The fourth quarter (Q4) of 2024 ended with a depressing slump but otherwise continued what had been a strong year for US stocks. Foreign stocks perked up occasionally, as did US bonds, but our domestic stock market was the clear standout in terms of generating performance. The expanding AI industry, Fed policy, and inflation once again played important roles during the quarter and year while election outcomes in November reset expectations.

Here’s a roundup of how major market indexes performed during Q4 and for the year, respectively:

US Large Cap Stocks: up 2.5%, up 24.9%

US Small Cap Stocks: up 0.3%, up 11.4%

US Core Bonds: down 3.1%, up 1.3%

Developed Foreign Markets: down 8.4%, up 3.5%

Emerging Markets: down 7.3%, up 6.5%

The stock market was consistently strong during most of 2024 after a solid 2023. The AI boom continued to lift “growth” sectors like Technology and Communication Services. There were some bouts of volatility, especially in late Summer but the S&P 500, the typical benchmark for US stocks, stayed above its 200-day moving average the whole year. The S&P hit 57 all-time highs throughout 2024, the most since 1928. Technology stocks, including companies like Nvidia and Apple, accounted for roughly 40% of the S&P’s return while Communication Services stocks, such as Meta and Google, accounted for about 20%, so performance was again tilted heavily to certain sectors. My research partners at Bespoke Investment Group found that the Magificent 7 (popular stocks propelled by the AI boom) now make up 33% of the S&P’s weighting, slightly more than the Tech sector itself at about 32%. And Apple, Nvidia, and Microsoft account for nearly 60% of the Magnificent 7. Growth from these companies boosts returns for the whole market in the short-term but concentrations like this can work the other way as well. It wasn’t all about AI, however. The Consumer Discretionary and Financial Services sectors also posted strong gains, up 29% and 28% for the year, respectively. At the other end of the spectrum Energy, Real Estate, and Healthcare sectors finished the year up slightly while the Materials sector was the lone loser, falling nearly 2% for the year.

November’s election impacted markets in a number of ways but something interesting was Bitcoin hitting $100,000 per “coin” during Q4. Notoriously volatile, the cryptocurrency was rallying going into Election Day and took off when Donald Trump won his second chance at the White House. The reasons why are varied but seem focused on expectations for a friendlier regulatory environment under the new administration. While this seems reasonable, only time will tell if crypto speculators are right.

Expectations for lower interest rates also had an impact on market returns last year and certainly in Q4. For most of the year investors had been expecting the Fed to start aggressively reducing interest rates as inflation continued to fall, but the first change didn’t come until September. The Fed reduced its short-term rate benchmark by half a percentage point during that month’s Open Market Committee meeting, in line with market expectations. The Fed then lowered rates by a quarter point each during its November and December meetings. However, inflation seemed to perk back up so the rhetoric around these decisions, especially in December, led investors to reevaluate expectations for how low rates might go in 2025. Investors had been anticipating short-term rates might fall by a full percentage point or more in the new year but, as of this writing and based on the CME Group’s FedWatch Tool, this has been revised to maybe a quarter to a half point drop. Uncertainty around this caused major stock market indexes to fall from a few to several percent as the year ended in true anticlimactic fashion.

All this again dragged on bond prices during 2024, but mostly during Q4. Prior to that, bond investors had been pricing in the aforementioned rate cut expectations which helped the Bloomberg US Aggregate Bond Index peak at over a 5% return for the year by mid-September. It was downhill from there to the 1.3% annual return and the expectation reset mentioned above. Prices fell as yields rose. The benchmark 10yr Treasury yield ended the year at nearly 4.6%, up from September lows and impacting, among other things, 30yr mortgage rates which hit 7.3% as the year closed. So 2024 was another challenging year for investors who favor the safety and liquidity of investments like US Treasurys and high-quality corporate bonds. Typical money market funds returned close to 5% for the year, more than core bonds and other traditionally safe investment options. Elsewhere within the fixed income realm lower-quality “junk” bonds returned nearly 8% for the year and preferred stocks gained roughly 7%.

