Last week was a big one for markets. The Fed announced another interest rate decrease, we had some good economic and corporate profit reports, and that other midweek announcement… what was that about again?

All kidding aside, you’re likely aware that the stock market surged on last week’s election news. Republicans were predicted to sweep the White House, the Senate, and the House (the latter now confirmed as I type this Tuesday morning). Very generally speaking, the stock market favors less regulation, lower taxes, and business-friendly legislation, all of which are expected when Republicans control the government. Will the market get what it wants? Perhaps, but last week and for the time being it’s all about shifting expectations.

That said, one of my professional tenets is not to lapse into politics. I don’t have anything to add other than personal opinions and I’m sure you’ve had your fill of those from elsewhere in recent days and weeks anyway. This isn’t to suggest that politics is unimportant, far from it. Instead, I prefer to deal with the practical implications of our politics, how it impacts markets, the economy, and so forth. So let’s look at some of the market reaction last week and some context as we move forward.

The stock market had been heading south a bit prior to the election but nothing major. Then the generally unexpected results (if you went by the major polls) came in late Tuesday and Wednesday saw an increase of 2.5% for the S&P 500, over 3% on the Dow, and the NASDAQ also surged higher. The S&P 500’s 50-day moving average price swung from “neutral” to “extremely overbought” in one day. For the week the S&P gained about 4.5%.

The relief rally, as described by the WSJ, impacted some parts of the market more than others. Small cap stocks had a one-day gain of nearly 6%. For the week, Tech and Financials were up over 5%, and Consumer Discretionary stocks were up 9% as investors “waved bye-bye to Bidenomics”. Bringing down the average were Real Estate, Healthcare, and Consumer Staples sectors, which each grew by maybe 2% or less. Utilities actually declined a couple percent last week. And in the realm of purely speculative assets, Bitcoin shot up and is over $86,000 as I type, based largely on assumptions the new administration will reduce regulation on cryptocurrencies.

Bonds initially fell as stocks rose but held up through week’s end. Yields on Treasury benchmarks were volatile but the 10yr Treasury yield settled around 4.3%, for example. Performance-wise, short-term bonds were flat to up a little, while medium-term bond index funds like the iShares U.S. Aggregate and Vanguard Total Bond Market were up around 0.8% for the week. Long-term bonds performed better but that’s after getting beat up during the few weeks prior. Elsewhere in fixed income, preferred stocks rose over 2% as their hybrid nature fed on optimism about stocks.

Helping fuel market performance last week was another rate reduction from the Fed. This marks 0.75% off the top of short-term rates since September. The pace of rate reductions is now expected to slow with about a 65% chance of another quarter point reduction when the Fed meets again in December. The bias is till toward reducing rates into the new year, especially since Fed Chair Jerome Powell mentioned during his press conference last week that rates are still high enough to restrict growth. But I think he, like many Americans and market participants in general, were surprised by the election results and are in recalibration-mode in terms of what policies to expect and how that changes the economic outlook. For example, the CME’s FedWatch tool currently shows investors expecting around another half percent rate reduction by Spring, versus over twice that prior to Election Day.

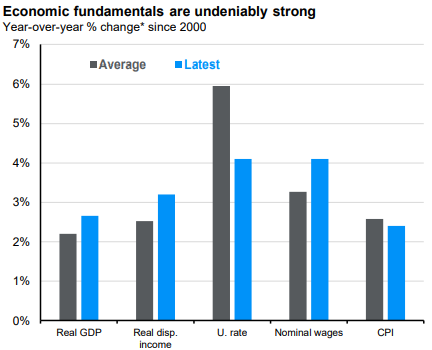

Along these economic lines, here’s a chart that I received yesterday from JPMorgan that speaks for itself.

As I type, markets have begun the new week with continued optimism. Will it last? Only time will tell. The jury is still out on the question of which party is better for markets. Frankly, there are too many variables and too much of a time lag to legislative changes to come up with an unbiased answer anyway. However, like I already mentioned, investors (collectively) favor the idea of Republican control, at least at the outset, and we can easily see how the market’s pulse quickened since last Wednesday.

So let’s be pragmatic and take what the political environment and markets throw at us in stride. Expect volatility while expecting long-term growth. Beyond that, if I’m managing your portfolio please know that I intend to stick with the plan. As values continue to rise in some parts of your portfolio, we’ll rebalance. Should any part of your portfolio need updating or replacing, I’ll handle it. If something has fundamentally changed in your financial life, such as your work situation or major unexpected expenses popping up, please let me know.

Have questions? Ask us. We can help.

- Created on .