptions. It may be enlightening while also putting some cash back into your checking account. What to do with the money you’ve saved? Buy some stocks and bonds. You may have heard they’re on sale lately.

Here's a link to the CNBC article if you’d like to read more.

Have questions? Ask me. I can help.

- Created on .