So we’ve had a good run for stocks and I still think the economy and markets have a tailwind. That said, there’s bound to be volatility stemming from uncertainty about the new administration in Washington, global instability, and a host of evergreen issues like inflation, Fed policy, and when, not if, we’ll see our next recession, just to name a few. If you’re still saving and don’t need cash from your investments anytime soon, you can leverage volatility by investing more when prices fall, either by rebalancing or investing new money. If you’re spending from your investments, this might be a good opportunity to replenish your cash, pay off some debt, and otherwise batten down the hatches. (I’m not trying to be negative, just practical following a good year with relatively low volatility.) Otherwise, I’ll continue to rebalance your portfolio as needed if I’m responsible for managing it. Let us know how we can help with any of this.

“What’s past is prologue”, according to Shakespeare. Contrast that with how past performance isn’t a guarantee of future results, according to our common industry disclosure, and you’d be correct in wondering why we spend so much time talking about history. I mean, are we trusting it as a guide for the future or not? I’ve always liked the middle ground quote from our American Shakespeare, Mark Twain, about how “history doesn’t repeat itself, but it often rhymes”.

I mention this because of the recent two-year anniversary of ChatGPT being unveiled to the public. As we’re all aware, the ensuing AI craze provided a major tailwind for the stock market over the past couple of years, although it’s tapered off a bit lately. AI’s dramatic impact on markets has been compared to the sea change of the internet’s “creation” in the early-90’s that eventually led to a market bubble. That whole process took over a decade to run its course but the last couple of years certainly seems to rhyme with it, at least so far.

I’m reminded of a Far Side comic from some years back. I couldn’t find the image to share with you, but I’m sure you can imagine the scene:

A person sits alone at a bar presumably deep in worry and drink, hoping for just one more bubble before retirement. The thinking, or at least how I interpreted the cartoon, is that a bubble would be obvious the next time and one could simply ride it until almost bursting, sell their stocks, and all their worldly problems would be solved.

While there’s a simple logic to that, part of the irony of the cartoon is how history doesn’t repeat itself exactly, it rhymes, as Twain suggested, and if hitting homeruns every time was that easy everyone would do it. So history is useful and important to help us understand the present but is pretty lousy as a predictive tool because future facts and circumstances will always be different.

Is history doomed to repeat itself due to AI’s impact on markets, making a major market bubble and subsequent burst something preordained? That’s sort of a dark question early in this holiday season but it’s nonetheless something to pay attention to.

All that said, here’s some snippets of information, charts, and context along these lines from my research partners at Bespoke Investment Group…

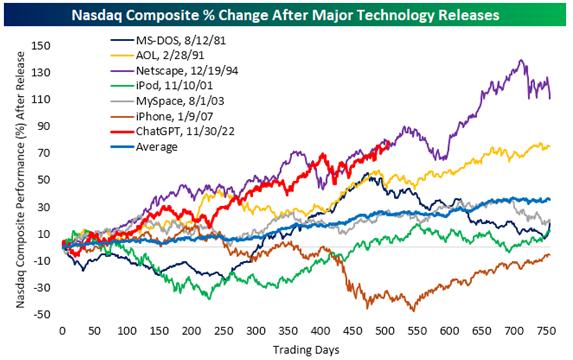

November 30th marked the 2-year anniversary of the release of ChatGPT, which kicked off the AI Boom. The success of ChatGPT has resulted in a massive ramp-up of capital expenditures in addition to various end-user adoptions like AI copilots, AI image generation, chatbots, humanoids, self-driving cars, and more. Leaving it to the imagination, there are endless applications for AI in modern life so the sky is the limit and it certainly will be looked back on as a notable technological advancement.

With ChatGPT turning two, we've updated our chart comparing the Nasdaq's performance since its release to other major tech releases over the past few decades. These include the first Microsoft MS-DOS operating system in 1981, AOL in 1991, the Netscape web browser in 1994, the iPod in 2001, MySpace in 2003, and the iPhone in 2007.

The Nasdaq is currently up 79% since ChatGPT's release on 11/30/22 (506 trading days ago). That barely edges out the Nasdaq's gain of 73% over the same 2-year time frame following the release of the Netscape web browser in December 1994. As you can see in the chart, these two releases -- ChatGPT and Netscape -- look very similar with bigger gains than any other major tech release since 1980.

