What Bonds Do Best

Bonds have been going through a rough patch lately. No, they haven’t tanked in exciting fashion like stocks can do sometimes. They’ve just been boring and uninspiring. They’ve been like dead legs as you head out for a run on an otherwise beautiful day; an unworthy detractor. And they’ve underperformed.

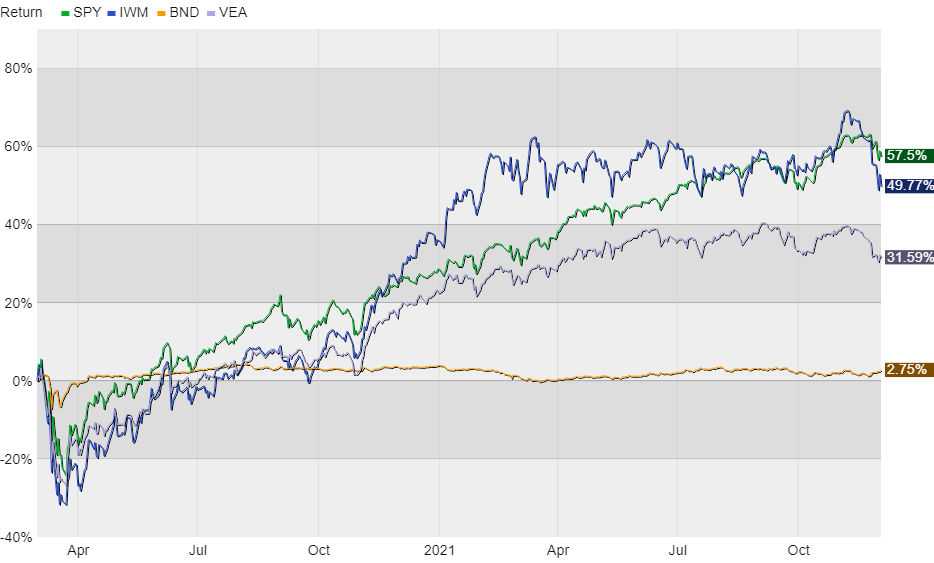

This underperformance is heightened by how well the stock market has done since the pandemic lows in March 2020. Since then the major bond market indexes have gained about 8% while stocks, depending on the index, have doubled. And pre-pandemic, from early-March 2020, bonds have only returned shy of 3% to the stock market’s 50% or more, again depending on the index.

The following chart shows this clearly. Here we see four big ETFs that each track a separate market index. SPY tracks the S&P 500, the primary US stock index. IWM tracks the Russell 2000, the main index for small-cap stocks. VEA tracks the MSCI EAFE, an index of developed foreign markets including Europe. And BND, the orange line, is Vanguard’s Total Bond Market fund, a good proxy for bonds issued by the US government, government agencies, and high-quality corporations.

It’s apples and oranges, but extended underperformance like this coupled with low interest rates leads many to ask reasonable questions like: Why should I own bonds at all? Shouldn’t I sell them and buy stocks instead?

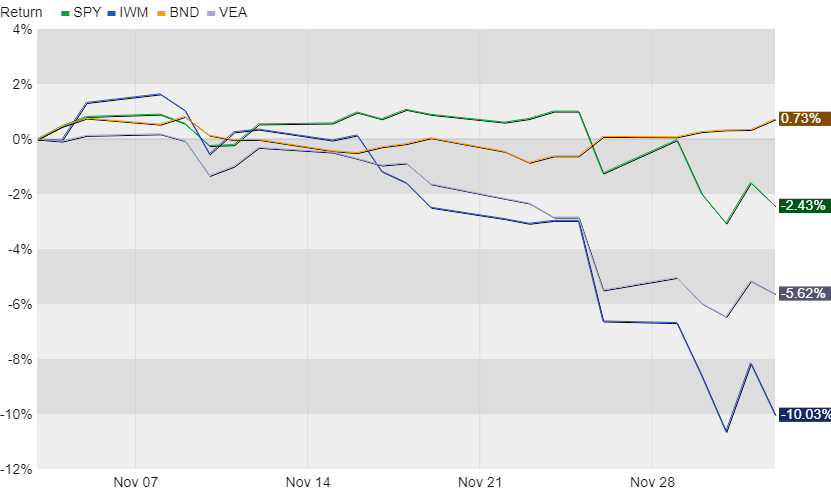

This is a tricky question, but the following chart of market activity during the last month provides a great example of why bonds are valuable to many investors. It’s all about downside protection.

Heading into this autumn, BND had been down about 2% year-to-date. Again, this stood in stark contrast to the stock market being up 20% or more during the same timeframe. And underperformance from bonds was dragging down moderate portfolios that might hold 30%, 40%, or even 50% in bonds. It’s hard to see one side of a portfolio performing so well while the other is acting like dead weight. So some head scratching was to be expected.

But of course that was when the stock market had been rising steadily. Add in the news of omicron causing overnight market anxiety, and bonds were suddenly showing investors what the asset class is best at: not being stocks.

What I mean is that when investors, individual and institutional alike, sell stocks they typically buy bonds, often short- or medium-term, to park money while waiting for the stock market to settle down. This raises bond prices during periods of stock market volatility and leads to the kind of behavior seen in the chart above. While this dynamic isn’t a guarantee day-to-day, and there can be periods when the relationship falls apart, it’s typical over time.

You own bonds in a moderate or conservative portfolio because the asset class smooths out stock market volatility and provides regular income. The give up is that bonds can’t rise as much as stocks overtime. So you have to choose how much protection you want versus how much volatility you’re willing to stomach in the name of growth potential. Part of the art and science of portfolio management is determining what proportions of stocks and bonds is ideal for the individual investor. There are rules of thumb, but no single right answer.

Do you have to own bonds? No. If you’re focused on growing your portfolio and see risk and volatility and your friends, you could maybe do with having less in bonds, or even cut them out entirely. And I’ve written before about how some investors could do other things to dampen their exposure to market volatility by enhancing their capacity to take risk. They could pay down debt instead of owning bonds. They could, under the right circumstances, buy a rental property for regular income instead of owning bonds. There are other options too.

But for most investors it’s just easier to buy high-quality bonds as part of a diversified portfolio. The right bonds in the right proportions will help reduce your portfolio’s reaction to stock market gyrations and will, ideally, keep you from doing anything rash when markets get crazy. Bonds do their job over time, just don’t expect them to be very exciting along the way.

Have questions? Ask me. I can help.

- Created on .