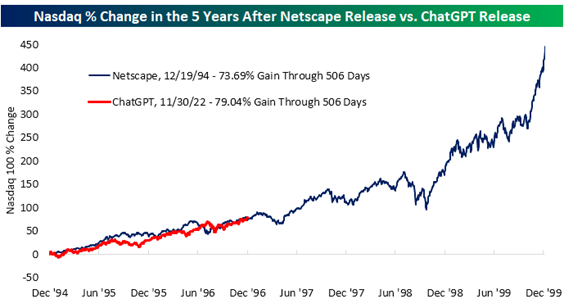

Below is a closer look at the Nasdaq's move since ChatGPT's release on 11/30/22 versus its performance following the release of the modern web browser (Netscape) in late 1994. In this chart we've expanded the timeline out to the end of 1999 so you can see just how much more the Nasdaq would go on to rally in the second half of the 1990s. For those arguing that we're still in the early innings of the AI Boom, this chart provides you with some strong ammo! Two years after the release of Netscape, the Dot Com Bubble of the 1990s was still just getting started.

(We would note, though, that if the Netscape comp holds, there would be a pullback in the next 100 trading days or so before the next leg higher occurs.)

I don’t know about you but I’m finding myself to be more of a traditionalist these days. I like my holiday season evenly distributed with each holiday given it’s due. So I balk when Christmas decorations start popping up before Halloween and Thanksgiving sort of floats in between. And when Black Friday and Cyber Monday deals start showing up in my inbox weeks ahead of schedule, it throws me off. If these are early deals, shouldn’t I just wait for even better prices after Thanksgiving? But as with so much these days, all this seems subject to wide interpretation and is mostly about marketing anyway. Gosh, I’m feeling grumpy this morning…

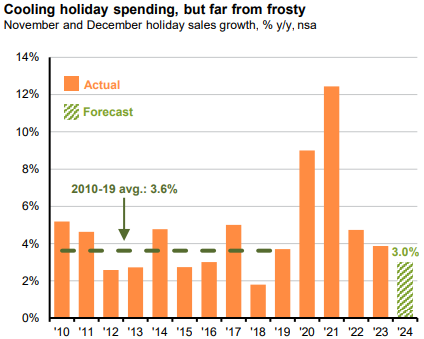

Another traditional part of the holidays is people forecasting how much consumers might spend during the shopping season. This, too, is subject to opinion and perspective but consumers are, on average, expected to spend a record amount as they hit the malls, online retailers, and the nation’s roads and airports. The TSA is predicting a record year for Thanksgiving week travel, for example. Easing inflation has helped, along with a strong wealth effect from increased asset prices.Given that consumer spending has accounted for roughly 80% of GDP growth this year, more spending is a good sign for our economy, even when viewed through the tempered lens below. I’ll again lean on a quick summary and chart from JPMorgan this week that illustrates this point.

Besides that, I’d like to take a moment to wish you and yours a wonderful Thanksgiving. This is one of my favorite holidays. Family and friends come together in gratitude and appreciation for, well, everything. There’s good food and drink, and perhaps discussions stretching beyond politics. Enjoy!

From JPMorgan…

This Thanksgiving, as families gather around the table, the festivities provide a welcome reprieve from the political tensions of recent months. With Americans expected to spend nearly a trillion dollars spreading holiday cheer, this spending showcases their resilience in a shifting economic landscape.

While holiday spending is projected by the National Retail Federation to hit a record high, sales growth, as shown by the chart of the week, is expected to fall slightly below the pre-pandemic average of 3.6%. However, this moderation reflects easing inflation rather than weakening demand. In fact, when adjusted for inflation, real sales are set to exceed last year, buoyed by record shopper turnout and an anticipated rise in per-person spending to around $900. Driving this is real wage growth, which has remained positive for a year and a half. Furthermore, stock market gains and recent Fed rate cuts have lifted consumer confidence. That said, elevated prices, along with the depletion of pandemic era savings cushions, may cap spending growth for some households.

Retailers, for whom the holiday season drives a disproportionate share of annual sales, face a mixed outlook. Deal hunting consumers are turning to discount retailers, boosting revenue and profit forecasts. Conversely, those reliant on discretionary categories like apparel and specialty goods are seeing softer demand as shoppers focus on essentials.

Despite challenges, this season reflects a broader economic trend: slowing but not stalling. As winter sets in, consumer spending is cooling but remains far from frosty—underscoring the resilience of the U.S. economy as we head into 2025.

Counting today we have ten market days left in the year – it’s crunch time. This calendar compression isn’t new but is still hard to get comfortable with. I’m spending these last days double checking that RMDs have been taken on schedule, Roth conversions and other transfers are completed, portfolios are properly balanced, and that appropriate losses get harvested for tax purposes.

There’s been less of the latter this year, fortunately. Stocks have done well and bonds have chugged along, with core bond market indices up for the year about 2-3% as I type. There’s been volatility in both parts of the market but it seems like bonds have been consistently choppy. This has created some unrealized losses in bonds that could be harvested within non-retirement accounts, so I’m watching that closely as we approach year-end. Ultimately, I’ll only harvest a loss if the tax benefit is proportionally large enough not to get absorbed by a short-term upswing, or if the client has other realized gains this year that I’m trying to shield. Maybe this is too much information, but it sheds a little light on some of the important details I handle as we close out the year.

Otherwise, at this point we’re expecting another 0.25% short-term rate reduction from the Fed when the rate-setting committee meets tomorrow. The CME’s FedWatch tool indicates a 97% probability of a reduction (down a smidgeon from yesterday’s 99%) so the only question now is how the Fed explains its decision and how it sees the road ahead for inflation, the job market, and the economy. Market and economic indicators show a mixed bag while there still seems to be a tailwind as we prepare to enter the new year, but it’s always best to expect the unexpected.

I’ll write more about all this in my Quarterly Update during the first week of January. Until then I’m taking the next couple of weeks off from writing this blog. I’ll still be hard at work, of course, both with details like I already mentioned and the rip-roaring fun of formal continuing education. My education never stops since I read and watch daily, but it doesn’t often come with “credit”. I normally do a lot of formal continuing ed via industry conferences but I’ve slacked off on those this year. Couple that with a regulatory change requiring a certain amount of hours by year-end and I have some catching up to do. Note to self: don’t procrastinate so much next year!

Beyond that, let me take this opportunity to wish you and yours a happy holiday season and a fabulous start to 2025. Good luck and best wishes from all of us here at Ridgeview Financial Planning.

Good morning everyone. I hope you had an enjoyable Thanksgiving last week. For me, it was a good time to add some calories that I’d soon be burning off.

While I won’t bore you with all the details, I spent most of this past weekend paddling a stand-up paddleboard in 3.3-mile loops within a water park in Sarasota FL. The race is called Last Paddler Standing. Sounds fun, right?

The main event went up to 48 hours of continuous one-hour loops. A “super loop” of about 4.9 miles kicked in at lap 49 – more on that in a minute.

Finish each loop however fast you want but the next one starts at the top of the next hour and if you miss it you’re out. You could drink while paddling but eating or otherwise taking care of yourself all had to be done between loops.

This sort of thing exists in the running world and is often referred to as a “backyard ultra”, but to my knowledge it’s unique in paddling. Races like this draw experienced pros and weekend-warriors like me – it’s a good mix.

Each loop began at the top of the hour and took most paddlers about 45-50 minutes to complete. This often left me with 15 minutes during the early loops but more like 10-12 as the loops wore on. Sleep? Forget about it. It’s amazing how much you can do to reset yourself in a few minutes but it really takes a toll on your body and mind as the hours roll on.

I ended up completing 31 laps, top six if I recall correctly. This meant 31 hours of paddling a long rectangular loop while a cold north wind blew the entire time, sometimes with a vengeance. You’d ride the wind down but struggle against it most of the way back. It was so strong at times that it just seemed ridiculous. There’s nothing quite like being cold, wet, and windblown – definitely not what a California Boy expects to find in Florida.

Anyway, my 31 laps were eclipsed by the remaining five paddlers who each went the full 48, as I recall.

Then the super loop kicked in with its added distance, but into that same north wind. Yikes. Incredibly strong/professional paddlers attempted it and failed to finish in the allotted hour.

Still, two managed to finish the first super loop. Just prior to beginning the second super loop, one backed out, leaving the remaining paddler to complete one loop on his own within the allotted time to win the race.

Imagine this… you’ve just paddled for 49 hours in challenging conditions with hydration and food when possible, but no meaningful rest. Then you’ve got to do it one more time, alone, and with weather conditions that were only getting worse. You paddle your brains out and end up finishing about 30 seconds too late. Congratulations on your accomplishment but no, you didn’t “win” the race, the course won. Still, the guy absolutely crushed it and it was one of those inspiring moments that you don’t see very often, even though he didn’t make it in time.

While the final race result was a heartbreaker, my experience was good. I had a few trips down into the pain cave but my wife and kids (my crew), and comradery with friends helped me keep going. Additionally, the other racers, their crews, and the race staff all came together in rough weather to create something special. I plan to sign up for it again but I sincerely hope for better weather next time. Optimism… it gets me into trouble sometimes.

In last week’s note I mentioned how many, if not most, investors are in wait-and-see mode when it comes to the new administration’s impact on the economy and markets. I also mentioned how investors generally favor traditional Republican ideals of lower taxes and less regulation. That said, nobody likes uncertainty.

Along these lines, the following is a great summary from JPMorgan on the ongoing reassessment happening in the markets. We’ve discussed this in recent weeks, but it’s helpful to get some confirmation. Investors had been expecting interest rates to drop rapidly but are now revising those assumptions. This impacts bond prices directly and feeds into stock prices, while also percolating throughout the economy. Rates remaining higher for longer would be a net-negative for the economy and would hit homebuyers and people with consumer debt hardest. The WSJ reports that the average 30yr fixed rate mortgage is about 7.4%, higher than referenced below. And the Prime rate, impacting credit card balances for example, is still at 7.75%, not terrible but substantially higher than a few years ago.

From JPMorgan…

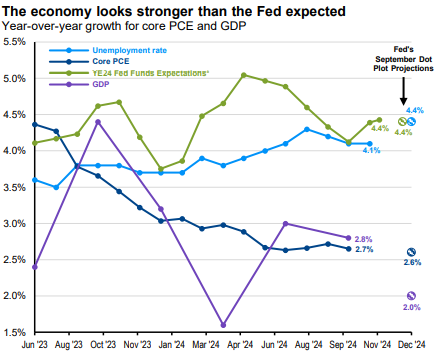

In September, the Fed kicked off its cutting cycle because “the balance of risks” had shifted. But subsequent economic data and the election results could be shifting it back. This week’s chart shows both growth and the labor market are tracking stronger than the Fed expected, posing upside risk to inflation.

Core PCE [personal consumption expenditures] has come down since 2022, but progress has stalled over the past few months. Both CPI and PPI rose solidly this month, increasing estimates for October PCE. Moreover, the housing inflation driving CPI is unlikely to alleviate anytime soon. The ~75bp sell-off in the U.S. 10-year since the first cut has pushed mortgage rates from 6.1% to 6.8%, and housing purchase activity remains near its lowest level since 1995.

While [Fed Chair] Powell stated at the November meeting “in the near term, the election will have no effects on our policy decisions,” investors are likely more concerned about the long term. Several of Trump’s top priorities are somewhat inflationary. Immigration restrictions could re-heat the labor market, stoking wage growth, and tariffs could increase prices. This, combined with a potential trade-war supply chain disruption, could reverse recent disinflation progress in goods.

Altogether, risk seems more skewed toward inflation than in September. December revisions to the dot plot [where Fed policymakers chart their economic assumptions] should reflect this, but the Fed will likely stay the cutting course. However, markets are currently only pricing ~70bps of easing by the end of 2025, compared to ~95bps before the election and ~160bps after the September meeting. Investors should be aware future easing could progress slower and end quicker than previously expected.

Elsewhere in the realm of uncertainty, investors are waiting to learn who President-Elect Trump will nominate to be Treasury Secretary. As you can imagine, this cabinet position can have significant impacts on markets, for better or worse, and is probably the most relevant pick for investors to watch. The position is up in the air as I type this morning. The primary concern among market watchers is how willing a new Sec Tres will be to leverage tariffs. As alluded to above, trade wars, spats, and so forth slow trade in an interconnected global economy, so add that to the list of things for investors to worry about.

Ultimately, these unanswered questions stoke short-term volatility as we swing from unbridled optimism to something more guarded. This may be with us for a while as the new administration gets sorted. Remember, though, that markets can seem shaky even as prices are rising. Some have historically referred to this as climbing the wall of worry, while the WSJ over the weekend referred to investors betting on a market melt-up. However you frame it, investors are cautiously optimistic at a minimum and that’s a good thing.